Improved Fed Sentiment Lifts Stocks

Equity markets moved sharply higher in the week, buoyed by comments from Fed Chairman Ben Bernanke and minutes from the Federal Open Market Committee (FOMC) that suggest quantitative easing won’t end anytime in the near future. The S&P 500 rose 3.0% while the Dow Jones Industrial Average climbed 2.2%. After a 20 bps back up on Friday, July 5, the 10 year Treasury fell 12 bps to finish the week yielding 2.61%.

On Wednesday, minutes from the June 18-19 FOMC meeting were released. Markets reacted positively to the transcript, which revealed a committee grappling with how to end its quantitative easing program. Investors were encouraged by the committee’s firmer commitment to contingent accommodation, which will likely extend the duration of the program beyond that seen with an artificial timeline. The group also sought to distinguish decision making around the QE program from its Federal Funds Rate guidance, which it plans to keep near zero as long as unemployment remains above 6.5%.

Also on Wednesday, Ben Bernanke reaffirmed that the Fed would maintain its bond purchases until economic data – particularly in the labor markets – showed signs of significant improvement. In a bid to soothe negative market sentiment, Bernanke also noted that, “highly accommodative monetary policy for the foreseeable future is what’s needed.” The combination of Fed minutes and Bernanke’s comments led to a sharp rally in stocks in the final two days of the week.

Last week marked the official start of corporate earnings season, with reports from Alcoa, J.P. Morgan, and Wells Fargo. Alcoa narrowly beat earnings estimates, while both banks performed better than expected. It should be noted, however, that a major source of J.P. Morgan’s and Wells Fargo’s results were lower loan loss provisions. Still, the reports boosted investor sentiment in an otherwise quiet week of economic data.

On the indicator front, investors had little to digest last week. The few releases scheduled revealed little new information about the US economy.

On Tuesday, the National Federation of Independent Businesses (NFIB) reported that small businesses were more pessimistic in June relative to the month prior. The group’s headline Small Business Optimism Index fell 1.5 points to 93.5, below economists’ expectations.

The majority of the index’s 10 components declined in June, suggestive of broad weakness across the sector. The NFIB index’s sub-100 level remains in recessionary territory, as a lack of small business growth persists as of the most stubborn areas of the US economy. Given the impact of young businesses and startups on job growth, investors should watch this metric closely.

Producer inflation increased 0.8% in June, above forecasts for a 0.5% gain. Higher gasoline prices fed the surge, as fuel costs increased 7.2% during the month following a period of softness. At the core level, producer prices increased 0.2% month-over-month. This was in line with expectations.

With core inflation still contained, there is unlikely to be any alarm bells ringing, despite some warmth at the headline level. Consumer inflation data comes in next week, which is ultimately a more important metric as it relates to Fed policy.

Consumer optimism declined modestly in early July, although it remains near recovery period highs. At 83.9, the index came in slightly below economists’ estimates. While consumers’ attitudes about current conditions actually improved, their future expectations fell. Some of the softness in sentiment may be attributable to the recent rise in gasoline prices. Given the small magnitude of the index change, however, this report was largely a non-event.

Hedge Funds Can Advertise…But Should They?

In April 2012, the Jumpstart Our Business Startups (JOBS) Act was signed into law. The legislation eased a number of regulatory burdens on small businesses and private industry in a bid to boost job growth. The bill made additional headlines for lifting an 80-year ban on solicitation for private placements, the restriction that prevented hedge funds from advertising their wares to the general public.

It was not until this past week, however, that the SEC approved the implementation of this component of the JOBS Act. More than a year overdue, SEC commissioners voted 4-1 to approve the measure as written. A faction of the regulatory group believed the approval of general solicitation opens up investors to fraudulent behavior, causing the measure’s long delay. Following the SEC vote, consumers could see hedge fund ads as soon as October.

Financial pundits seized on the news to go after their favorite punching bag. Mocking slogans such as, “creating alpha since, well, mostly never,” made the rounds in the investment blogosphere, as a bevy of hedge fund cynics questioned what hedge funds could possibly advertise following several years of lackluster performance.

Meanwhile, financial publications publish provocative headlines (and even more unsettling cover pictures) such as last week’s “Hedge Funds are for Suckers” by Bloomberg’s Businessweek. The article rehashes the familiar refrain that hedge funds are too expensive and enrich hedge fund principals at the expense of investors. As last year’s “Hedge Fund Mirage” proved, questioning the value proposition of the alternative investment industry is a surefire way to generate controversy and sell magazines.

A major flaw in the media analysis of hedge funds, however, is that it is entirely return focused. This ignores a major shift in why investors – particularly large institutions – allocate capital to these solutions. While it was true in the 1990’s that investors were primarily seeking excess return, today’s hedge fund participant maintains a keener eye on risk. The primary objective of hedge fund allocations today, for the majority of investors, is to mitigate the potential for capital loss and to generate superior risk-adjusted returns. Survey after survey supports this evolution among hedge fund investors.

Unfortunately, risk-adjusted performance is not sexy. Nor does it fall under the purview of what the common, mainstream investor is seeking. It is unlikely that many average consumers know who William Sharpe is, let alone his eponymous measure of risk-adjusted returns. General hedge fund advertising may fall flat without appropriate education about the objective of alternative investments and context to performance results.

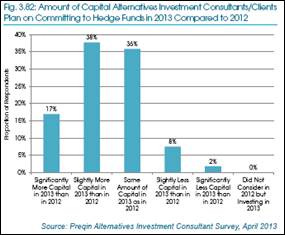

Ultimately, though, it may not matter for the hedge fund industry. As an industry report released by Preqin last week indicates, endowments, foundations, and pension plans are increasingly allocating to alternative investments, and expectations are for that trend to continue. And while advertising rules have changed, the individual wealth requirements for hedge fund investors have not. This suggests no substantial need for broad-scale advertising efforts.

Source: Preqin

It is true that the hedge fund industry, at large, has produced disappointing results in the last few years. However, the inherent flexibility of these products affords them greater opportunity to hedge risks and take advantage of market dislocations. For this reason, hedge funds will always retain a committed investor base. With public scrutiny high though, hedge funds may be wise to stay out of the limelight until the industry firmly regains its footing. Even then, it remains to be seen what advantage is derived from opening up the curtain to anyone beyond sophisticated investors.

The Week Ahead

Corporate earnings will take center stage this week, as major companies such as Citigroup, Coca-Cola, Goldman Sachs, Johnson & Johnson, American Express, Bank of America, eBay, Google, Microsoft, Phillip Morris International, and Verizon Communications report.

On the economic front, several important reports are due, including retail sales, industrial production, consumer prices, and housing starts. Additionally, manufacturing data is released via the Philadelphia and Empire State regional Fed surveys.

Abroad, a range of important economic data concerning China’s economy is due for release. Indicators include second quarter GDP, industrial production, and retail sales. Investors will scrutinize this data closely given fears of a slowdown in the world’s second largest economy.

Only South Africa’s central bank meets this week, although minutes from last week’s Bank of England meeting should reveal any change in stance on the country’s asset purchasing program and its benchmark lending rates. No change is expected.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value

© Fortigent