Investors are piling into U.S. Stocks with July only a little half over. Read this investor insight by TrimTabs Asset Management to learn more about the recent uptick in U.S. Equities and other detailed supply and demand activity with the stock market at the start of Q3.

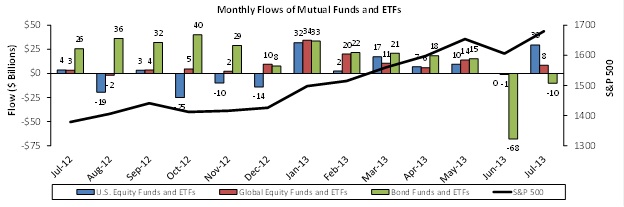

Inflow of $29.6 Billion into U.S. Equity MFs and ETFs in July Already Seventh-Highest Monthly Inflow on Record.

Investors are pouring massive sums into U.S. equities, which should make contrarians wary of this market at least for the near term. A staggering $29.6 billion has flowed into U.S. equity mutual funds and exchange-traded funds this month ($7.4 billion into U.S. equity MFs and $22.2 billion into U.S. equity ETFs). U.S. equity ETFs have posted nine consecutive daily inflows, and eight of those nine daily inflows exceeded $1.5 billion.

Source: TrimTabs Investment Research

Past performance is not indicative of future results.

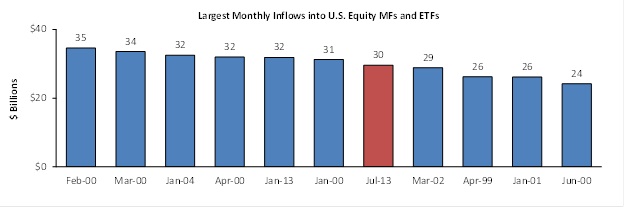

July is only about half finished, yet this month's inflow into U.S. equity funds is already the seventh-highest on record. Note that four of the six larger monthly inflows occurred at the top of the technology bubble in early 2000.

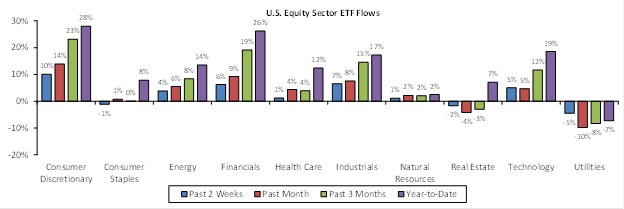

Investors Flock to Risk amid July Market Meltup. Consumer Discretionary, Industrials, and Financials Most Popular Sectors in Past Two Weeks.

ETF investors flocked to higher-beta sectors amid the stock market melt-up in early July. Consumer Discretionary, Industrials, and Financials were most popular, each issuing at least 5% of assets in the past two weeks. By contrast, the only sectors that posted outflows were Consumer Staples, Real Estate, and Utilities. Utilities lost 5% of assets even though the average fund was up 3.0%.

So far this year, Consumer Discretionary and Financials have been the clear flow winners, each taking in more than 25% of assets. The only sector to post an outflow has been Utilities, which has lost 7% of assets.

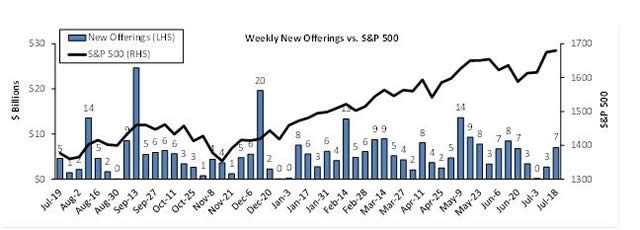

New Offering Calendar Picks Up Steam: Dealogic Reports $2.8 Billion Scheduled for Wednesday and $1.3 Billion Scheduled for Thursday. NRG Yield IPO Surges on First Day of Trading.

Underwriters are starting to take advantage of the rally to unload more new shares. They priced $2.0 billion from 7/12/13 through 7/16/13, including a $500 million IPO for NRG Yield that priced above its expected range and popped 24% on its first day of trading (we suspect the word ‘yield’ in the company’s name did nothing to discourage investor interest).

Dealogic reports that $2.8 billion is scheduled for 7/24/13—led by a $1.4 billion overnight secondary for Realogy Holdings (Apollo is cashing out again) and a $600 million follow-on for WhiteWave Foods—and $1.3 billion is scheduled for 7/25/13—led by a $300 million IPO for Diamond Resorts International.

Add some more overnight deals, and volume could easily reach $7 billion, which would be the highest in five weeks.

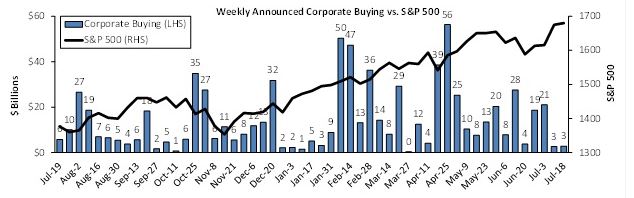

Companies Announce Modest $2.8 Billion in Float Shrink This Week. Buybacks Lackluster So Far in Earnings Season but Likely to Pick Up. Buybacks in Pre-Earnings Season Average Robust $2.4 Billion Daily.

On the other side of the ledger, corporate buying has remained light for the second consecutive week. Bally Technologies is buying SHFL Entertainment for $1.3 billion in cash, AT&T is buying Leap Wireless for $700 million in cash, and MB Financial is buying Taylor Capital Group using $50 million in cash. In addition, five companies have announced buybacks totaling $570 million, led by a $500 million repurchase for Mattel.

Buyback announcements have averaged only $100 million daily so far in earnings season, but we expect them to pick up by the end of the month as more companies report earnings.

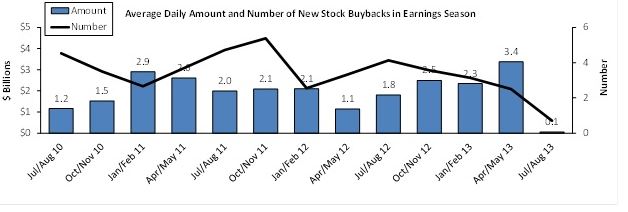

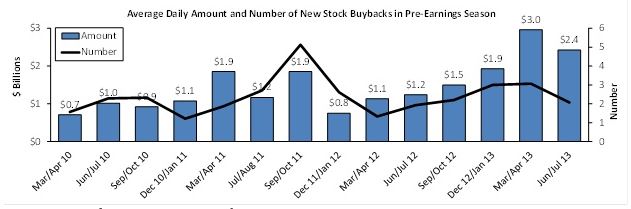

Buybacks in the pre-earnings season that just ended were robust, averaging 2.1 for $2.4 billion daily. Repurchases for Oracle ($12.0 billion), Pfizer ($10.0 billion), and Abbott Laboratories ($3.0 billion) boosted the volume. We are overweight Health Care in our sector model portfolio because far more sizeable float shrink has been announced in the sector recently than in any other.

This communication is a publication of TrimTabs Asset Management. It should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. Information presented does not involve the rendering of personalized investment advice. Content should not be construed as an offer to buy or sell, or a solicitation of any offer to buy or sell the securities mentioned herein. Performance results for investment indexes and/or categories, generally do not reflect the deduction of transaction and/or custodial charges or the deduction of an investment-management fee, the incurrence of which would have the effect of decreasing performance returns. All information is based on sources deemed reliable, but no warranty or guarantee is made as to its accuracy or completeness. Past performance may not be indicative of future results. Therefore, no investor should assume that the future performance of any specific investment or investment strategy will be profitable or equal to past performance levels. All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals, and economic conditions, may materially alter the performance of an investor’s portfolio. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment or strategy will be suitable or profitable for an investor’s portfolio.

© AdvisorShares