Stocks Climb on ECon Data

Equity markets moved higher last week on the back of better economic data. The S&P 500 Index gained 1.1% and the Dow Jones Industrial Average was higher by 0.6%.

It proved to be a busy week with data on manufacturing, employment, personal income, and Federal Reserve minutes offering different glimpses at the economy. Ultimately, investors were pleased to see a strong manufacturing report coupled with Fed minutes showing potential of a delay in the slowdown of asset purchases.

Within the manufacturing sector, the ISM PMI Index rose to 55.4 in July from 50.9 the month prior. Readings above 50 indicate expansion in the manufacturing sector. The strong July figure came after three months of readings within one point on either direction of 50, raising concerns of a slowdown in that area of the economy. July’s survey indicated sharp improvement in new orders, production, employment and inventory. New orders regularly portend future growth and jumped from 51.9 to 58.3.

Switching gears to overall economic growth, the second quarter Gross Domestic Product (GDP) report showed an economy growing at an annualized 1.7% rate. While this was better than economists anticipated, the underlying components were relatively weak. Residential investment led the way with a 13.4% increase, but personal consumption decelerated from the first quarter with a 1.8% gain.

Transitioning to the consumer, personal income rose 0.3% in June and personal consumption expenditures (PCE) increased 0.5%. Adjusted for inflation, real PCE matched its prior two months with a 0.1% increase.

Based on the latest annual revisions from the Bureau of Economic Analysis (BEA), the personal savings rate received a slight bump higher. Following the revisions, the savings rate is now 4.4%. The BEA moved defined benefit plans from cash accounting to accrual-based accounting to capture individuals’ future benefits.

Source: Haver Analytics

Outside of economic data, the Federal Reserve made slight waves with the statement from its July meeting. Throughout the release, references to higher mortgage rates, restrained economic growth, and softer than desired inflation led investors to believe the Fed would remain accommodative. In addition, Federal Reserve Bank of St. Louis President James Bullard said, “The committee needs to see more data on macroeconomic performance for the second half of 2013 before making a judgment on this matter.” He cautioned against reliance on forecasts versus actual data releases.

Low Quality Jobs Recovery Continues in July

In a busy week of economic data, investors ended the week on a mixed note. The government jobs report revealed a labor market experiencing steady if not unspectacular growth, as nonfarm payrolls came in below consensus estimates while the unemployment rate surprised to the upside.

Arguably, markets should have retreated on Friday, as the jobs report offered the worst of both worlds for investors. While payrolls have come to represent the health of the labor markets, the unemployment rate has become a perverse indicator of Fed monetary policy. The July report was thus negative on two fronts, with nonfarm payrolls disappointing and the jobless rate falling more than expected.

According to Dave Altig, research director at the Atlanta Fed, July’s report modestly accelerates the timetable for when the FOMC might wind down asset purchases and begin the process of raising short-term interest rates. Assuming a continuation of the current 12-month average monthly payroll gain of 190,000 jobs (and no change in the labor force participation rate), Altig calculates that that the unemployment rate will near 7.0% by the end of 2013, and the 6.5% level sometime in 2014. Those thresholds coincide with what Fed Chairman Ben Bernanke has associated with an end to QE and ZIRP, respectively.

Source: Federal Reserve Bank of Atlanta

Equity markets did indeed slip after the bell, but slowly crawled back into the black by 4pm. The Fed’s de-emphasis of stimulus reduction after Wednesday’s FOMC meeting apparently assuaged market fears, with markets gapping up to start Thursday and taking the labor data in stride a day later.

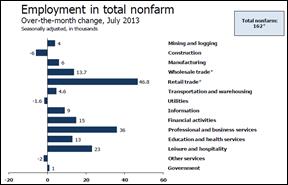

For the month, nonfarm payrolls rose 162,000, below the pace of 189,000 jobs per month added in the prior 12 months. Consensus had been looking for a 195,000 gain. Making matters worse, May and June were revised lower by 26,000 jobs, taking some of the luster off June’s originally reported 195,000 increase.

Government jobs were flat in July, an aberration from recent history in which the series has slowly hemorrhaged positions. A 10,000 increase in local government education jobs boosted the sector, as state, Federal and local ex-education each contracted.

Almost the entirety of the improvement in the nonfarm report occurred in service-providing jobs, as goods-producing jobs added just 4,000 jobs in July. Despite the supposed renaissance in American manufacturing and homebuilding, the construction and manufacturing sectors combined to add a net zero jobs to the US economy during the month.

Source: Global Economic Analysis

There is ongoing concern that the quality of the US labor market recovery is less than spectacular. We have previously noted here that a disproportionate amount of labor market gains have come via the retail trade and leisure & hospitality sectors – generally lower wage industries. According to the Wall Street Journal, nearly 70% of payroll gains in the second quarter were generated in these areas, despite only accounting for about one-third of the job market. Furthermore, “the average hourly pay for these jobs is $15.80, while that for the remaining two-thirds of jobs is $27.16 an hour.”

July was no different, as retail trade added 47,000 jobs and food services & drinking places (a sub-sector of the leisure & hospitality sector) added 38,000. Meanwhile, professional & business services added 36,000 jobs, with about a fourth coming from temporary help services.

The result of this low quality jobs recovery is stagnant wages on an inflation-adjusted basis. Real incomes have risen by 1% a year since the recession ended in 2009. In the past 12 months, real average hourly earnings for all employees were positive only six times. This lack of real wage growth continues to pressure consumer spending, which is leaning heavily on debt expansion and a falling savings rate.

In the household survey, the headline unemployment rate fell to 7.4%, two tenths lower than June and the lowest reading of the recovery. The labor force participation rate did slip by a tenth to 63.4%.

After a momentary spike in the underemployment rate, or U-6, the measure receded back from 14.3% to 14.0%. Some view this as a truer measure of unemployment as it includes discouraged workers as well as those involuntarily working part-time for economic reasons.

Ultimately, nonfarm payrolls came in a bit soft, but as we have seen in recent revisions, they could easily be brought back in line with recent averages. Investors should continue to watch real wage growth, however, and the quality of this labor market recovery. Without a significant pick up, US economic growth will be relegated to the ongoing artificial support of the US government. With the establishment and household surveys diverging, this secondary source of support could be eliminated more quickly than expected.

The Week Ahead

In contrast to last week, there is only a modest amount of new data on the calendar this week. Particular attention will be paid to the ISM Non-Manufacturing Index, job openings and labor turnover (JOLTS), consumer credit and wholesale trade.

On Monday, Dallas Fed President Richard Fisher will speak on the economy. Mr. Fisher will become a voting member of the FOMC in 2014 and has regularly criticized quantitative easing. Other members of the Fed will also speak during the week, including Charles Evans, Charles Plosser and Sandra Pianalto.

A handful of central banks meet this week, including those in Australia, Japan, Korea, Peru and Russia.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value

© Fortigent