This might just be the cruelest time to be an asset allocator.1 Normally we find ourselves in situations in which at least something is cheap; for instance when large swathes of risk assets have been expensive, safe haven assets have generally been cheap, or at least reasonable (and vice versa). This was typified by the opportunity set we witnessed in 2007.

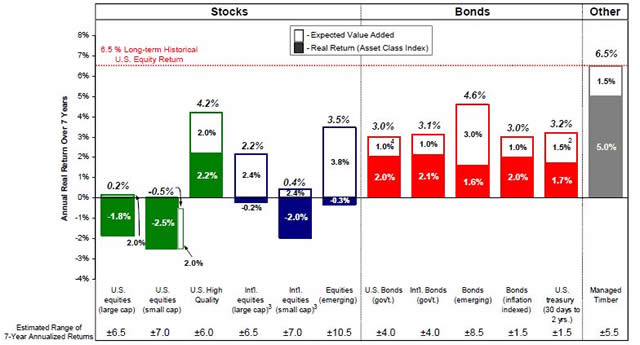

Exhibit 1

GMO 7-Year Asset Class Real Return Forecasts*

As of September 30, 2007

* The chart represents real return forecasts for several asset classes and not for any GMO fund or strategy. These forecasts are forward-looking statements based upon the reasonable beliefs of GMO and are not a guarantee of future performance. Forward-looking statements speak only as of the date they are made, and GMO assumes no duty to and does not undertake to update forward-looking statements. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties, which change over time. Actual results may differ materially from those anticipated in forward-looking statements. US inflation is assumed to mean revert to long-term inflation of 2.2% over 15 years.

Source: GMO

- 1 Long-term inflation assumption: 2.5% per year.

- 2 Alpha transported from management of global equities.

- 3 Return forecasts for international equities are ex-Japan.

Likewise, during the TMT bubble of the late 1990s, the massive overvaluation of certain sectors was offset by opportunities in “old economy” stocks, emerging market equities, and safe-haven assets.

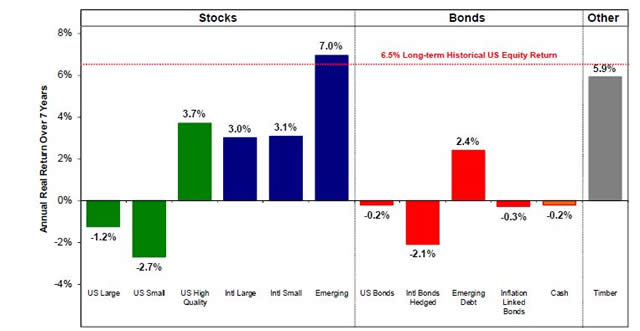

However, today we see something very different. As Exhibit 2 shows, today’s opportunity set is characterized by almost everything being expensive. As I noted in “The 13th Labour of Hercules,”2 this is a direct effect of the quantitative easing policies being pursued by the Federal Reserve and their ilk around the world.

Exhibit 2

GMO 7-Year Asset Class Real Return Forecasts*

As of June 30, 2013

- The chart represents real return forecasts for several asset classes and not for any GMO fund or strategy. These forecasts are forward-looking statements based upon the reasonable beliefs of GMO and are not a guarantee of future performance. Forward-looking statements speak only as of the date they are made, and GMO assumes no duty to and does not undertake to update forward-looking statements. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties, which change over time. Actual results may differ materially from those anticipated in forward-looking statements.

US inflation is assumed to mean revert to long-term inflation of 2.2% over 15 years.

Source: GMO

The Fed has been unusually transparent in explaining its thoughts on the impact of quantitative easing. Brian Sack of the New York Fed wrote in December of 2009 (bold emphasis added):

A primary channel through which this effect takes place is by narrowing the risk premiums on the assets being purchased. By purchasing a particular asset, the Fed reduces the amount of the security that the private sector holds, displacing some investors and reducing the holdings of others. In order for investors to be willing to make those adjustments, the expected return on the security has to fall. Put differently, the purchases bid up the price of the asset and hence lower its yield. These effects would be expected to spill over into other assets that are similar in nature, to the extent that investors are willing to substitute between the assets. These patterns describe what researchers often refer to as the portfolio balance channel.

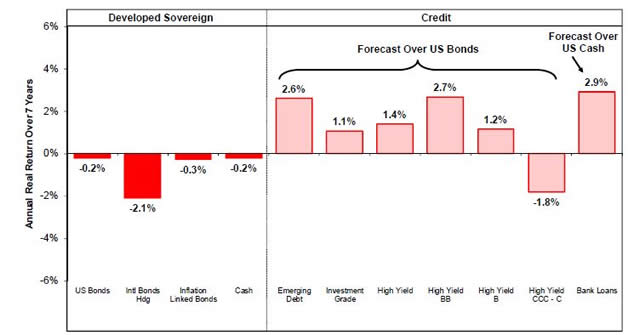

Market participants have (at least until the last month) reacted to this situation by “reaching for yield” as witnessed by the more detailed fixed income forecasts in Exhibit 3. This could be described as a “near rational” bubble (inasmuch as investors are reacting to the very low cash returns, which they expect to last for a long time). I’ve described it as a “foie gras” bubble as investors are being force-fed higher risk assets at low prices.3 The bad news is that reaching for yield rarely ends well.

Exhibit 3

GMO 7-Year Fixed Income Forecasts*

As of June 30, 2013

- The chart represents real return forecasts for several asset classes and not for any GMO fund or strategy. These forecasts are forward-looking statements based upon the reasonable beliefs of GMO and are not a guarantee of future performance. Forward-looking statements speak only as of the date they are made, and GMO assumes no duty to and does not undertake to update forward-looking statements. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties, which change over time. Actual results may differ materially from those anticipated in forward-looking statements.

U.S. inflation is assumed to mean revert to long-term inflation of 2.2% over 15 years.

Source: GMO

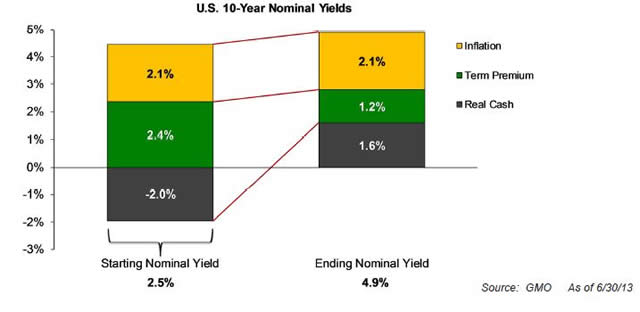

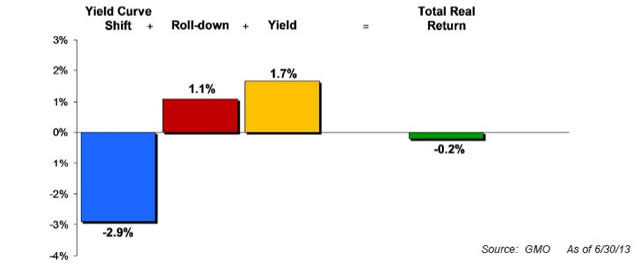

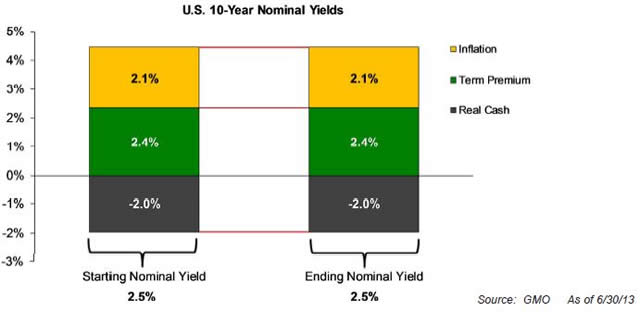

Of course, like all of our published forecasts, the forecasts for government bonds and cash assume mean reversion. That is to say that when constructing our forecasts, we follow a pattern such as the one shown in Exhibit 4.4 Effectively, this forecast says that real cash rates will mean-revert toward something close to long-term average, the slope of the yield curve will move to its long-term average, and inflation will move to the consensus view of long-term inflation (in the absence of a strong view on the future path of inflation). As even a cursory glance at the exhibit shows, the main driver of our negative view on treasuries is the impact of real rates normalizing from -2% to 1.6% over the course of 7 years.5

To convert this into a 7-year forecast we need to acknowledge the various components: the shift in the yield curve; the real yield; and the roll down (from having a 10-year bond that after 1 year becomes a 9-year bond, and thus to ensure constant maturity, you sell and reinvest in a new 10-year bond). Under our baseline assumptions (i.e., those shown in Exhibit 4), this gives rise to the forecast shown in Exhibit 5.

Exhibit 4

Yield Decomposition for U.S. Treasuries

Exhibit 5

U.S. 10-Year: Building a 7-Year Forecast

A GMO Heresy: The Possibility of No Mean Reversion!

As regular readers will know, we at GMO are stalwart supporters of the concept of mean reversion in general.6 However, if ever there was an economic case for a question mark over mean reversion, it is surely with respect to cash rates and bond yields. The simple reason behind this seemingly heretical statement is that rates are (can be) policy instruments. As Keynes7 noted, “The monetary authorities can have any interest rate they like… They can make both the short and long-term [rate] whatever they like, or rather whatever they feel to be right… Historically the authorities have always determined the rate at their own sweet will.”

We are all used to thinking of central banks as setting the short-term interest rates, but generally the long rate is seen as a market-determined rate (i.e., some combination of market expectations of future short rates, liquidity preference, and risk premiums). However, there is nothing to stop central banks from setting the long rate as well. Indeed, in the past they have done exactly that (e.g., the UK during World War II had a target of 3% for bond yields). So bond yields can be an outright policy instrument too.

The Myth of the Bond Vigilantes

When I’m talking to people about this, it is at this point that someone usually brings up the bond vigilantes: surely these guardians of monetary and fiscal rectitude will step in. However, for a nation that can print its own currency and has a floating exchange rate, bond vigilantes are a myth – an economic bogey man made up to scare recalcitrant governments into “good” behaviour.

Just imagine that I as a foreigner decide to sell my holdings of U.S. government bonds. If the Federal Reserve stands ready to buy at the same yield at which I sell, there will be precisely zero impact on yields, i.e., I sell at, say, 2.5% and the Fed buys those same bonds at 2.5%. The only impact is that the dollar will go down against the pound as I switch from holding a dollar asset to holding sterling.

This, of course, assumes that the central bank targets price (i.e., has a desired bond yield) and doesn’t care about the exchange rate. As an aside (to me, at least), one of the oddities in the process of quantitative easing is that it is “quantitative” rather than price-based. Presumably, the Fed and its brethren think they can do more than simply lower rates by using the “quantitative” approach. I’m just not sure what. To me, a combination of a price/yield target for treasuries and a quantitative easing policy for other assets (such as MBS) would be the easiest and most logical way to move beyond the zero bound on short rates. A price target is certainly easier to exit as you simply raise the yield target to your new desired level. The good news is that policy making is well above my pay grade!

The Myth of the “Natural” Rate

An alternative argument that gets put forward is that the Fed can’t really set any rate that it likes because, ultimately, it must respect the “natural rate of interest.” One should always be suspicious of the word “natural” in the context of economics. It tends to imply some semi-divine concept, yet there are essentially no natural laws in economics.

The concept of the “natural” rate dates back to early monetary theorists but was given maximum exposure in the works of the Swedish economist, Knut Wicksell.8 However, there are several arguments that I find compelling and believe cast serious doubt on the concept of a “natural” rate of interest. The arguments over the existence of a natural rate of interest are generally what can only be described as “wonkish”9 and thus I won’t subject the reader to an elongated discussion here. For those (geeks, nerds, and anyone with trouble sleeping) who are interested, I’ve written a wonkish addendum to this piece called “Wicksell’s Red Surströmming.”

Rather than a single, divine “natural” rate, I’d suggest it might be more helpful to think of a range of neutral or consistent rates. (As Keynes put it, “It cannot be maintained that there is a unique policy which, in the long run, the monetary authority is bound to pursue.”10 For instance, a price stability consistent interest rate might be defined as the rate of interest consistent with stable prices (akin to inflation targeting, the darling of central bankers around the globe), a full employment11 consistent interest rate would aim to reduce unemployment to levels that were essentially frictional, and one can easily posit a financial stability consistent interest rate that kept financial markets well-behaved.12

The chance of these various rates all coinciding is essentially zero. Trying to achieve all three outcomes with a single policy instrument (short-term interest rates) is likely to be an impossible task. Thus, some political guidance as to the relative merits of the various objectives is needed, or more instruments available to be called upon.13

This, of course, simplifies away from the problem of actually knowing what these various rates are. What level of rates ensures price stability? What level of rates ensures full employment? And so on. This is certainly well beyond my ken, and I suspect an unknown for the central bankers as well. To really add salt to the wound, these various rates are highly likely to be time-varying as well. Hence, trying to identify any one of these rates is akin to looking for a needle in a haystack, with the added complication that someone keeps moving the entire haystack!

Fixed Income Forecasts in a World without Mean Reversion

Anyway, back to forecasting. The bottom line is that it is perfectly possible that the Fed, et al, could hold rates down (at both the long and short end) for some prolonged period. This is obviously an exceptionally bullish case for bonds (in fact, I’d argue it was the “best” case outcome that could reasonably be expected, absent a strongly deflationary viewpoint).

It is easiest to see how this would play out by thinking about the buy and hold return to owning a 10-year treasury. Currently, such an investment yields around 2.5% p.a. in nominal terms. If we were to hold such a bond for its lifetime, then we would simply end up with a real return equal to the current yield minus the inflation rate (say, 2.3%14), i.e., close to a zero real return.

Exhibit 6

No Mean Reversion in Yields

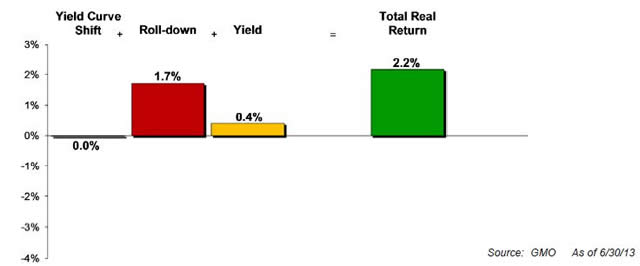

However, as noted above, if we pursue a constant maturity strategy (i.e., when our 10-year bond becomes a 9-year bond, we sell it and reinvest in a new 10-year bond), a rolldown return is created (assuming a normal upward-sloping yield curve). This would translate into a 7-year forecast in an identical fashion to that noted earlier and as represented in Exhibit 7. Effectively, rather than the -0.20 bps forecast we see under the baseline assumption of mean reversion, we would get a forecast of 2.2% p.a.15

This might seem like a reasonable rate of return. However, it only holds if and only if the Fed keeps rates unchanged in real terms over the next decade. As I showed in my previous work on equities under financial repression (“The 13th Labour of Hercules”), the way you behave and your estimates of return are driven by your expectation of the duration of financial repression.

Exhibit 7

Impact on Return Generators of No Mean Reversion

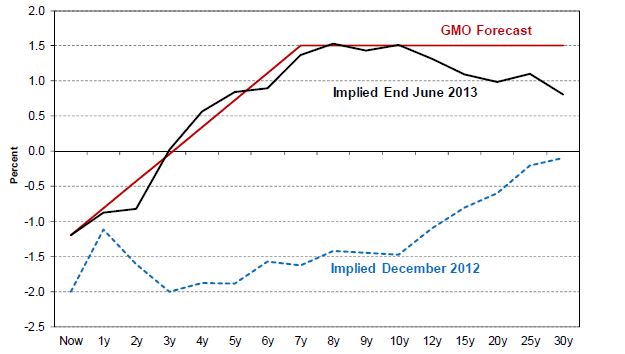

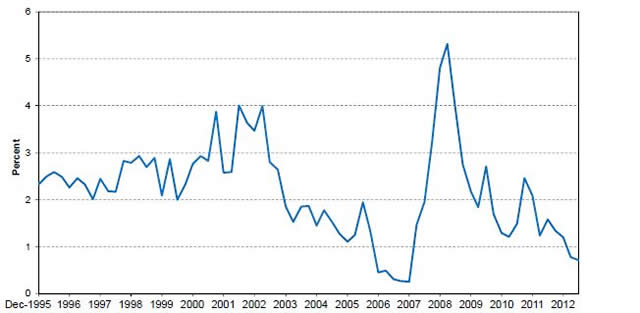

However, as I also pointed out in previous musings on financial repression, as far as I can tell, no one has any real idea how long the Fed (and others) will keep rates low. The market’s implied view has certainly changed radically over the last six months as Exhibit 8 shows. In essence, the Fed spoke of “tapering” and Mr. Market heard “tightening.”

For what it is worth (and I assure you it isn’t a lot), I think that given that the Fed merely mentioned the possibility of tapering its quantitative easing policies, this seems like a probable over-reaction, especially since the Fed is explicitly following a so-called “Evans Rule” and is committed to keeping policy easy until the unemployment rate reaches 6.5% (currently at 7.5% with low participation rates) or inflation (based on the PCE) exceeds 2.5% (currently at 1%). A tapering of the quantitative easing policies seems like a very different thing than the Fed embarking on an explicit interest rate tightening cycle.

Exhibit 8

Implied Real Short Rates

The chart represents a real return forecast for the above named asset class and not for any GMO fund or strategy. These forecasts are forward-looking statements based upon the reasonable beliefs of GMO and are not a guarantee of future performance. Forward-looking statements speak only as of the date they are made, and GMO assumes no duty to and does not undertake to update forward-looking statements. Forward-looking statements are subject to numerous assumptions,risks, and uncertainties, which change over time. Actual results may differ materially from the forecasts above.

Source: GMO As of 6/30/13

Given the massive uncertainty surrounding the duration of financial repression, it is always worth considering what happens if you are wrong. In owning treasuries under the assumption that the Fed holds real cash rates negative, you get the roll return as above, but this could be described as a “pennies in front of a steamroller” style strategy. It is always possible that the Fed could decide to step away from the market or normalize real rates and you would end up with a return more akin to the baseline mean reversion forecast we presented above. You are effectively running a strategy that potentially has significant tail risk embedded within. One of the most useful things I’ve learnt over the years is to remember that if you don’t know what is going to happen, don’t structure your portfolio as though you do!

The bottom line is that treasuries offer low returns under most scenarios. If the Fed steps away from the market and normalizes, you get a negative return; if the Fed stays in the market, you get a pretty low return. You are pretty much doomed either way. The only scenario under which treasuries do “well” is one with outright deflation! In essence, in the absence of a strong view on deflation, you neither want to be long, nor short, treasuries. You just don’t want to own any.

The Death of an Asset Class?

I am well aware of the dangers of proclaiming the death of an asset class, because usually when this is announced, we witness an enormous bull market in the supposedly dead asset class. However, barring the deflation outcome, we could finally be witnessing what Keynes described as the euthanasia of the rentier:

“The owner of capital can obtain interest because capital is scarce, just as the owner of land can obtain rent because land is scarce. But whilst there may be intrinsic reasons for the scarcity of land, there are no intrinsic reasons for the scarcity of capital… I see… the euthanasia of the rentier.”16

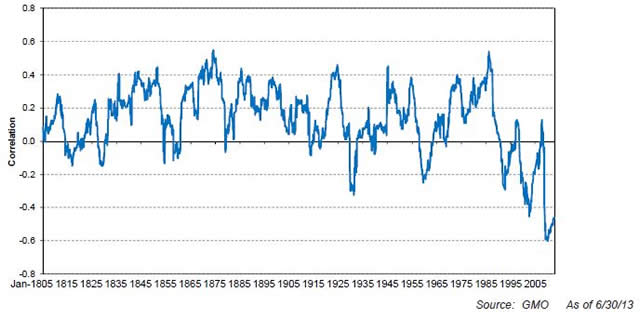

Assuming you aren’t expecting outright deflation, then the best that can be said for owning some treasuries is that they act as diversification/insurance in the context of an equity portfolio. However, as Exhibit 9 shows, the correlation between bonds and equities isn’t exactly stable – it wanders all over the place, and on average is positive! Certainly it is negative during a subset of events that are probably best described as deflationary busts (e.g., 1930s, 2008). So if this is the risk you are worried about, then perhaps you should own some fixed income. However, it isn’t obvious just how much of a diversifier bonds can be at very low yields.17 Nor do bonds act as diversifying assets to events like the stagflation of the 1970s. Ultimately, if you own bonds as insurance you must ask yourself how much you are paying for that insurance, because insurance is as much a valuation-driven proposition as anything else in investing.

Exhibit 9

Correlation of Bond and Equity Returns (Rolling 5-Year)

The Purgatory of Low Returns

Of course, bonds aren’t the only low-returning asset class. As Exhibit 2 showed, the current opportunity set according to our forecasts is generally not compelling. To us, both bonds and equities generally look to be “overvalued.” Those focusing on the “attractive level of the equity risk premium” potentially fail to recognize this situation.

If the opportunity set remains as it currently appears and our forecasts are correct (and I’m using the mean-reversion- based fixed income forecast), then a standard 60% equity/40% fixed income strategy is likely to generate somewhere around a paltry 70 bps real p.a. over the next 7 years!18 Even if we used the non-mean-reversion-based forecast, the 60/40 portfolio looks likely to generate a lowly 1.7% p.a. real. Thus, if the opportunity set remains constant, investors look doomed to a purgatory of low returns.

Exhibit 10

60/40 Forecast Real Returns over Time

Each data point represents GMO’s forecast for a 60%(S&P 500)/40%(U.S. Bonds) portfolio. These forecasts are forward-looking statements based upon the reasonable beliefs of GMO. Past forecasts were not, and current forecast are not, a guarantee of future performance. Forward-looking statements speak only as of the date they are made, and GMO assumes no duty to and does not undertake to update forward-looking statements. Forward-looking statements are subject to numerous assumptions, risks, and uncertainties, which change over time. Actual results may differ materially from those anticipated in forward-looking statements.

Source: GMO As of 6/30/13

So what is an investor to do? I believe there are at least four (possibly not mutually exclusive) paths an investor could go down to try to avoid this outcome:

- Concentrate. Simply invest in the highest-returning assets. This is obviously risky as you become dependent upon the accuracy of your forecasts, and right now nothing is outstandingly cheap so you are “locking in,” at best, fair returns (assuming you wanted to have a portfolio that was 100% invested and split between, say, European value and emerging market equities). You are, however, giving up the ability to rebalance.

- Seek out alternatives. This meme had been popular until the GFC revealed for all to see that many alternatives were anything but alternatives. True alternatives may be fine, but they are likely to be few and far between.

- Use leverage. This is the answer from the fans of risk parity. Our concerns about risk parity have been well documented.19 As a solution to a low-return environment, leverage seems like an odd choice. Remember that leverage can never turn a bad investment into a good one, but it can turn a good investment into a bad one (by forcing you to sell at just the wrong point in time).

- Be Patient. This is the approach we favour. It combines the mindset of the concentration “solution” – we are simply looking for the best risk-adjusted20 returns available, with a willingness to acknowledge that the opportunity set is far from compelling and thus one shouldn’t be fully invested. Ergo, you should keep some “powder dry” to allow you to take advantage of shifts in the opportunity set over time. Holding cash has the advantage that as it moves to “fair value” it doesn’t impair your capital at all.

Of course, this last approach presupposes that the opportunity set will shift at some point in the future. This seems like a reasonable hypothesis to us because when assets are priced for perfection (as they generally seem to be now), it doesn’t take a lot to generate a disappointment and thus a re-pricing (witness the market moves in the last month). Put another way, as long as human nature remains as it has done for the last 150,000 years or so, and we swing between the depths of despair and irrational exuberance, then we are likely to see shifts in the opportunity set that we hope will allow us to “out-compound” this low-return environment. As my grandmother used to chide me, “Good things come to those who wait.”

Wicksell’s Red Surströmming (A Wonkish Addendum)1

The concept of a “natural” rate of interest is ubiquitous in modern finance and in discussions about monetary policy (i.e., the Fed’s rates are too low, too high, etc). Effectively, inflation/deflation is said to be caused by a gap between the “natural” rate and the policy-determined rate. However, I fear the concept of a “natural” rate of interest is ill- defined and probably doesn’t exist at all (outside of some extremely restrictive models, of interest only to academics).

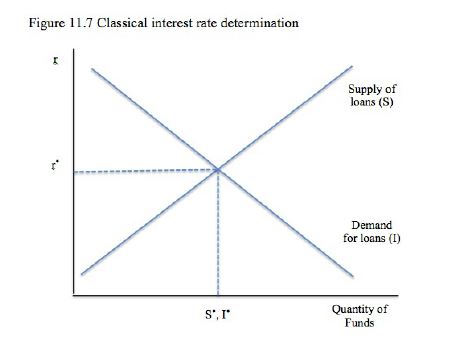

As noted in the main essay, the concept of the “natural rate of interest” was given its most expansive representation in the works of Knut Wicksell (especially Wicksell 1898). He argued that the natural rate of interest “is obtained by thinking of it as the rate which would be determined by supply and demand if real capital were lent without the intervention of money.” By real capital, Wicksell is referring to machines, tools, etc. In more general terms, the approach is usually summed up by a diagram such as the one below (aka Robertson’s loanable funds market).

The supply of loans is the savings curve, and the demand of loans is the investment curve. These curves are held to be determined by real forces such as productivity and thrift. Thus the natural rate of interest is argued to be independent of “monetary factors.” Ben Bernanke certainly subscribes to this view. In a recent speech2 he opined, “In the longer term, real interest rates are determined primarily by nonmonetary factors.” Similarly, the current darling of the Fed and “central banking guru,” Michael Woodford, is a self-confessed “neo-Wicksellian” whose magnum opus shares the title of Wicksell’s 1898 book, InterestandPrices.

However, there are some fundamental issues with this framework. We can see a simple example by considering the following: let’s take a private closed economy (i.e., no government, no trade).

Output (Y) can be defined as consumption © plus investment (I) Y = C + I

If we accept that output equals income, then we can also define Savings (S) is equal to all income (Y) not consumed or

S = Y - C

This can be rewritten as Y = C +S

At this point it becomes obvious that S = I.

This is an identity: it has to be true at all points in time and with all interest rates! In terms of the loanable funds diagram shown above, this effectively says the investment and saving lines are one and the same thing (just viewed from different angles). They are really just one line. Thus, they can’t determine the “natural rate of interest.”

The neoclassical economists (such as Myrdal and Ohlin) argued that the S=I identity was not a problem because it was an ex post statement, and the loanable funds framework was an ex ante analysis – i.e., it was about planned savings and planned investment. It was said that these planned levels were equilibrated by the real rate of interest. Under this view, both saving and investment are seen as volitional decisions of individual savers and investors.

This may be true under a very specific model of the economy – one in which we are all farmers! Chick3 notes “Classical theory had its beginnings in the setting of an agricultural economy, where the archetypal form of saving was the seed-corn; production not consumed, a real resource. (Being real [and highly divisible], there is no problem of aggregation.) Income, the harvest, is predetermined. When corn is held back from consumption, it is saving; when sown, investment. The saving is done (slightly) prior to the investment in the nature of things and is only done for the purpose of investment.” In this type of economy saving does indeed proceed investment, and conforms to the loanable funds approach.

This is a typical example of what Schumpeter4 terms “real analysis” (in which money is a veil):

Real Analysis proceeds from the principle that all essential phenomena of economic life are capable of being described in terms of goods and services, of decisions about them, and of relations between them. Money enters the picture only in the modest role of a technical device that has been adopted in order to facilitate transactions.

However, whilst the loanable funds approach may hold for a single-commodity agricultural economy, the conclusions don’t extend to more complex economies. We then need to turn to “monetary analysis,” in which monetary variables are not considered an essentially redundant veil, but rather as fundamental from the start:

Monetary Analysis introduces the element of money on the very ground floor of our analytical structure and abandons the idea that all essential features of economic life can be represented by a barter-economy model. Money prices, money income, and saving and investment decisions bearing upon these… acquire a life and importance of their own, and it has to be recognized that essential features of the capitalist process may depend upon the ‘veil’ and that the ‘face behind it’ is incomplete without.

In Chick5 an evolution of banking in “stages” is outlined. The second stage is characterized by widespread acceptance of deposits as money for transactions. “The banking system can now lend to a multiple of reserves, subject to… reserve requirements; deposits are a consequence.” Effectively, loans now create deposits. Banks decide to make loans based on expected profitability and the creditworthiness of borrowers. This means that investment can now proceed saving. As Moore6 puts it, savings simply becomes the accounting record of investment.

Under this framework, saving is no longer volitional. Under a monetary analysis, all investment spending must be financed, but it can be financed in one of two ways, either via internal finance or external finance. When investment is financed by internal means, the money to finance must first have been saved. When investment is financed externally, the accompanied savings may be volitional or non-volitional. When the external finance takes the form of issuing new stocks or bonds, then this represents an increase in volitional saving. When the external finance is via bank loans, then the saving is non-volitional (since it need not involve any decision to abstain from consumption). Deficit spending, deficit finance, and non-volitional saving cannot occur in nonmonetary economies and thus are missed by those following a “real analysis path.”

Above we defined savings as income not consumed. Moore points out that a more transparent definition is “net wealth accumulation.” He notes:

If income is not spent on consumption goods it must necessarily be spent on or held in the form of non- consumption goods. When individuals “save” their net worth increases… when saving is defined as the change in net worth, it can very easily be seen to simply be the accounting record of investment.

Moore suggests looking at the National Balance Sheet (Table 1). Changes in tangible assets must create changes in net worth. Thus “saving” is the accounting record of investment.

Table 1

|

National Balance Sheet |

|

|

D Financial Assets XX |

D Financial Liabilities XX |

|

D Tangible Assets XX |

D Net Worth |

|

(Investment) |

(Savings) |

We can then say that investment causes savings. With the exception of unplanned inventory accumulation, all decisions to invest are volitional. In contrast, most saving behaviour is non-volitional. Planned savings by households will almost never equal planned investment by firms (except by extreme accident). Hence, the precepts of the loanable funds approach must be rejected and there is no such thing as the “natural rate of interest.”

The Cambridge Capital Controversies

If that wasn’t enough wonkishness for you, there is another problem with the “loanable funds” approach to the natural rate of interest. It dates back to an intellectual dispute that raged in the 1950s/60s between Cambridge UK (with Robinson, Kaldor, Sraffa, and Pasinetti among the combatants) and Cambridge USA (represented by Solow, Samuelson, Hahn, and Bliss).

The war was effectively opened by the following salvo from Joan Robinson:7

The production function has been a powerful instrument of mis-education. The student of economic theory is taught to write Q = f(L,K) where L is a quantity of labour, K a quantity of capital and Q a rate of output of commodities. He is instructed to assume all workers are alike, and to measure L in man-hours of labour; he is told something about the index-number problem in choosing a unit of output; and then he is hurried on to the next question, in the hope that he will forget to ask in what units K is measured. Before he ever does ask, he has become a professor, and so sloppy habits of thought are handed on from one generation to the next.

In standard neo-classical economics, the production function Q=f(L,K) is coupled with a handful of further assumptions such as exogenously given resources and technology, constant returns to scale, diminishing marginal productivity, and competitive equilibrium. From this, what Samuelson8 called the three parables can be derived:

- The real return on capital (the rate of interest) is determined by the marginal productivity of capital.

- A greater quantity of capital leads to a lower marginal product of capital/lower interest rate (also holds with respect to capital/output ratio and the sustainable levels of consumption per capita).

- The distribution of income between labour and capital is explained by relative factor scarcities and marginal products.

As with Wicksell’s original statements about real capital (above), all is good and well in a single-commodity example. However, when one generalizes, things begin to go awry. Heterogeneous capital goods can’t be aggregated in physical units9 (semi-conductors and spades don’t share a common unit of account in physical terms). Hence they are required to be valued in some terms; generally this is done with reference to the present value of output they are capable of producing (i.e., some form of discounted cash flow analysis). This, of course, involves an interest rate, and here the whole thing collapses into circularity – you can’t get a rate of interest without knowing the value of capital and you can’t know the value of capital without an interest rate. As Sraffa10 (1962) put it, “What is the good of a quantity of capital… which, since it depends on the rate of interest, cannot be used for its traditional purpose… to determine the rate of interest.”11

Sadly, although the Cambridge UK team won the battle as even Samuelson admitted the three neo-classical parables “cannot be universally valid,” the Cambridge USA team won the war12 given the aggregate production function and the loanable funds theory are still drummed into unsuspecting students’ heads without any discussion of the issues raised by the Cambridge Capital Controversies.

Conclusion

The idea of a natural rate stems from models that are appropriate to the most basic form of economy, but that simply do not translate into models of more complex economies. The identity nature of S=I combined with the reality of a modern financial system and the problems raised by the Cambridge Capital Controversies all add up to very good reason for doubting the existence of a natural rate of interest. I would go as far as to say that the natural rate of interest is a myth.

1 It is certainly a bad time to be writing a paper on bonds, given that I seem to be revising the numbers almost every day!

2 James Montier, “The 13th Labour of Hercules: Capital Preservation in the Age of Financial Repression,” November, 2012. A white paper available, with registration, at www.gmo.com.

3 Of course, investors always have a choice not to participate by simply sitting on the sidelines. However, this option is often not viable for many because “career risk” dominates. This innate tendency to be invested is, of course, severely exacerbated when sitting on the sidelines carries the price tag of a nega- tive real return.

- 4 The framework for constructing bond forecasts is based on the work of several of my colleagues including Edmund Bellord, Nick Nanda, and Kai Wu. They have each forced me to think much more deeply about bonds.

5 It is perfectly possible that over the next 10 years we may end up with a cash rate that is lower than 1.6% because of the policies the world’s central banks are pursuing.

7 John Maynard Keynes, Collected Writings (Volume XXVII), Cambridge University Press, December 1980.

8 Knut Wicksell, InterestandPrices, 1898.

9 Indeed, when I wrote up some of these arguments internally even a couple of my more tolerant colleagues suggested they were excessively wonkish.

- 10 From Keynes Lectures 1932 (via Rymes [1989] Keynes’s Lectures, 1932-35).

11 Defined as frictional unemployment and zero underemployment with participation rates at high levels.

12 One could plausibly argue that the recent pronouncements by the Fed over the possibility of tapering were driven more by concern about the behaviour of financial markets than the underlying state of the economy.

13 For instance, using fiscal policy to target full employment.

14 Both the inflation swaps market and the Philadelphia Fed Survey show around this level of expected inflation over the next 10 years.

15 This work was first presented by Edmund Bellord at our client conference in the fall of 2012.

16 John Maynard Keynes, TheGeneralTheoryofEmployment,InterestandMoney, MacMillan Cambridge University Press, 1936.

17 Again, assuming no deflation.

18 This uses a global equity (40% U.S./40% International/20% Emerging) forecast.

19 See Ben Inker’s white paper of March 2010, “The Hidden Risks of Risk Parity Portfolios” at www.gmo.com, with registration.

- 20 Of course, when we say risk we don’t mean volatility, beta, or VaR. Rather, we are driving at an assessment of the “fundamental risk” of an investment.

1 Surströmming is a Swedish “delicacy” that consists of putrefied herring.

2 http://www.federalreserve.gov/newsevents/speech/bernanke20130301a.pdf

3 Victoria Chick, MacroeconomicsAfterKeynes:AReconsiderationoftheGeneralTheory, The MIT Press, 1983.

4 Joseph Schumpeter, HistoryofEconomicAnalysis, Oxford University Press, USA, 1954.

5 Victoria Chick, “The Evolution of the Banking System and the Theory of Saving, Investment and Interest,” discussion paper, University College of London, Dept. of Economics, 1992.

- 6 Basil Moore, ShakingtheInvisibleHand:Complexity,ChoiceandCritiques, Palgrave Macmillan, 2006.

7 Joan Robinson, “The Production Function and the Theory of Capital,” Review of Economic Studies, 21(2), 1953-54, pp. 81-106.

8 Paul Samuelson, “A Summing Up,” The Quarterly Journal of Economics, Vol. 80, No. 4, November 1966.

9 Wicksell himself was aware of this problem, which he detailed in 1911. “Whereas labour and land are measured each in terms of its own technical unit (e.g., working days or months, acre per annum) capital… is reckoned… as a sum of exchange value – whether in money or as an average of products. In other words, each particular capital-good is measured by a unit extraneous to itself.”

- 10 Piero Sraffa, ProductionofCommoditiesbyMeansofCommodities:PreludetoaCritiqueofEconomicTheory, Vora & Co., 1960.

11 Interestingly (well, to me anyway) the eventual neoclassical end point of general equilibrium models also finds that the three parables can’t be extended outside of the simple, one-commodity good environment.

12 It should be noted that one of the reasons that the Cambridge UK group stopped poking holes was due to its literal demise: of the group only Pasinetti is still going, with both Robinson and Sraffa dying in 1983, and Kaldor in 1986.

Mr. Montier is a member of GMO’s Asset Allocation team.

Disclaimer: The views expressed herein are those of James Montier as of July 22, 2013 and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2013 by GMO LLC. All rights reserved.

© GMO