Q2 Ends In The Black

The second quarter wrapped up a roller coaster quarter with a positive gain last week. After a 91 bps climb in the S&P 500, the index finished the quarter up 2.9%. Meanwhile, the Barclays Aggregate Bond index sank 2.3% for the period. That was the worst quarterly return since Q2 2004, and just the third loss of more than 2% in the past 20 years.

There was a full slate of economic data for investors to digest last week, with indicators covering multiple sectors of the US economy.

On Tuesday, several important housing indicators were released. The first related to housing prices, as the S&P/Case-Shiller and FHFA House Price indices were reported. Overall, both reading suggested that housing prices continue their upward trajectory.

The FHFA index, which measures housing prices on transactions involving agency-owned properties, increased 0.7% in April and 7.4% year-over-year. Although April’s rise was slightly below expectations, March was revised upward by 0.2%. The index has steadily improved since bottoming in mid-2011.

The Case-Shiller report indicated similar improvement. Housing prices rose 1.7% in April, with increases observed across all components. On a year-over-year basis, the index is now 12.1% higher, a sharp acceleration from July 2012 when the index was just breaking out of negative territory. According to Econoday, this was the first double-digit reading since May 2006.

Following last week’s encouraging existing home sales data, new home sales came in quite robust. The measure rose to a seasonally adjusted annualized rate of 476,000 sales in May, 16,000 above consensus. The prior month was also revised higher by 12,000 sales. Supply appears to be stabilizing, ticking up to 4.1 months from 4.0 the month before. Analysts pointed to tight supply as a headwind for continued sales earlier in the year.

On Wednesday, investors received a bit of negative news when the final reading of first quarter GDP was revised lower by 0.6%. The estimate was initially reported as 2.5% in April, then as 2.4% in the second estimate. Economists had not expected any significant revision to May’s number.

The downward revision was attributable to personal consumption, which is not a positive development for an economy driven primarily by the spending habits of its citizens. The Commerce Department reported that personal consumption fell to 2.6% from the originally reported 3.4% gain. Exports and imports were also adjusted downward, softening overall output.

Investors were treated to additional information on personal consumption on Thursday, with the release of the Personal Income & Outlays report. Data for May showed that consumer spending expanded 0.3% in the month, slightly below expectations. This follows an April figure of negative 0.3%. The mixed results foreshadow another modest quarter of GDP growth.

Incomes were slightly more positive, with a 0.5% gain during the month. This was well above economists’ expectations, and follows an upwardly revised 0.1% increase in April. If incomes can continue to firm, consumption data may look more positive in the months ahead.

Investors Gear Up For Earnings Post-Taper

Following a few weeks of FOMC-induced turmoil, investors are looking forward to getting back to the fundamentals. Second quarter earnings season are set to kick off July 8 with Alcoa, in what will mark an important reporting period for financial markets. Given the now much telegraphed intentions of the Fed, investors are scrutinizing whether the US economy and corporate sector is ready to stand on its own feet.

Unfortunately, early indications may be no. According to FactSet research, a record high number of S&P 500 companies are issuing negative guidance for the second quarter. To date, 87 companies have guided lower, with just 21 issuing positive guidance. Negative guidance has been concentrated across a broad range of sectors.

Source: FactSet

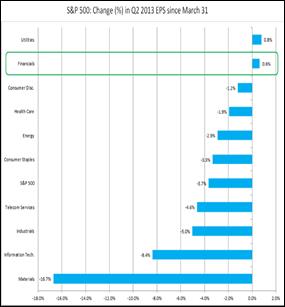

In line with the levels of negative guidance, analysts have cut earnings estimates sharply during the period. On March 31, the aggregate earnings estimate for the second quarter stood at 4.2%. During the past three months, that has been negatively revised 3.4% to 0.8%.

FactSet notes that this negative revision is actually better than the five-year average of negative 6.4%, but it is slightly skewed by financials. That sector, which has suffered the brunt of investor risk aversion during and after the financial crisis, was one of only two sectors to see earnings revised higher during the quarter. During the past five years, financials has experienced negative revisions averaging over 20%.

Source: FactSet

As we noted last week, however, many banks are poised to generate better results given the recent movement in interest rates. Because they can borrow at short-term rates that are still near zero, banks see their margins rise by lending at the now rising longer-term rate. This is likely a major contributor to the more favorable outlooks by analysts. Markets agree, as financials were the top performing sector during the second quarter.

Outside of financials, the breadth of negative downgrades has been rather broad-based. Data from Bespoke Investment Group revealed the ratio of positive to negative earnings revisions moved into negative territory over the past four weeks. Within the S&P 1500, an index that covers a broader range of stocks than its more well-known sibling, analysts upped their estimates for 400 companies while lowering them for 481. Additionally, seven of the ten major sectors saw negative revision ratios. Compared to the first quarter, however, analysts are slightly less negative than they were entering the reporting season.

If S&P earnings growth does manage to reach just a 0.8% rate, it will mark a continuation of a slowdown in corporate bottom line results that began in earnest in Q4 2011. The corporate sector has appeared to reach a stable, but low trajectory, similar to that seen for the broader US economy. Investors will likely need to see a more robust rate of growth before becoming comfortable enough to absorb the end of QE without complaint.

The Week Ahead

Investors can expect some major market moving data in the week ahead. On Monday, the Institute of Supply Management (ISM) releases its manufacturing index, followed up by its services index on Wednesday. Following the market closure on Thursday in observance of Independence Day, the Labor Department releases its monthly nonfarm payroll and unemployment reports.

In Europe, both the European Central Bank and Bank of England meet this week. No major changes to monetary policy are expected. For the BoE, this will be the first meeting with new head Mark Carney, formerly of the Bank of Canada. Some view Carney as more aggressively dovish compared to the outgoing governor Mervyn King.

Other central banks meeting this week include Romania, Russia, Australia, Poland, and Sweden. Romania and Poland are expected to cut their benchmark rates by 25 bps each.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value

© Fortigent