Equities Grind Higher as the Economy Continues to Muddle Through

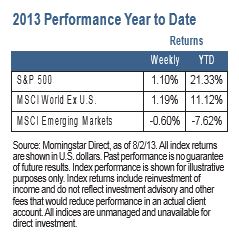

U.S. equities advanced last week, with the S&P 500 increasing 1.10%.1 For the month of July, the S&P gained 5.09%, and equities have increased 21.33% year to date.1 Second quarter earnings season is nearly complete, and there has not been a material change in estimated earnings for the balance of the year or 2014. Revenues were slightly ahead of expectations, and earnings per share were approximately 3% higher than expected, annualizing at about $110 per S&P 500 share.2

Waiting to Hit the Growth Accelerator

Earnings performance was skewed to financials that accounted for all of the earn- ings gains. The other 9 sectors combined had slightly negative earnings, according to FactSet analysis. Among the positive earnings surprises were cyclical sectors like technology, industrials and financials. Defensive sectors and those that generally benefit from inflation are not faring as well.2

We expect the U.S. economy to accelerate in the second half toward 2.5% to 3.0% GDP growth. We believe the labor market should continue to improve gradually as the number of employed workers increases at a rate similar to the first part of the year, despite the higher growth we anticipate. Consequently, we expect productivity to increase. Underlying inflation seems to have leveled out at a rate below the target of 2% set by the Federal Reserve. It appears QE3 will begin to gradually wind down after the September Fed meeting.

Weekly Top Themes

1. Real GDP for the second quarter was relatively weak at 1.7% with nominal GDP of 2.4%.3 We continue to believe that pent up demand in cyclical sectors and a decline in the negative effect of sequestration will help growth trends.

2. July monthly payroll employment disappointed versus expectations

with an increase of 162,000 jobs.4 Previous data were revised lower, and the

unemployment rate declined only because the employment participation rate

dropped. Since QE3 started, the monthly average payroll growth has been

roughly 200,000.

3. The July ISM Manufacturing survey reported its biggest one month increase since 1996.5 Domestic final demand, particularly housing-related issues, were the biggest areas of strength.

4. The Case-Shiller home price index is now up nearly 15% from its low in March 2012.6 The overall figure follows from the recently reported 1.1% increase in May (10-city composite, seasonally-adjusted).

5. The race to succeed Fed Chairman Ben Bernanke is led by Janet Yellen and Larry Summers. It is unlikely either will suggest premature Fed tightening. Yellen could be the candidate of continuity and stability. Summers may be seen as the change candidate, with greater uncertainty regarding policy.

The Big Picture

We advocate a moderately pro-growth portfolio underpinned by a slowly improv- ing global economy and reflationary policy support from G7 central banks. Equities should be beneficiaries of growth and reflation tailwinds as earnings advance and investors gradually add risk exposure after a period of conservatively- based portfolio composition. In fixed income, yields should slowly trend higher in response to better growth conditions, resulting in poor total returns, with risks pre- dominantly to the bearish side. The ongoing reversal in the prior commodity boom points to further price weakness until global growth is strengthened materially.

In our view, investors should consider an overweight stance on equities. Equities are poised to benefit from improving earnings, while rising yields imply a modest

downturn for bond portfolios. On a sector basis, we favor cyclical sectors that should rebound as growth improves.

MAJOR WORLD ECONOMIES — POTENTIAL OUTCOMES

U.S.: The economy will continue to gain traction with GDP likely to expand nearly 3% over the coming year.

China: We remain proponents of a soft landing, anticipating 7% to 7.5% real growth over the next year.

Europe: It seems that the worst may be past, but any upturn will be weak and fragile.

Japan: The economic recovery resulting from aggressive reflation should continue.

1 Source: Morningstar Direct, as of 8/2/13. 2 Source: FactSet Earnings Insight, 8/2/13, http://www.factset.com/earningsinsight. 3 Source: Bureau of Economic Analysis, “National Income and Product Accounts Gross Domestic Product, Second Quarter 2013 (advance estimate),” July 31, 2013, http://www.bea.gov/newsreleases/national/gdp/gdpnewsrelease.htm. 4 Source: Bureau of Labor Statistics, “The Employment Situation - July, 2013,” August 1, 2013, http://www.bls.gov/news.release/empsit.nr0.htm. 5 Source: July 2013 Manufacturing ISM Report On Business,® August 1, 2013, http:// www.ism.ws/ismreport/mfgrob.cfm. 6 Source: S&P Dow Jones Indices, “Home Prices Continue to Increase in May 2013 According to the S&P/Case-Shiller Home Price Indices,” July 30, 2013, http:// us.spindices.com/index-family/real-estate/sp-case-shiller.

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float- adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Non-investment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, includ- ing currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

Nuveen Investments | 333 West Wacker Drive | Chicago, IL 60606 | 800.752.8700 | nuveen.com

GPE-BDCOMM1-0813P

© Nuveen Asset Management