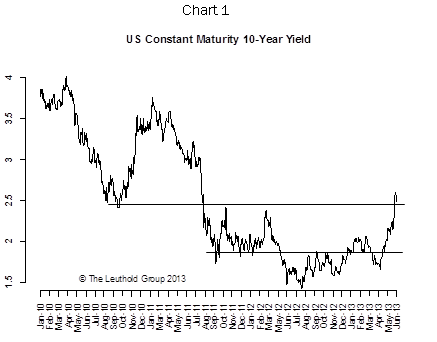

June was a volatile month for interest rates and currencies. The FOMC surprised the market as the Fed upgraded its economic outlook as well as mentioned a timeline for potential “tapering.” As a result, the upper bound of 245 on the 10-year was broken (Chart 1), and the subsequent stronger-than-expected jobs reports and confidence numbers further propelled the 10-year yield to 270 bps at the beginning of July. We were correct in expecting higher volatility, but did not expect the 245-250 barrier to be given up so easily.

So now the question is how high can it go? Just like every other market, bond yields tend to overshoot, and we think 3% is the upper bound in the short-term. However, we believe it will settle back closer to 250 bps by the end of the year.

There are several reasons we think the upside is limited for interest rates. First, the Fed has a great track record of overestimating economic growth. Its forecasts have consistently overshot in the last three years, and it’s had to launch QE2, OT, and QE3 to prevent a double dip. Our “muddle through” view on the global economy argues for at least keeping pace with QE, not tapering.

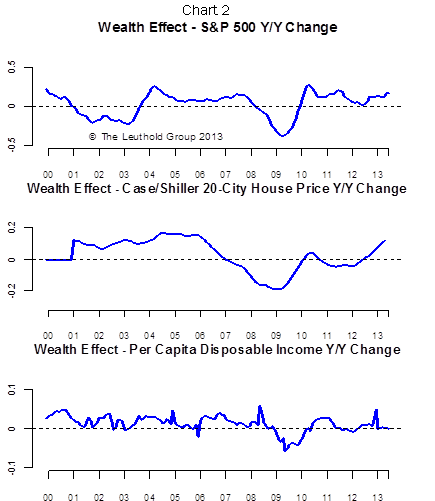

Second, the wealth effect would be at risk if interest rates go up too quickly. The Fed’s current policy supports the economy primarily through the wealth effect channel, not the traditional credit creation. Chart 2 shows the asset markets (proxied by the S&P 500) and the housing market are creating the wealth effect the Fed desired while the income effect is negligible.

The problem is that both the stock market rally and the housing market recovery are highly dependent on ultra-accommodative policies and low interest rates. In other words, the wealth effect is not permanent and can be reversed if the Fed exits too early and interest rates go up too far too fast.

As we’ve mentioned before, it’s all about confidence in recent years. If both the stock market and the housing market are adversely impacted by sharply higher interest rates, consumer and investor confidence will crater, which will negatively impact the economy as consumers and businesses pull back on spending and hiring. This is a real threat, and we believe the Fed would be genuinely concerned if rates go up too much.

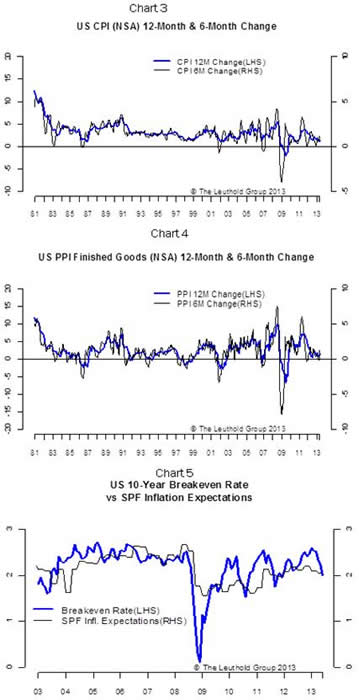

Third, the dip in inflation should be a concern to the Fed. After all, the Fed is much more worried about deflation than moderately higher inflation. Recent inflation numbers have uniformly tilted lower. Charts 3, 4, and 5 show lower than expected CPI and PPI numbers, and inflation expectation measures are trending down too. This is not just happening in the U.S., but in other developed and emerging countries. This should at least give the Fed pause when it comes to tapering decisions.

We are not even considering external risk events, which are many and can drive rates much lower. All taken together, we believe 250 is a reasonable level for the second half of 2013.

© Leuthold Weeden Capital Management