Global government bonds have performed poorly so far this year. Year to date through July 13, the Barclays Global Treasury Index, which covers 30 investment grade domestic government bond markets, is down 5.5% in unhedged U.S. dollar terms. The same index hedged back to U.S. dollars is down 0.6% year to date. This difference in returns highlights a key point. The source of pain for unhedged investors has been twofold: rising government bond yields and a stronger U.S. dollar. When an investor buys foreign assets they have two choices on the currency risk embedded in those foreign assets — they can keep it or hedge it away. The unhedged and hedged versions of this Global Treasury Index capture these two choices from the perspective of a U.S. based investor.

Abstracting away from the currency question for a moment, the inflection point for global bond markets came on May 3 with the release of a stronger-than-expected non-farm payroll (NFP) report in the U.S. Up to that point, yields had declined in most major markets and the Global Treasury Index had gained 2.2% on a hedged to U.S. dollar basis. The NFP report introduced the risk of an earlier tapering of the Fed’s quantitative easing (QE) program, kicking off the rise in global yields. May 19 comments by Fed Chairman Ben Bernanke that the Fed could end its QE program altogether by mid-2014 just added fuel to the fire.

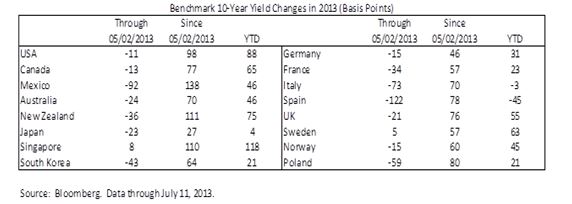

While clearly prompted by developments in the U.S., the government bond rout has been truly global. As shown in the table above, most major bond markets have seen a sharp rise in yields since early May even though economic performance and central bank policy varies widely across countries.

The high correlation in yields across countries — first on the downside and then on the upside — suggests that central bank liquidity and investor sentiment have been the driving forces behind government bond returns this year, rather than local fundamentals. The outsize swings in smaller, less liquid markets paints a similar picture, one of global investors first chasing yield where they could find it, but then rushing for the exits when the liquidity story soured.

For an unhedged U.S. investor, the rise in the U.S. dollar has been even more painful than the rise in global bond yields. Year to date, the U.S. dollar has appreciated 6.6% on a trade-weighted basis. A higher U.S. dollar creates currency losses on non-U.S. assets if left unhedged, and vice versa. The U.S. currency has benefited this year from a growing sense that the U.S. economy is emerging from its post-crisis funk faster than other major economies and the Fed will therefore move sooner than other major central banks to normalize policy. More aggressive easing outside the U.S., notably in Japan, has helped the U.S. currency as well. More broadly, though, the U.S. dollar now appears to be behaving with a pro-cyclical bias, an important shift from 2008-2011 when it behaved with a fairly consistent anti-cyclical bias, (i.e., rallying during growth scares and market crises but then declining again during periods of optimism).

Looking forward, we believe the medium-term trend is toward higher government bond yields, which remain low in a historical context. In the next few months, however, a period of consolidation seems likely. The global economy is still running below trend and lingering slack in the developed economies suggests inflationary pressures will remain muted if global growth accelerates back to a trend-like pace in the year ahead, as we expect. In aggregate, monetary policy is likely to remain very accommodative for the foreseeable future, especially in the advanced economies.

Greater differentiation across markets also seems likely in the short run. The rise in U.S. Treasury yields seems appropriate given the shift in Fed thinking on QE. But the case for a sharp back up in yields outside the U.S. is less clear. For example, the Bank of Japan has embarked on an aggressive quantitative easing effort that will see its balance sheet swell over the next two years as it seeks to root out persistent deflation. And while economic activity in Euro Area appears to be stabilizing as the emphasis on fiscal austerity fades, the outlook remains fairly weak. The Euro Area unemployment rate has risen steadily over the past two years to a record high of 12.2%, suggesting that monetary conditions in the Euro Area as a whole remain far too tight. Pressure on the European Central Bank to do even more will likely grow if the modest recovery we and the consensus now expect fails to materialize.

We remain constructive on the outlook for the U.S. currency over the medium term. The U.S. economy is much further along in the structural healing process than either Europe or Japan and it is becoming increasingly clear that monetary policy will normalize sooner in the U.S. as a result. This looming policy shift has benefited the U.S. dollar at the expense of other major currencies, and we see this trend continuing over the medium-term. The rapid increase in U.S. oil and gas production is another medium-term positive for the U.S. currency. A secular decline in the demand for imported energy should allow the U.S. economy to grow more quickly with less of the negative impact on the country’s external accounts seen in the past.

But we expect the U.S. dollar to experience its share of setbacks along the way. Based on the Bank of England’s nominal effective exchange rate index, the U.S. dollar is already up about 15% from the historic low reached in July 2011, and up almost 7% alone on a year-to-date basis. While still below its long-run averages, the U.S. dollar is no longer as cheap as it once was. Perhaps more important, the first rate hike by the Fed is still one-and-a-half to two years away. Historically, the U.S. has needed to offer a reasonable yield premium at the front end of the curve for the U.S. dollar to appreciate on a sustainable basis. This dollar cycle may well be different thanks to the use of unconventional monetary policy in the U.S., but we would be surprised if the U.S. dollar can march steadily higher before actual short-rate differentials shift materially in the currency’s favor. More likely, the U.S. dollar will see a handful of pullbacks along the way, but we would view these pullbacks as buying opportunities as long as our medium-term thesis about cyclical divergence remains intact.

Disclosure

The views expressed are as of 7/15/13, may change as market or other conditions change, and may differ from views expressed by other Columbia Management Investment Advisers, LLC (CMIA) associates or affiliates. Actual investments or investment decisions made by CMIA and its affiliates, whether for its own account or on behalf of clients, will not necessarily reflect the views expressed. This information is not intended to provide investment advice and does not account for individual investor circumstances. Investment decisions should always be made based on an investor's specific financial needs, objectives, goals, time horizon, and risk tolerance. Asset classes described may not be suitable for all investors. Past performance does not guarantee future results and no forecast should be considered a guarantee either. Since economic and market conditions change frequently, there can be no assurance that the trends described here will continue or that the forecasts are accurate.

This material may contain certain statements that may be deemed forward-looking. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those discussed. There is no guarantee that investment objectives will be achieved or that any particular investment will be profitable.

Investment products are not federally or FDIC-insured, are not deposits or obligations of, or guaranteed by any financial institution, and involve investment risks including possible loss of principal and fluctuation in value.

Securities products offered through Columbia Management Investment Distributors, Inc., member FINRA. Advisory services provided by Columbia Management Investment Advisers, LLC.

© 2013 Columbia Management Investment Advisers, LLC. All rights reserved. 696189