Introduction

Given recent strong performance and yields hovering at historic lows, a current topic of debate has been whether the high yield bond market has become an asset bubble and how much of a risk is the potential end to the Federal Reserve’s accommodative monetary policy to high yield investors. While we at Rainier acknowledge there are current risks in the fixed income market, we believe these concerns are not unique to high yield bonds. In fact, yields across the entire fixed income spectrum have reached record lows in an effort by the Federal Reserve to suppress interest rates. The effects can be clearly seen in the Treasury yield curve as bonds with maturities less than ten years are currently offering investors a negative real yield. While high yield bonds would be hard pressed to deliver the equity-like returns experienced over recent years, a number of factors support our case that high-quality high yield bonds should remain a part of a well-diversified portfolio as we believe they offer investors a compelling balance between risk and reward.

Prices: Need or Greed?

In addressing if the high yield market has in fact become too rich of an asset class, financial bubbles throughout history have often been characterized by excessive prices fueled by speculative expectations. We do not believe this type of exuberance has manifested itself in today’s high yield market as credit spreads are relatively close to their historical averages. Although high yield in general appears to be fully priced, we also believe the asset class still offers more attractive compensation to income-oriented investors relative to other fixed income vehicles. Therefore, rather than point to investor greed as the driving factor behind recent performance, we attribute the strong level of demand for high yield debt to a pair of ubiquitous forces.

First, we believe the Federal Reserve’s monthly purchases of $85 billion worth of long-term Treasuries and mortgage backed securities (accounting for almost 90% of all new issuance) has forced institutions such as pension funds and insurance companies to increasingly allocate their portfolios toward higher yielding spread products in order to meet their growing liabilities. Considering Treasuries and investment grade sovereign yields are near record lows, institutions seeking additional income have few viable alternatives to high yield. Insurance companies in particular have been under pressure to increase the level of income from their investments. As low yields pinch profitability, insurers have chosen to purchase higher yielding debt rather than increase prices or redesign their products to offer individuals less attractive features.

The second major force behind current high yield demand relates to investor demographics. Between 1945 and 1964, 76 million American children were born into the baby boomer generation. Now controlling over 80% of the country’s personal financial assets and accounting for more than 50% of consumer spending, this massive generational group has driven nearly all major cycles over the past 40 years. However, following the financial crisis, baby boomers saw a sharp decline in their household net worth causing nearly half to either delay or abandon retirement. After living through their second major stock market collapse in just a decade, many boomers are now unable to stomach the risk of having their nest egg devastated again as they near their retirement years. As such, soon-to- be retirees are increasingly shifting their assets toward income producing investments such as high yield corporate bonds, opting for the generally more conservative and reliable returns of fixed income over the potentially higher, but more volatile, returns of equities.

While Unlikely, Would Tapering be so Bad?

At the margin, the U.S. economy has been improving. The combination of rising job creation, increased bank lending and affordable housing has spurred an acceleration of new household formation. The supply of existing homes has fallen in line with its pre-crisis levels of just 4.7 months while the pace of new home construction remains lower than the historical cycle lows. New starts are just under 1,000,000 homes compared to the long-term average of 1,500,000. We believe demand will continue to outstrip supply for the foreseeable future, contributing to higher prices and improvement in household net worth, which should be supportive of consumer spending. Even the Bloomberg Consumer Comfort Index, which tracks Americans' perceptions of the economy and personal finances, is at a 5-year high.

With the U.S. economy on a positive trajectory, anticipation of the Federal Reserve scaling back its bond buying in the near term has given pause to many fixed income investors. However, despite encouraging economic data, we at Rainier believe it is still unclear if the economic recovery has been robust enough to be sustained in the absence of stimulus by the Fed. While payroll tax increases and the implementation of government spending reductions due to sequestration have begun, it is still very early in the process and we may have yet to see the full economic consequences from these actions. All the while, consumers and businesses are still awaiting Congress to pass a budget that does not strangle the economic recovery with spending cuts and tax increases. In light of these uncertainties, we believe the Fed tapering its quantitative easing program in the immediate future is both unwarranted and unlikely, especially with unemployment significantly above the Fed’s target of 6.57% and inflation continuing to trend lower.

However, as the economic recovery reaches critical mass, the eventual tapering of the Fed’s open market activities will likely not be entirely negative for holders of high yield debt. Interest rates moving higher would likely be received by investors as an affirmation from the Fed that the economic recovery has gained traction, and more importantly, is sustainable. While investment grade bond prices have historically been driven by macroeconomic factors that affect interest rates, high yield bonds have been more accurately characterized by their idiosyncratic risk—as their prices have been linked closely to a specific issuer’s ability to pay its debt obligations. Since high yield bonds are more closely correlated with private sector growth, the combination of higher risk premiums and improving corporate conditions in a typical economic recovery has resulted in spread compression as Treasury rates rise, helping mitigate the negative price impact of higher Treasury rates. Therefore, in the event the Fed was to begin tapering its bond purchasing, we would expect high yield bonds to outperform other types of fixed income.

Global Concerns Remain, Stay Sharpe

While acknowledging the unyielding demand for income in this low interest rate environment and the improvement in the underlying economy as bank lending expands, housing prices improve and job creation picks up, investors need to remain cognizant of the risks they are taking relative to the compensation they receive. We are positive on the outlook for high yield in this context, particularly given the myriad of question marks surrounding the global economy.

Conditions outside of the United States continue to introduce uncertainty into the financial markets. As we saw recently with Cyprus, the European sovereign debt crisis is not over and it is unclear if peripheral countries like Spain and Italy are taking full advantage of the time the European Central Bank has bought them with its outright market transaction promise to implement structural reform. Spain will likely miss its deficit targets and Italy is still wrestling with political uncertainty following a crucial election. Greece was recently reclassified as an emerging market by Russell Investments, the first time a developed nation has been downgraded by the index provider. In northern Europe, it is becoming increasingly apparent the citizens of countries such as Germany and Norway are no longer willing to finance the bailouts of weaker periphery countries and further restructurings will be much more onerous going forward. Perhaps most alarming is the deficit situation in France which is rapidly deteriorating while unemployment skyrockets—a significant cause for concern since Germany and France have been viewed until now as the most stable core countries within the European Union.

Away from Europe, China is struggling to cope with controlling an overheating property market and an unregulated shadow banking system. Economic data continues to reveal softening in the world’s second largest economy as the country makes the painful transition from an economy based on exports and manufacturing, to one driven by consumer consumption. As a result, emerging markets, as well as countries whose economies are heavily reliant on commodity exports (e.g. Brazil, Canada, and Australia), have seen massive outflows from both their debt and equities as fears over weakening demand and slowing growth escalate.

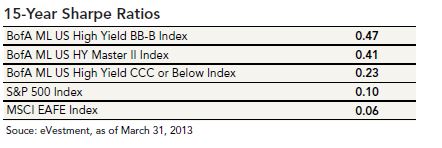

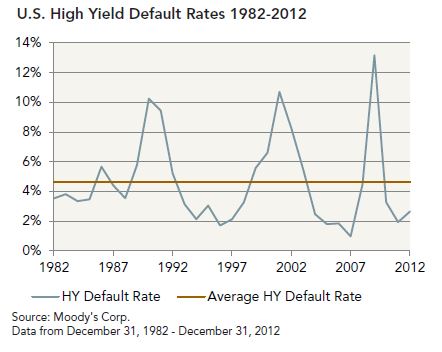

With such a cloudy macroeconomic picture, we anticipate high-quality high yield fixed income to potentially deliver superior risk-adjusted returns over the current market cycle relative to other asset classes. From a historical perspective alone, high yield bonds have achieved a remarkable risk- adjusted performance record, as measured by the Sharpe ratio, producing comparable returns to equities with significantly less volatility. This risk-reward relationship for high yield has been most pronounced among bonds rated BB and B. Today, high yield arguably looks even more attractive on a risk-adjusted basis as defaults are near historic lows, liquidity has vastly improved and corporate balance sheets are healthier than in years prior. Subsequently, volatility for high yield bonds has been on the decline, and compared to a year ago, volatility for the asset class has fallen by half.

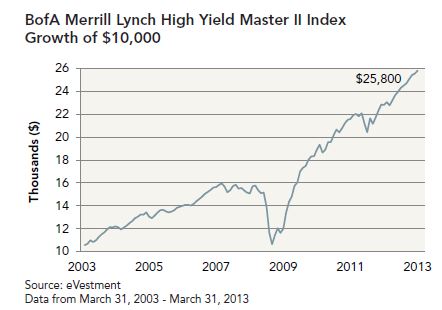

Despite these merits, investors in recent years have steadily piled into dividend paying stocks in hopes of capturing additional income and capital appreciation potential. However, over the past decade, high yield bonds1 have provided investors an average yield to maturity of 9.22% while the annual dividend yield for the S&P 500 has averaged 2.01%. Not only has high yield typically provided greater income relative to dividends, but high yield bonds should also appreciate in value if economic conditions in the U.S. and corporate balance sheets were to continue to improve, while exhibiting less potential downside volatility compared to equities if global weakness was to intensify.

Take the High Road to High Yield: Quality is Paramount

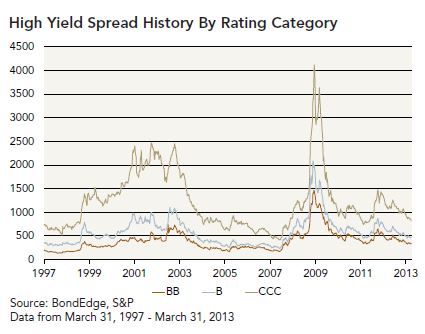

After considering current valuations, compensation levels, and the risks associated, we would encourage potential high yield investors to focus on the higher quality segment of the high yield market since we believe it to be the most attractive opportunity among fixed income investments. While we previously mentioned the broader high yield market as a whole seems to be trading near fair value, spreads received on riskier CCC rated debt compared to bonds rated BB and B are nearing historical tights as income-oriented investors have flocked to the highest absolute yield. Since this relationship may persist for quite some time, we consider the lower quality segments of the high yield market to be relatively unattractive since investors are not being compensated for the additional risk assumed in today’s volatile market characterized by periods of risk-on and risk-off.

Conclusion

As speculation surrounding the Fed’s next move reaches a fever pitch, investors have increasingly begun to view high yield with a nervous eye. In recent weeks, bondholders have reduced their high yield allocations at a record clip. However, we would firmly argue as demand for yield and market uncertainty persist, a selective portfolio of higher quality high yield bonds should allow investors to enjoy higher current income, modest capital appreciation opportunities and a more attractive risk-reward profile when combined with other asset classes. For those reasons, we believe investors who continue to allocate a portion of their portfolio to high yield debt should be well served in today’s market environment.

1As measured by the BofA Merrill Lynch High Yield Master II Index. Data as of March 31, 2013.

Mutual fund investing involves risk. Principal loss is possible. Investments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities. Investment by the Fund in lower-rated and non-rated securities presents a greater risk of loss to principal and interest than higher-rated securities. The Fund may invest in foreign securities which involve greater volatility and political, economic and currency risks and differences in accounting methods. These risks are greater in emerging markets. The Fund invests in small and medium sized companies, which involve additional risks such as limited liquidity and greater volatility. Diversification does not assure profit nor protect against loss in a declining market.

The Fund’s investment objectives, risk, charges and expenses must be considered carefully before investing. The statutory and summary prospectus contain this and other important information about the investment company, and may be obtained by calling 800-280- 6111 or by visiting www.rainierfunds.com. Please read it carefully before investing.

Bonds rated BB and B by Standard & Poor’s are of medium grade quality. Security currently appears sufficient, but may be unreliable over the long term. Bonds rated BB & B by Standard & Poor’s and Finch have a greater vulnerability to default but currently have the capacity to meet interest payments and principal repayments. The Sharpe ratio is a measure of the excess return (or risk premium) per unit of deviation in an investment asset or trading strategy. The BofA Merrill Lynch US High Yield Master II Index consists of U.S. dollar-denominated bonds with at least one year remaining until maturity and have credit ratings below investment grade but are not in default. The BofA Merrill Lynch US High Yield BB-B Index consists of bonds rated BB+ through B- by Standard & Poor’s or equivalent as rated by Moody’s or Fitch. The BofA Merrill Lynch US High Yield CCC or Below Index is a subset of the BofA Merrill Lynch US High Yield Master II Index and includes all securities with a given investment grade rating CCC or below. The S&P500 is an index of 500 stocks chosen for market size, liquidity and industry grouping, among other factors. It is designed to be a leading indicator of U.S. equities and is meant to reflect the risk/return characteristics of the large cap universe. The MSCI EAFE Index (Europe, Australasia, Far East) is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the US & Canada. You cannot invest directly in an index.

The chart located on page two highlighting the Growth of $10,000 illustrates the performance of a hypothetical $10,000 investment made in the BofA Merrill Lynch High Yield Master II Index Fund ten years ago. It assumes reinvestment of dividends and capital gains, but does not reflect the effect of any applicable sales charge or redemption fees. This chart does not imply any future performance.

Index performance is not indicative of the Funds performance. Past performance does not guarantee future results. Current performance can be obtained by calling 800-280-6111.

The Rainier Funds are distributed by Quasar Distributors, LLC.

Institutional Shares: RAIHX

Original Shares: RIMYX

© Rainier Funds