The initial goals of the Federal Reserve’s “GreatMonetary Experiment”— to keep rates low, createnegative real yields, spur consumption andcushion the budgetary consequences of fiscalstimulus — have largely been accomplished. Investors could now face the threat of rising bondyields. Various bull and bear scenarios mightensue. What are they and what could triggerthem? What are the risks to portfolios?

Key Points

The Federal Reserve’s initial goals from “The Great Monetary Experiment” are accomplished.Investors could now face the threat of rising bond yields.

- As the Fed begins to reduce monetary accommodation, first through the tapering of its assetpurchases and then eventually via a rise in interest rates, the Treasury yield curve will likelyrespond to this changing environment. What are the scenarios we might see surrounding theyield curve and interest rates, if 1) monetary velocity accelerates, but the Fed maintainscurrent policy?; 2) monetary velocity accelerates within expectations?; or, 3) monetaryvelocity accelerates beyond expectations?

- The fear of an imprecise course correction is palpable among many investors and economicpundits. There is a growing fear that the Fed will commit to zero far longer than economicallynecessary. The consequence could be a “Duration Blowback” as retail, institutional andforeign investors abandon Treasuries.

- The math behind the impact of duration risk can be ugly. As investors contemplate thepossible damage to their high quality portfolios from a rising yield curve, there is one specific precedent many are focusing on: the many similarities between the present andwhat some call “The Great Bond Bear Market of 1994.”

In this second installment of our three-part series The Danger of Duration in Investor Portfolios, we intend to map out how the Fed’s exit strategy might impact the yield curve. In doing so, we will provide a simple, mathematical framework about how this transition to a rising yield environment could affect investments.

We believe that the market is now grappling with what could become a potentially difficult transition to a rising Treasury yield environment. For the past five years, since the beginning of the Great Financial Crisis, virtually all bonds have enjoyed strong, positive returns; yields and spreads have collapsed. The main force behind this (and therefore the driver of these returns) has been the Federal Reserve (Fed) and its extraordinary zero interest rate monetary policy (ZIRP). But now, recognizing that their work is nearing completion, the Fed is contemplating its exit strategy.

Duration Described: The Ugly Math of Long Maturity

Duration is a measure of a fixed income instrument’s sensitivity to rising rates. In general, the longer the instrument’s maturity, the longer its duration, and the more sensitive its price will be to changes in market yields. This is because the instrument’s value is the sum of cash flows received (interest payments and principal payments), discounted at the current rate demanded by investors for that instrument until its maturity.

Time Value of Money

When rates rise, an investor has to implicitly discount all interest and principal payments for bonds at a higher rate. And that rate is compounded by the “time value of money”. Thus, if a bond’s interest and principal payments stretch far off into the future, the discount factor becomes large. The market reacts typically by dropping the value of the longer-dated bond much more dramatically than the shorter-dated bond.

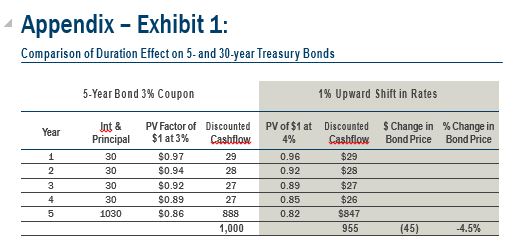

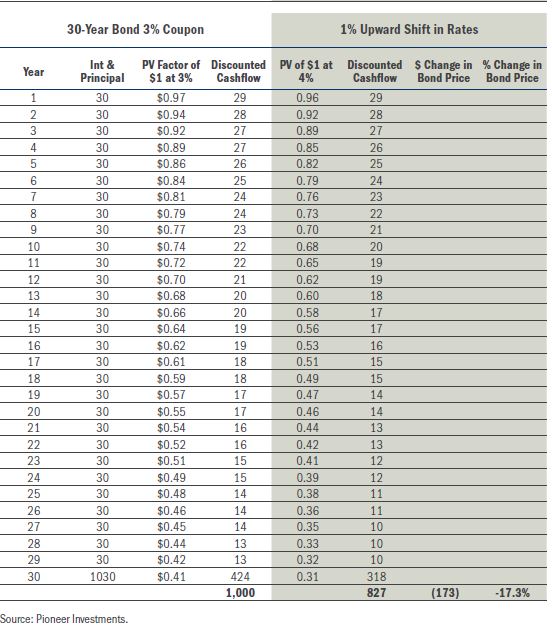

Below, for simplicity’s sake, we look at two bonds, each with identical coupons, each paying interest only once per year. The first is a 5-year bond with a 3% coupon; the second is a 30-year bond with a 3% coupon. We use the current Treasury curve as a baseline to calculate the existing bond prices and then calculate the change in value from a 1% upward and equal shift in rates.

Present Value

Consider two bonds with different maturities: a 2-year and a 30-year Treasury. For a $1,000 2-year Treasury bond yielding 1%, the principal to be paid back in 2 years is a large component of the bond’s present value. The interest payments (4 payments of $5 = $20 vs. $1000 principal) are a small part of the present value. Conversely, for the $1,000 year bond yielding 3%, the principal payment, made far in the future, is a smaller component of the present value. The interest payments (60 payments of $15 = $900 vs. $1,000 principal) are a much larger portion of the bond’s present value.

To adjust to the shift, the 5-year bond will drop 4.6% in value. The 30-year bond will drop 17% in value. (In our Appendix, exhibit 1, we show the year-by-year calculation.)

We use the current Treasury curve as a baseline to calculate the existing bond prices and then calculate the change in value from a 1% upward and equal shift in rates.

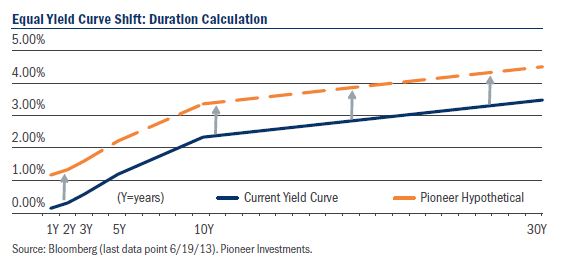

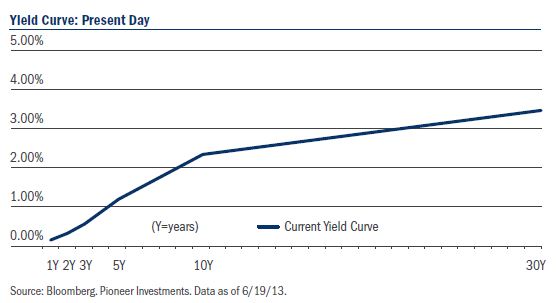

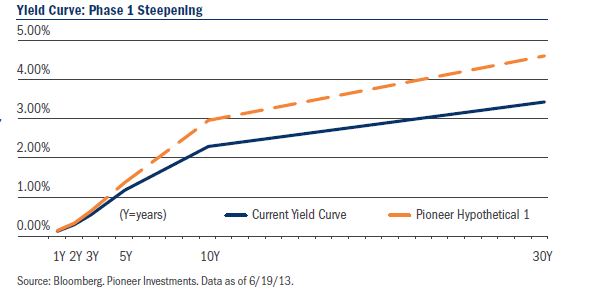

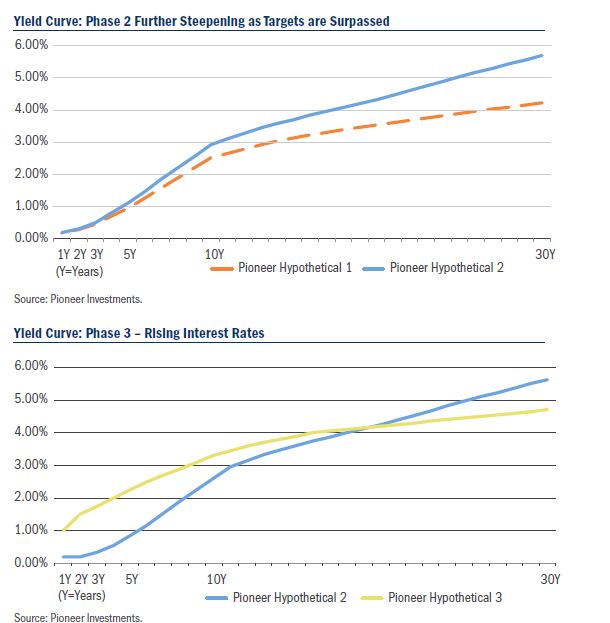

Treasury Yield Curve and Interest Rate Scenarios

As the Fed begins to reduce monetary accommodation, first through the tapering of its asset purchases and then eventually via a rise in interest rates, the Treasury yield curve should respond to this changing environment.

The next four graphs illustrate a hypothetical sequence of yield curve steepening and interest rate raises. The levels of rates and yields are not our forecast – although we believe they are quite plausible. Of course, there is no assurance that these will happen.

Current Yield Curve – the Fed maintains ZIRP.

1. Yield curve steepens as monetary velocity picks up. Targets are within the Fed’s scope, the Fed lets Quantitative Easing (QE) tail off, credit expansion offset by liquidity withdrawal. Investors are not getting overly anxious about Inflation.

2. Monetary velocity accelerates further. Inflation starting to become a fear as targets are met and surpassed, but the Fed maintains ZIRP.

3. ZIRP Abandoned. The Fed begins to raise interest rates to manage the velocity through net interest margin contraction – the profit a bank derives by borrowing on the short-end of the curve and lending against the long-end. The front end steepens, the back end begins to flatten in response to higher interest rates.

Treasury Tail Risk – The Ultimate Duration Blowback

There is one “extreme” scenario that some have suggested is the ultimate duration nightmare – a wholesale rout of the Treasury and Dollar markets. This event could transpire if investors lose faith in U.S. political and monetary authorities resulting from an extreme currency debasement and the simultaneous inability to reign in federal deficits. Those who argue we are going down this path may point to the seemingly never-ending rounds of QE and political paralysis on a long-term budget plan. While we sympathize with many of these concerns, we don’t find them compelling in the near- to intermediate- term for the following reasons:

- The U.S. is not the only country in the world engaging in monetary stimulus. Thus, other large, liquid currency options don’t appear to be particularly compelling “safe havens.” Indeed, the U.S. economy is the best performing large economy in the developed world and thus will likely instead be a capital magnet.

- Government spending as a percent of GDP has produced large budget deficits, but spending on an absolute basis has been essentially unchanged since 2010. Thus, we think deficits have been a product of the decline in GDP and tax receipts, not spending. That being said, politicians appear to be generally in agreement that the deficit needs to be reduced – it is the “How” that is currently being debated.

- Monetary policy has often been described as a “blunt instrument” with long lags between policy action and economic response. The fear of an imprecise course correction is palpable among investors and economic pundits. There is a growing fear that the Fed will commit to zero far longer than economically necessary.

- The consequence could be a “Duration Blowback” as retail, institutional and foreign investors abandon Treasuries. This would, of course, have significant consequences to the rest of the U.S. debt market.

1994 Redux? We’ve seen this Movie.

As investors contemplate the possible damage to their high quality portfolios from a rising yield curve, there is one specific precedent many are focusing on: the many similarities between the present and what some call “The Great Bond Bear Market of 1994.” Leading up to the events of that year, a steep recession and financial crisis in the late 80s and early 90s was followed by an extended “on hold” phase by the Fed. Investors were caught completely off-guard when the monetary regime shifted and the Fed began tightening in early February 1994.

At the end of 1993, the market projected that the 10-year and the 30-year yield would be 6.2% and 6.5% respectively by the end of 1994 according to BCA Research. The actual yields at the end of 1994 turned out to be 130 basis points higher at 7.8% and 7.85%. From the trough of yields in September 1993 to the peak in November 1994, the Treasury index lost 5%. High-grade spread products such as Agency mortgages, mortgage-backed securities, and investment-grade corporates also suffered losses. Some of the same technical factors are in place today.

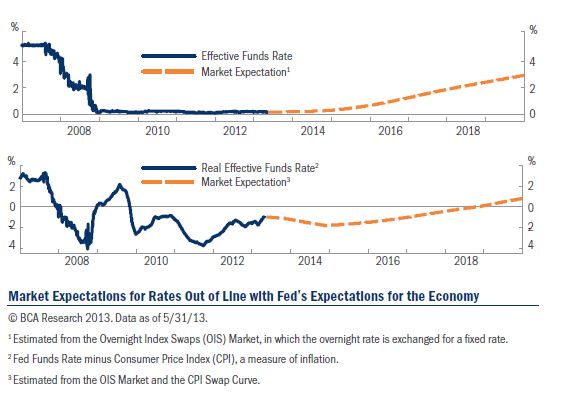

Many investors are not expecting any meaningful rise in rates before the end of the decade. Our friends at BCA have done some work in this area. The graph below suggests that investors are anticipating only modest interest rate increases for the remainder of the decade. And based on forward inflation expectations, rates will remain negative until 2020. This is clearly inconsistent with the Fed’s projection that the economy will reach full employment by 2015. It suggests to us that while investors are paying lip service to concerns about duration, it isn’t really reflected in the market.

A Few Other Possible Scenarios to Ponder

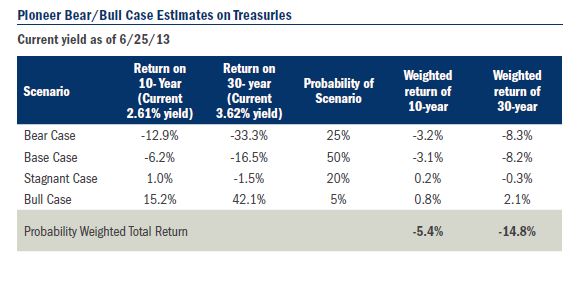

Over the past month, financial markets have erupted as investors grappled with the ramifications of a dramatic shift in monetary policy. Ironically, despite the fact that monetary stimulus remains on full-throttle and interest rate rises are still a long way off, fixed income investors have scrambled to adjust portfolios to this new paradigm. While high quality bond portfolios have sustained significant losses (at least relative to their paltry returns over the last few years), there is potentially much more to come. At this point we think it makes sense for investors to consider how their returns might vary under different economic and yield curve scenarios going forward. While the permutations are numerous, we propose four different potential scenarios unfolding over the next couple of years (through year-end 2014). Of course, we don’t have a crystal ball, but we have assigned probabilities based on our expectations of these scenarios:

- Bear Case: an accelerating rise in employment and inflation (+3% GDP growth), resulting in a 6.5% 30-year yield and a 5% 10-year yield at the end of the time horizon (probability: 25%)

- Base Case: a continued modest acceleration in economic activity (2%-3% for the next 2 years), that results in a 5% 30-year yield and a 4% 10-year yield (probability 50%).

- Stagnant Case: sluggish economic activity (1%-2%) over the next 2 years that results in a 30-year yield that is 4% and a 10-year yield that is 3% (probability 20%).

- Bull Case: another recession drives the 30-year yield to 2% and the 10-year yield to 1.25% by year-end (probability 5%)

We then looked at the returns of the 30- and 10-year bonds within the various scenarios, assuming an evenly-weighted gain or loss over the period. Based on our assumption, both 10-year and 30-year bonds would have negative returns.

While high quality bondportfolios have sustained significant losses (at leastrelative to their paltryreturns over the last few years), there is potentially much more to come.

Get Ready

The stage is being set for a potentially significant change in the fixed income markets. Investors need to understand how the evolving landscape could affect their allocation to this perceived “safe haven” asset class. In the next and final installment of the The Danger of Duration in Investor Portfolios we will investigate a number of fixed income subsectors that are being viewed as “refuges” from what may be a turbulent transition to higher rates.

The views expressed in this memorandum regard-ing market and economic trends are those of theauthor and not necessarily Pioneer Investments,and are subject to change at any time. These viewsshould not be relied upon as investment advice, assecurities recommendations, or as an indication of trading intent on behalf of any Pioneer invest-ment product. There is no guarantee that marketforecasts discussed will be realized or that these trends will continue.

© Pioneer Investments