Making Sense of the Bond Market

Income and Diversification Still Valid Reasons to Own Bonds

• The great challenge for investors and advisers today is to forecast where interest rates and bond prices will be once the influence of radical central bank intervention dissipates.

• Measures of inflation expectations are declining, and deflation remains the dominant influence on interest rates.

• In assessing whether to trim bond allocations, it is important to revisit

the reasons for selecting a particular asset allocation before modifying or abandoning it.

The US Federal Reserve’s quantitative easing (QE) is designed to make money affordable and encourage economic growth. After nearly $3.2 trillion in open- market bond purchases it is nearly impossible to believe this has had no affect on the yield curve. The sheer size of the action compels us to believe that rates today are artificially low. Accordingly, bondholders fear that once this artificial

downward pressure is released, rates will return to “normal” higher levels and bond prices will decline.

The Crash of 2008 and resulting Great Recession forced unprecedented levels of government spending and borrowing globally. Lackluster economic growth in the aftermath has failed to generate the tax revenue required to reduce deficits or pay down debt. In an effort to support massive debt loads and boost economic growth central banks have deployed ultra-low (i.e., zero) short-term interest rates (ZIRP) and QE. The conundrum for bondholders is that while these policies may help debtors pay debt service and avoid default now (boosting bond prices), they may also destroy the purchasing power of the interest and principal owed to lenders later.

Early rounds of QE may have already washed out of the bond market and may no longer present a risk of rising interest rates for bondholders. New research1 shows that both QE1 and QE2 ultimately drove forward rates down respectively. Significantly, it was found that the length of time QE affected forward rates was relatively short, between four and 12 months, and that the duration of the effectiveness of subsequent rounds of QE declined with each application.

Gauging the Bond Markets' Reaction to QE

During each round, medium and long-term interest rates actually rose.2 Yes, you read that right. Rates went up. When each round or stimulative (or both) for the economy, and demanded higher rates. When the money printing ended, rates moved back down in response to still sluggish growth and low inflation. Investors judged

Infinity” was designed to create an unbounded or lasting inflationary stimulus. As one might expect, the market has reacted by pushing rates higher. But with rumors of Federal Reserve Chairman Ben Bernanke’s retirement coming in January 2014, QE Infinity may turn out to be no more infinite than the first three versions. If the Fed tapers QE Infinity before a durable economic recovery is in place, rates may return to their previous low levels.

Another interpretation of the impact of QE comes from Dr. Lacy Hunt of Hoisington Investment Management who makes a compelling case that US rates are in fact exactly where they should be regardless of Fed policy.3 He believes rates belong at historically low levels for years to come given weak aggregate demand, low personal savings rates, poor labor force participation rates, declining velocity of money (the turnover rate of dollars in the money supply), extraordinary global public debt burdens, and negative demographic trends among G-8 countries.

Remember, the Fed is trying to counter strong deflationary forces that naturally produce low rates. In the short term the Fed wants rates low to stimulate growth. Eventually however, they want rates to rise due to higher self-sustaining levels

of economic growth and employment. Truly the Fed is trying to thread a needle between inflation and deflation. If Japan’s attempt to generate lasting growth and inflation using ZIRP and QE is any indication of their effectiveness, bond investors may have little to worry about rising rates. Interest rates in Japan have been among the lowest in the world for over a decade.

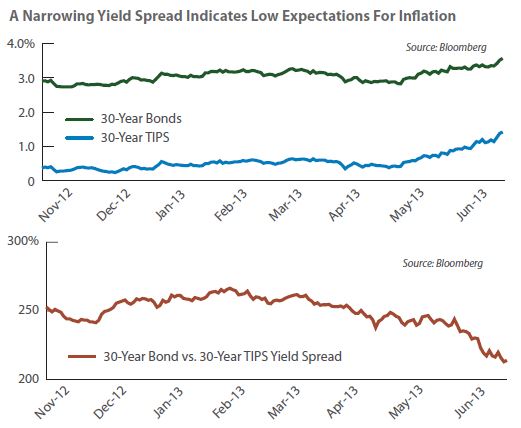

In assessing whether to trim bond allocations, take note of how real rates of return have improved over the last four months. 10-year US Treasury nominal rates have risen0.80% to 2.54% while the Fed’s five-year forward break-even inflation rate has declined0.46%. At the same time, the yield spread between 30-year bonds and 30-year TIPS (a sign of long-term inflation expectations) has also declined from 2.66% to 2.13%.

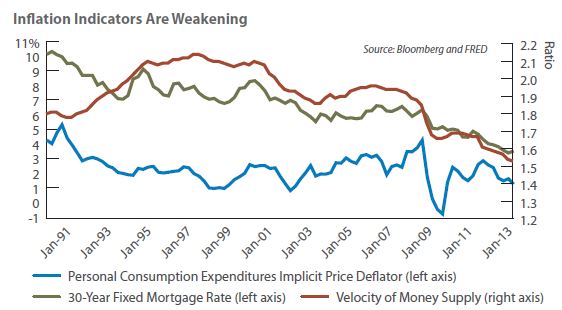

Other indications of inflation expectations, such as the Personal Consumption Expenditure Implicit Price Deflator (a measure of price changes in the personal consumption segment of GDP) and the velocity of money also continue to fall.

30-year fixed mortgage rates tend to follow these measures of inflation closely.

So what about the recent global spike in interest rates? ZIRP may turn out to be the more problematic policy for the Fed. Having kept its 2009 promise to hold short-term rates near zero for years into the future, the Fed has encouraged risk taking around the globe in the form of the “carry trade,” i.e., borrowing funds at virtually no cost (0.25%) and using those funds to buy other higher-yielding assets. As long as the price of the purchased asset remains stable, the position can produce a daily carry profit. If the asset price appreciates, the position can also generate capital gains. Low volatility in the price of the acquired asset is

important if the holder is going to maintain the position, especially when leverage is involved, as it often is.

However, when the purchased asset price fluctuates widely and the asset’s price falls, as with the recent uptick in rates, the accumulated carry can be wiped out and the holder is forced to liquidate the position. During the four years the Fed has maintained ZIRP, hedge funds, banks, and commodity speculators have built huge and profitable carry trades. The recent spike in rates (decline in bond prices) has triggered the liquidation of carry trades all over the world, the unwinding of which puts further downward pressure on prices in a vicious feedback loop. The recent rise in rates may be more a temporary result of this carry trade liquidation cycle than the onset of an economic boom or cyclical rise in rates. The important thing about these types of liquidation events is they are driven more by the mechanics of imbalances (too much money betting the same way, including the average American bondholder) than by economic fundamentals. Occasionally, the imbalances get so large, and the feedback cycle so violent, that general economic activity is curtailed in response (e.g., 2008), but the recent rate spike does not appear to have the potential to create that kind of broader economic whiplash.

Since 2000, US Treasury 10-year notes have experienced seven episodes of rising yields. During those periods yields went up a minimum of 0.76% to a maximum of 1.42%, with an average rise of 1.09%. From the record low of 1.39% set on July 24, 2012, a “normal” rise in rates according to this would leave the US Treasury 10-year note yield at 2.48%, and perhaps as high as 2.81%. The divergent decline in measures of inflation expectations should give investors pause before they accept the notion that “this time” rates are set to march well beyond the levels of other recent episodes.

It is important to revisit the reasons for selecting a particular asset allocation before modifying or abandoning it. Bond investors generally purchase bonds as shock absorbers for riskier portions of their portfolios. This risk dampening effect comes from income and from returns uncorrelated with equity returns. Going forward, capital gains may be less likely, but bonds still offer relatively low volatility, a dependable income stream, and low correlation to returns from common stocks. Replacing bond income with dividend income from common stocks may sacrifice most of the diversifying benefits of bonds for a small increase in yield. Also, equity markets have demonstrated a heightened sensitivity to rising interest rates and have sold off sharply on recent rate spikes. Replacing bond positions with equity positions may compound risks in counterintuitive ways.

The threat of a reversal of QE policies triggering a sudden normalization of yields and an increase in rates is palatable, but we are more likely to see rates move sideways for the next three years. We do not expect 10-year note yields to move up or down more than 1% from a 2.5% fulcrum. US economic growth will continue to improve, but only slightly, while economic growth in the rest of the world will not improve, and may worsen. Deflation remains the dominant influence on rates.

If you believe the Fed’s policies have in fact created a self-sustaining US economic recovery strong enough to offset the deflationary power of faltering economies in Europe, China, Australia, and Japan, then we may have seen the epochal bottom in interest rates. This does not necessarily imply anything more than a normal rise in rates in the foreseeable future. One way to determine whether the economy has really attained escape velocity is to watch how equity prices respond to rising interest rates. If the economy is entering a period of sustained higher growth, job creation, and profits, then equity valuations should remain strong without additional Fed stimulus and absorb the impact of marginally higher rates without a major correction. At this moment, equity markets do not appear that sturdy.

On the other hand, when the US Treasury 10-year note yield (2.54%) exceeds

the dividend yield of the S&P 500 (2.13%), exceeds the Personal Consumption

Expenditure Implicit Price deflator (1.40%), and exceeds the yield spread between 30-year bonds and 30-year TIPS (2.13%), the positive real interest rates embedded in US bond yields may be a fleeting opportunity that has been rare in recent years.

Footnotes

1 Jarrow, Robert; Li, Hao.“TheImpact of Quantitative Easing of the U.S. Term Structure of Interest Rates” Johnson Graduate School of Management, Cornell University, January 23, 2013.

2 Salsman, Richard M.“The Fed’s QE Schemes Have Raised, Not Lowered, T-Bond Yields,” Forbes.com, June 13, 2013. http://www.forbes.com/sites/richardsalsman/2013/06/13/the-feds-qe-schemes-have-raised-not-lowered-t-bond-yields/

3 Hunt, Lacy H.“Debt Deflation/Inflation Debate and the Path to Economic Normalcy.” 2012 Fixed Income Management Conference, CFA Institute, October 10, 2012. http://www.cfainstitute.org/learning/products/multimedia/Pages/77519.aspx

Bonds entail credit risk, because the issuers of the bonds and other debt securities held by a Fund may not be able to make interest or principal payments when due. Even if these issuers are ableto make interest and principal payments, they may suffer adverse changes in financial condition that would lowerthe credit quality of the debt, leading to greater volatility in the price of the security. If the credit quality of a bond is perceived to decline, investors willdemand a higher yield, which means a lower price on that bond to compensatefor the higher level of risk.

Interest ratefluctuations affect bondnot the income received by the Fund from its portfolio securities. Because prices and yields on debt securities vary over time,a Fund's yield also varies. Bonds with embedded callable options also contain an element of prepayment risk. When interest rates decline, issuers can retire![]() their debt and reissue bonds at a lowerinterest rate. This hurts investors because yields available for reinvestment will have declined and upward price mobility on callable bonds is generally limited by the call price.

their debt and reissue bonds at a lowerinterest rate. This hurts investors because yields available for reinvestment will have declined and upward price mobility on callable bonds is generally limited by the call price.

Please consider an investment’s objectives, risks, charges, and expenses carefully before investing. To obtain this and other important information about the Amana, Sextant and Idaho funds in a current prospectus or summary prospectus, please visitwww.saturna.com or call toll free 1-800/SATURNA. Please read the prospectus or summary prospectus carefully before investing.

![]() The Amana, Sextant and Idaho Tax-Exempt Funds are distributed by Saturna Brokerage Services, member FINRA / SIPC. Saturna BrokerageServices is a wholly-owned subsidiary of Saturna Capital Corporation, adviser to the Amana, Sextant and Idaho Tax-Exempt Funds.

The Amana, Sextant and Idaho Tax-Exempt Funds are distributed by Saturna Brokerage Services, member FINRA / SIPC. Saturna BrokerageServices is a wholly-owned subsidiary of Saturna Capital Corporation, adviser to the Amana, Sextant and Idaho Tax-Exempt Funds.

Important Disclaimers and Disclosures

This report is intended only for the information of the reader, and is not to be used for or considered as an offer or the solicitation of an offer to sell

or buy any securities or other financial instruments of any kind, including without limitation, any mutual fund or other product offered, sponsored, created, or managed by Saturna Capital Corporation or its subsidiaries

or affiliates (“Saturna”). This report is not intended for distribution to, or use by, any person or entity who is a citizen or resident of, or located in, any locality, state, country, or other jurisdiction in which such distribution, publication, availability, or use would be contrary to law or regulation or which would subject Saturna to any registration or licensing requirement within such jurisdiction.

This document should not be considered as providing investment advice or services, or any service offered by Saturna. Saturna may not have taken any steps to ensure that the securities referred to in this report are suitable for any particular investor. Saturna will not treat recipients as its customers by virtue of their reading or receiving the report.

Nothing in this report constitutes investment, legal, accounting or tax advice or a representation that any investment or strategy is suitable or appropriate to a particular investor’s circumstances or otherwise constitutes a personal recommendation to any investor. Saturna does not offer advice on the tax consequences of any investment.

All material presented in this report, unless specifically indicated otherwise, is under copyright to Saturna. None of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party, without the prior express written permission of Saturna. Unless otherwise indicated, all trademarks, service marks and logos used in this report are trademarks or service marks of Saturna.

The information in this report was obtained from sources Saturna believes to be reliable and Saturna believes the information and opinions in the material are accurate and complete as of the date of this material. However, information and opinions contained herein will changeover time and without notice. Saturna has no obligation to update or amend any information or opinions at any time. Saturna makes no representations as to the accuracy or completeness of this material, nor does it have any responsibility to ensure that any other materials,

including any containing materially different information, are brought to the attention of any recipient of this report.

![]() Under no circumstances shall Saturna, its employees, or any affiliate, be responsible for any investment decision by any recipient. This material is distributed on condition that it will not form the sole basis or a sufficient basis for any investment decision by any recipient. Any recipient who is not a market professional or institutional investor should seek the advice of an independent financial adviser prior to taking any investment based on this report or for any necessary explanation of its contents.

Under no circumstances shall Saturna, its employees, or any affiliate, be responsible for any investment decision by any recipient. This material is distributed on condition that it will not form the sole basis or a sufficient basis for any investment decision by any recipient. Any recipient who is not a market professional or institutional investor should seek the advice of an independent financial adviser prior to taking any investment based on this report or for any necessary explanation of its contents.

Saturna does not provide tax, legal or accounting advice. Investors should consult their own tax, legal and accounting advisers before engaging in any transaction. In compliance with IRS requirements, recipients are notified that any discussion of U.S. federal tax issues contained or referred to herein is not intended or written to be used for the purpose of (A) avoiding penalties that may be imposed under the Internal Revenue Code; nor (B) promoting, marketing or recommending to another party any transaction or matter discussed herein.

Velocity is a ratio of nominal GDP to a measure of the money supply. It can be thought of as the rate of turnover in the money supply, that is, the number of times one dollar is used to purchase final goods and services included in GDP. The Personal Consumption Expenditure Implicit Price Deflator measures the change in prices paid for goods and services within the personal consumption sector of the U.S. economy. It measures price changes more broadly than the Consumer Price Index, which tracks a specific basket of goods.

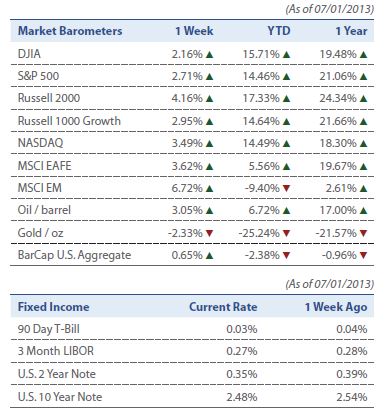

The Dow Jones Industrial Average is a price-weighted index of 30 of the largest, most widely held U.S. stocks. The S&P 500 is an index comprisedof 500 widely held common stocks considered to be representative of the U.S. stock market in general. The Russell 1000 Growth index is a widely recognized index of large-cap growth stocks. The Russell 2000 Indexis comprised of U.S. small cap stocks and measures the performance of the 2,000 smallest U.S. companies in the Russell 3000 Index. The NASDAQ Composite index measures the performance of more than5,000 U.S.and non-U.S. companies traded “over the counter” through The National Association of Securities Dealers Automated Quotation system. MSCI EAFE Index, produced by Morgan Stanley Capital International, measures the equity market performance of developed markets in Europe, Australasia, and the Far East. The MSCI Emerging Markets Index, produced by Morgan Stanley Capital International, measures equity market performance in over 20 emerging market countries. Barclay’s Capital U.S. Aggregate Bond Index measures the performance of theU.S. bond market. All indices shown are widely recognized unmanaged indices of common stock prices which reflect no deductions for fees, expenses or taxes. Investors can not invest directly in the indices.

Past performance does not imply or guarantee future performance, and no representation or warranty, express or implied, is made regarding future performance. The price, and value of, and income from, any of the securities or financial instruments mentioned inthis report can fall as well as rise. The value of foreign securities and financial instruments is subject to exchange rate fluctuation that may have a positive or adverse effect on the price or income of such securities or financial instruments. Investors in securities such as ADRs – the values of which are influenced by currency volatility – effectively assume this risk.

© Saturna Capital