Rising Rate: Challenge and Opportunity

Summary

While the prospect of rising interest rates generally strikes fear into the hearts of fixed income investors, it’s important to remember that periods of rising rates are normal and can create opportunities for active bond managers. Since 1970 there have been 21 periods in which interest rates rose significantly. While each has had its own unique characteristics, over the past 20 years equities have rallied during these periods, which has tended to support corporate credit markets. Also, interest rates generally rise in a nonlinear fashion that creates opportunity for active investors who have the flexibility to buy and sell during market dips and peaks, minimize exposure to the most rate-sensitive segments of the yield curve, and use individual security selection to benefit from market dislocations.

Reversing course

There appears to be no greater fear in the hearts of fixed income investors than the prospect of rising interest rates. Over the past few years, unconventional monetary policies by the U.S. Federal Reserve (Fed) have suppressed U.S. Treasury rates to unprecedented lows in an effort to stimulate economic growth.

However, recent U.S. economic data reflects modest acceleration that may give the Fed the support it needs to begin tapering quantitative easing (QE).

Fixed income investors find this worrisome, of course. Reassured by repeated Fed pledges to hold rates down, investors have flocked into the bond market in recent years, driving up prices and sending bond yields — which move inversely to price — to record lows. It’s important for investors to remember that back-ups in rates are a normal part of a well-functioning economic system and should not signal cause for panic. Going back to 1970, there have been 21 periods during which rates rose significantly. Some key points to consider:

• While each rising-rate period has its own unique characteristics, over the past 20 or so years equities have been more likely to rally, not decline, when rates are rising. Strong equity markets have tended to support corporate credit prices even when interest rates were rising.

• Historically, interest rates have not risen on a linear track — there have been numerous spikes and pullbacks, and we believe within that volatility lies opportunity for active bond managers.

• While passive fixed income investors may be in for a rocky ride toward less-attractive total returns, active bond managers have more flexibility to manage duration (for example, shifting allocation toward less rate-sensitive segments of the yield curve) and to use individual security selection in an effort to benefit from market dislocations.

Equities often rally, credit potentially benefits

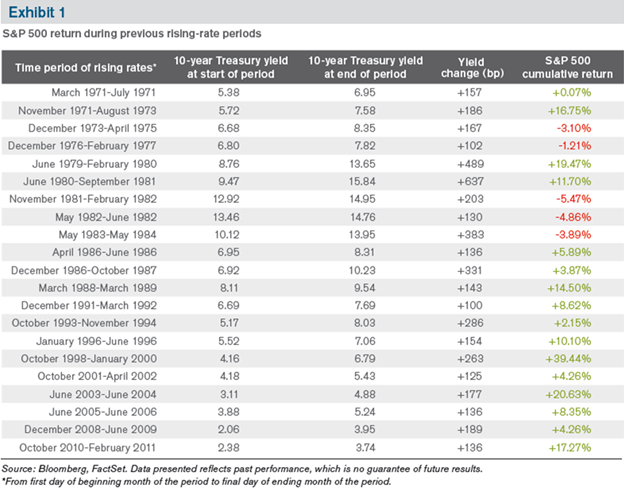

Since 1970, there have been 21 periods in which the benchmark 10-year Treasury bond yield rose by at least 100 basis points (bp). In the 1990s and 2000s, equities — as reflected by the S&P 500 Index — rallied in all rising-rate periods (Exhibit 1). Equities rallied during roughly half of the rising-rate periods from the 1970s into the 1980s, partly because Fed policy was less effective in keeping inflation contained during those years. Equity returns historically have not shown much correlation to the magnitude of the yield change.

For fixed income investors, rising equity markets can buoy corporate credit even as interest rates are rising. Improving economic fundamentals also have tended to lead to lower credit default rates and enhanced company balance sheets.

Volatility creates opportunity

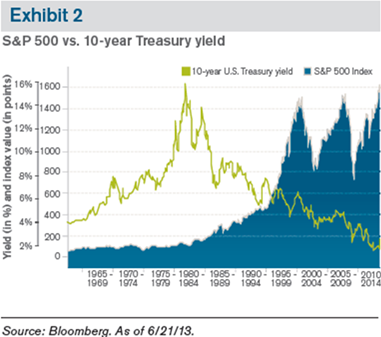

In general, declining interest rates have tended to support higher stock prices over the long term. But the progression has not been linear (Exhibit 2). Instead, both stock and bond prices progressed jaggedly along a trend line. If this pattern repeats itself, it should provide plenty of opportunity for active fixed income investors to buy on dips and sell on rallies.

We do not expect to see a violent, sustained move in interest rates, as this would be destabilizing to the economic recovery that the Fed has worked so strenuously to promote the past five years. Rather, we believe there will be a general upward trend in rates punctuated by periods of headline driven volatility. This is part of a necessary process as investors start repricing assets for positive real rates of return (net of inflation), assessing the probability of an improving global economy and accepting that the artificially low interest rates of the past few years are not sustainable.

Like all significant change, these shifts can be painful as investors move through them. However, they have been common. We believe they can be navigated successfully by taking calculated risks, focusing on capital preservation and keeping a close eye out for the opportunities that come from interest rate changes.

Active management matters

As we’ve previously pointed out in various whitepapers (including Why Credit Matters, 2009, and RedefiningRisk in Fixed Income, 2011) the major structural changes that have occurred in the U.S. fixed income market since 2008 have made the Barclays U.S. Aggregate Bond Index (Agg), a widely used proxy for passive fixed income investors, highly sensitive to interest rate changes. This means that nonactive investors using the Agg as a benchmark — whether in passive strategies or exchange-traded funds (ETFs) — are implicitly making a bullish bet on interest rates (i.e. that interest rates will decline). This was a beneficial strategy as rates were declining, but we doubt that most investors currently would be comfortable making a passive bet on a continued decline in rates.

While we believe that rates will trend higher, we don’t view this as a terrible crisis for fixed income markets. On the contrary, we believe it is a natural repricing. Typically, periods of market repricing can create opportunities for active investors to buy securities at attractive valuations, reposition at different points along the yield curve and reallocate between asset classes, sectors and securities. All of this can be good for investors in terms of capital preservation and positioning for the next market cycle.

We believe one of the key elements of active versus passive management is the ability of an active manager to express a bearish view in the market by not owning the securities or segments of the market that have the most downside risk, or where investors are not being adequately compensated for risk (although when valuations fall, it is possible for both active and passively managed investments to lose value).

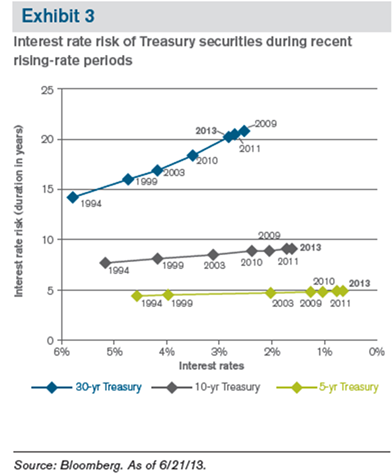

For instance, if one looks at interest rate sensitivity (duration) leading into the last seven notable rising interest rate years for 5-year, 10-year and 30-year Treasury securities (Exhibit 3), a pattern emerges. Since 1994, as interest rates have declined, sensitivity to rate changes (i.e. duration) has increased, particularly for the 30-year Treasury bond. We believe that the greatest risk of capital loss lies in the longer end of the yield curve, in securities maturing in 10 years or more, and we’re closely monitoring that segment and taking steps to minimize our exposure.

Navigating a post-QE world

Investors may fear entering a period of rising rates, but they don’t need to be afraid. While navigating a rising-rate environment can be challenging, we believe that active fixed income management and expertise in security selection can be beneficial. After the shock of QE tapering subsides, we believe attention will focus even more closely on individual company fundamentals, and that the markets will reward companies that are making positive structural changes in their business and enhancing their balance sheets.

Change is unsettling, and a significant reversal in interest rates definitely would alter the fixed income landscape. However, change creates opportunity. In our view, bond managers that are experienced in risk management around duration and in employing fundamental, bottom-up security selection will be in a good position to help maximize risk-adjusted returns and preserve client capital.

![]()

Please consider the charges, risks, expenses and investment objectives carefully before investing. For a prospectus or, if available, a summary prospectus containing this and other information, please call Janus at 877.33JANUS (52687) or download the file from janus.com/info. Read it carefully before you invest or send money.

Past performance is no guarantee of future results.

Investing involves market risk. Investment return and value will fluctuate, and it is possible to lose money by investing.

Bonds in a portfolio are typically intended to provide income and/or diversification. In general, the bond market is volatile. Bond prices rise when interest rates fall and vice versa. This effect is usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss.

Any portfolio risk management process discussed includes an effort to monitor and manage risk which should not be confused with and does not imply low risk or the ability to control certain risk factors.

There is no assurance that the investment process will consistently lead to successful investing or the stated objectives will be met.

The views expressed are those of the authors as of July 2013. They do not necessarily reflect the views of other Janus portfolio managers or other persons in Janus’ organization. These views are subject to change at any time based on market and other conditions, and Janus disclaims any responsibility to update such views. No forecasts can be guaranteed. These views may not be relied upon as investment advice or as an indication of trading intent on behalf of any Janus fund.

In preparing this document, Janus has relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources.

Barclays U.S. Aggregate Bond Index is made up of the Barclays U.S. Government/Corporate Bond Index, Mortgage-Backed Securities Index, and Asset-Backed Securities Index, including securities that are of investment grade quality or better, have at least one year to maturity, and have an outstanding par value of at least $100 million.

S&P 500® Index is a commonly recognized, market capitalization weighted index of 500 widely held equity securities, designed to measure broad U.S. equity performance.

Duration measures a bond price’s sensitivity to changes in interest rates. The longer a bond’s duration, the higher its sensitivity to changes in interest rates, all else being equal.

Janus Distributors LLC (06/13)

Investment products offer are: NOT FDIC-INSURED. MAY LOST VALUE. NO BANK GUARANTEE.

FOR MORE INFORMATION CONTACT JANUS

151 Detroit Street, Denver, CO 80206 I 800.668.0434 I www.janus.com

C-0613-40943 06-30-15 188-15-25823 06-13

© Janus Capital Group