The beginning of the return to normalized interest rates took a big toll on straight Treasury securities in the 2013 second quarter, but TIPS got hit even harder. For the quarter, the average TIPS security lost 6.6%, worse than the average loss of 3.0% on comparable maturity Treasurys and by far the worst losses seen in the TIPS market since the 2008 financial crisis.

TIPS are complicated primarily because their returns are based upon two components: current income and inflation. In theory, TIPS investors are willing to accept lower current income because they have some protection against an increase in inflation. So, for example, a TIPS investor might accept a 1% current yield, even though a comparable maturity Treasury security offers 3%, because he expects inflation to be at least 2% or 200 basis points. The difference between the 3% straight Treasury yield and the 1% TIPS yield is commonly known as the breakeven rate.

This is a simplified analysis. The actual mechanics of the relationship between current income and the inflation adjustment are more complex because the inflation adjustment is added to principal which is not received until maturity. Furthermore, the inflation adjustment is based upon the Consumer Price Index, which may or may not be a good proxy for the actual rate of inflation.

Like all fixed income securities, TIPS are exposed to fluctuations in the general level of interest rates. So, using our previous example, if the yield on the straight Treasury security rises to 3.50% because of a general increase in interest rates and inflation expectations remain unchanged at 2%, then the yield on the TIPS would be expected to rise from 1% to 1.50% and investors would suffer a corresponding loss in principal value.

In the 2013 second quarter, however, in addition to the rise in interest rates, inflation expectations declined. According to our calculations, the breakeven rate fell from 250 basis points to 168 basis points. This indicates that inflation expectations fell broadly, but especially on the short end of the yield curve. We know this is true because of the sharp decline in commodity prices, especially the plunging price of gold. The decline in the breakeven rate means that investors were less willing to pay a premium for the inflation protection offered by TIPS. The much sharper losses in TIPS in the second quarter were therefore due to two factors: (a) the general rise in interest rates and (b) a sharp drop in inflation expectations.

At the end of the quarter, the average breakeven spread on both 5-year and 10-year TIPS were within the bottom of their recent historical ranges (from 2011 to the present). All other things being equal and assuming that inflation expectations increase going forward, we should expect to see TIPS outperform straight Treasurys in the quarters ahead. TIPS could still suffer losses, if interest rates continue to normalize, but their losses should be less than those on straight Treasurys, assuming that inflation expectations revert back to their average recent historical levels.

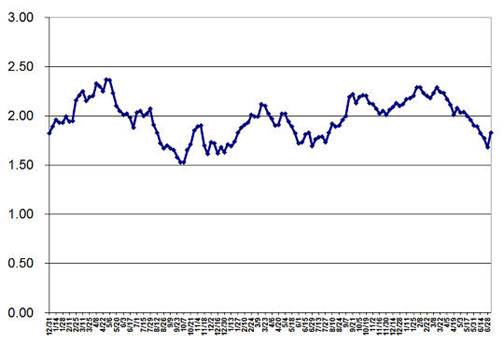

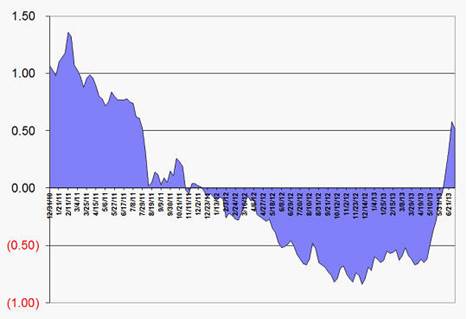

Chart 1

Yield Spread Between Constant Maturity 5-Year Treasury Note and 5-Year TIPS: 2011-2013

Source: U.S. Federal Reserve data

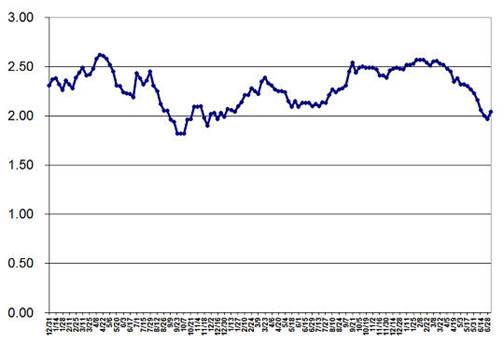

Chart 2

Yield Spread Between Constant Maturity 10-Year Treasury Notes and 10-Year TIPS: 2011-2013

Source: U.S. Federal Reserve data

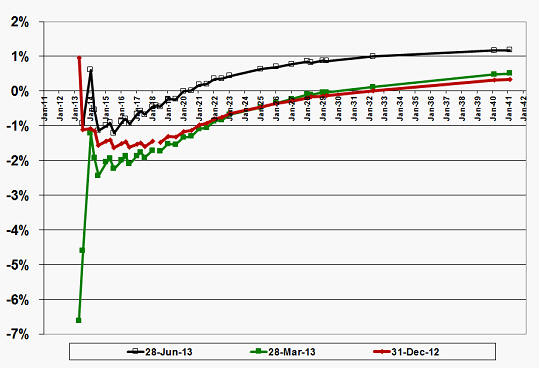

Chart 3 highlights the significant shift in the TIPS yield curve in the 2013 second quarter. From March 28 to June 28, the yield curve rose by about 125 basis points on average across all maturities.

Chart 3

TIPS yield curve: Dec. 30, 2012, Mar. 28, 2013 and Jun. 28, 2013

Source: Pricing obtained from Barron's and the Wall St. Journal; yields calculated by Lark Research, Inc.

During the 2013 second quarter, TIPS prices fell on average by more than 9 points!!! TIPS with short maturities (to 2015) fell by 2-3 points. Intermediates fell by 8-9 points; and long maturity TIPS fell by an astounding 18-19 points.

In the 2013 first quarter, the yield on TIPS was negative for maturities out to 2029. At the end of the second quarter, with the upward shift in the yield curve, TIPS yields were negative for maturities out to 2020.

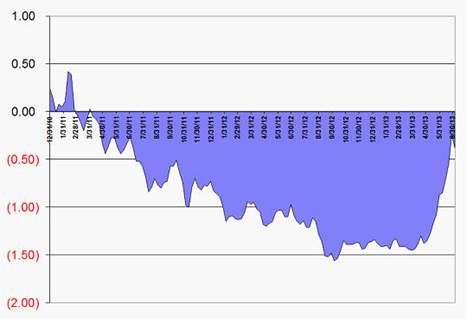

Chart 4

5-year Constant Maturity TIPS yields: 2011-2013

Source: U.S. Federal Reserve

The yield on five year TIPS ended the 2013 second quarter at -0.24%, 121 basis points higher than than the -1.45% yield that they carried at the end of the 2013 first quarter and 112 basis points higher than the -1.36% yield at the end of 2012. Five-year constant maturity TIPS yields had bottomed at -1.62% on October 4, 2012.

Chart 5

10-year Constant Maturity TIPS yields: 2011-2013

Source: U.S. Federal Reserve

10-year TIPS yields ended the 2013 second quarter at +0.58%, up 120 basis points from their -0.62% yield on March 28, 2013 and up 130 basis points from their -0.72% yield at December 28, 2012. The low water mark for 10-year TIPS yields on a weekly basis was -0.84 on December 7, 2012.

Table 1

Yield and Performance on TIPS vs. Comparable Maturity Treasurys: 2013 First Quarter

|

TIPS |

Comparable Treasury |

Breakeven |

Return |

Return |

|

|

Averages |

Yield |

Yield |

Spread |

on TIPS |

on Treas. |

|

2010-2015 maturities |

-2.45% |

0.16% |

2.60% |

0.2% |

0.1% |

|

2016-2021 maturities |

-1.48% |

0.96% |

2.45% |

0.3% |

0.4% |

|

2025-2040 maturities |

0.08% |

2.59% |

2.51% |

-2.0% |

-1.1% |

|

Totals |

-1.34% |

1.16% |

2.50% |

-0.3% |

0.0% |

Source: Lark Research estimates calculated from pricing data obtained from the Wall St. Journal. Returns on TIPS and comparable maturity Treasurys were calculated from Dec. 28, 2012 to Mar. 28, 2013.

Total TIPS returns were slightly negative at -0.3% on average in the 2013 first quarter, as small gains in the short- and intermediate maturities were offset by losses in the longer maturities. Comparable maturity straight Treasury securities produced breakeven returns. TIPS yields ended the first quarter at -1.34% on average, compared with -0.94% at the end of 2012, but the average is somewhat misleading because most of the decline in yields was realized on the shorter maturity TIPS. By comparison, yields on comparable maturity straight Treasurys were 1.16%, up from 1.13%.

Table 2

Yield and Performance on TIPS vs. Comparable Maturity Treasurys: 2013 Second Quarter

|

TIPS |

Comparable Treasury |

Breakeven |

Return |

Return |

|

|

Averages |

Yield |

Yield |

Spread |

on TIPS |

on Treas. |

|

2010-2015 maturities |

-0.73% |

0.22% |

0.96% |

-0.8% |

0.0% |

|

2016-2021 maturities |

-0.27% |

1.47% |

1.74% |

-6.6% |

-3.1% |

|

2025-2040 maturities |

0.94% |

3.09% |

2.15% |

-13.6% |

-6.0% |

|

Totals |

-0.07% |

1.61% |

1.68% |

-6.6% |

-3.0% |

Source: Lark Research estimates calculated from pricing data obtained from the Wall St. Journal. Returns on TIPS and comparable maturity Treasurys were calculated from Mar. 28, 2013 to Jun. 28, 2013.

In the second quarter, TIPS suffered an average loss of 6.6%, with the losses concentrated in the intermediate and long maturities. Straight Treasurys fell 3.0% on average, with losses also concentrated in the intermediate and long maturities. Breakeven spreads declined from 250 basis points on average in the first quarter to 1.68%, as the losses on TIPS exceeded the losses on straight Treasurys. The decline in breakeven spreads was greatest in the shorter maturities, due primarily to a decline in inflation expectations.

Table 3

Performance of TIPS Mutual Funds as of June 28, 2013

|

Performance |

Annual |

||||||||

|

NAV |

Assets |

One |

Three |

Five |

Expenses |

||||

|

Fund Name |

Ticker |

28-Jun-13 |

($B) |

13Q2 |

YTD |

Year |

Year |

Year |

as % |

|

Am. Cent. Inv. Infl. Adj. Bond |

ACITX |

12.10 |

4.61 |

-7.51% |

-7.86% |

-5.46% |

4.06% |

4.07% |

0.47 |

|

Am. Cent. Inv. Infl. Prot. Bond |

APOIX |

10.25 |

0.80 |

-3.24% |

-2.31% |

-0.83% |

4.08% |

3.63% |

0.55 |

|

BlackRock Infl. Prot. Bond A |

BPRAX |

11.02 |

3.93 |

-6.63% |

-7.52% |

-6.03% |

3.98% |

3.83% |

0.85 |

|

Dimensional Infl. Prot. Sec. |

DIPSX |

11.67 |

2.57 |

-7.95% |

-8.40% |

-7.95% |

5.06% |

4.24% |

0.13 |

|

Dreyfus Infl. Adj. Sec. |

DIAVX |

12.76 |

0.35 |

-6.91% |

-8.02% |

-6.91% |

4.00% |

3.52% |

0.70 |

|

Fidelity Infl. Prot. Bond |

FINPX |

12.34 |

2.96 |

-7.21% |

-7.99% |

-7.21% |

4.26% |

3.53% |

0.45 |

|

T. Rowe Price Inf. Prot. Bond |

PRIPX |

12.47 |

0.43 |

-7.09% |

-7.60% |

-7.09% |

4.17% |

3.73% |

0.50 |

|

Schwab Infl. Prot. Sel. |

SWRSX |

11.15 |

0.37 |

-7.14% |

-7.86% |

-7.14% |

4.32% |

3.52% |

0.19 |

|

Vanguard Inf. Prot. Bond |

VIPSX |

13.36 |

32.11 |

-7.34% |

-8.00% |

-7.34% |

4.56% |

3.61% |

0.20 |

|

Averages |

-6.78% |

-7.28% |

-6.22% |

4.28% |

3.74% |

0.45 |

|||

Sources: FINRA

The performance of TIPS mutual funds mirrored the returns on individual securities. The average TIPS mutual fund in this sample suffered a loss of 6.78% in the 2013 first quarter, compared with the average loss of 6.6% calculated for all TIPS securities. Any differences in performance among TIPS mutual funds probably relate to differences in average duration. Those funds more heavily exposed to the long end of the yield curve should have suffered greater losses in the quarter.

© Lark Research, Inc.