Overview…

- We review recent periods of financial market stress, which bring about elevated levels of asset volatility and during which investors are vulnerable to incurring substantial loss of capital.

- We illustrate that risk is determined both by the volatility of individual investments in a portfolio and the degree to which they are correlated. Often overlooked, correlation is a critical factor.

- Because assets become more correlated at the same time they become more volatile, we argue that the benefits of diversification often are difficult to achieve when they are most needed.

- We show the unwelcome degree to which the performance of hedge fund strategies has been tied to that of the overall equity market.

- Finally, we stress the importance of finding uncorrelated investment opportunities in order to construct portfolios that will be durable during the next market volatility event.

The Importance of Correlation in Portfolio Construction

As we approach the five-year anniversary of the financial crisis, stock prices are at record levels, the VIX is depressed, and economic growth, while uninspiring, appears on stable footing. The sanguine risk climate we find ourselves in bears little resemblance to the state of disarray that consumed financial markets in late 2008. During that tumultuous period, investors sought to deleverage risk exposures and were forced to hedge at any cost. So forceful was the demand for equity market protection that in November 2008, the VIX surpassed 80. Other risk metrics – from currency volatility to credit spreads – also soared during this time period.

Periods of financial market stress always bring about a surge in asset price volatility. In 1997, the devaluation of the Thai baht pushed the VIX to nearly 40. In 1998, the LTCM implosion brought the VIX to 45 as the market realized the magnitude of the hedge fund’s short volatility portfolio. The summer of 2002 saw the VIX again reach 45 as credit spreads soared and the accounting practices of some leading US companies were called into question. In May of 2010, first the Flash Crash and then the Greek debt melt down forced the VIX above 40. More recently, the August 2011 US debt ceiling showdown pushed the VIX to nearly 50. Each volatility event has a unique underpinning and there is a specific asset class that typically forms the eye of the hurricane. In all cases, however, the risk of substantial loss of capital is very real for investors.

Why does the 100 year storm seem to occur every 5 years in financial markets? And more importantly, how can investors prepare for the next period of elevated volatility? In the discussion that follows, we highlight some of the important lessons that recent periods of crisis offer and illustrate how investors can incorporate these into sound risk management practices.

We argue that allocators of capital must do more than understand the individual risk profiles of their investments. The nature of modern day financial market shocks requires investors to analyze how these risk allocations interact with each other. That is, the correlation profile of investment allocations is a critical and often overlooked component of portfolio construction. At a time when the arc of Federal Reserve policy is shifting and as alternative investment strategies have behaved increasingly like the overall stock market, this is especially true.

A Brief and Informal Primer: The Math of Volatility and Correlation

The risk profile of the S&P 500 index (SPX) is determined by two factors. First, there are (usually) 500 stocks in the index, each with its own individual volatility level. For example, GE has experienced a volatility of 19% over the past month. In contrast, MSFT has a one month realized volatility of 48%. The individual volatilities for each stock in the SPX all contribute to the volatility of the index.

A second and very important factor that determines the volatility of the index is the extent to which the stocks are correlated with one another. When the stocks that comprise an index move together closely, they provide little opportunity for diversification. However, when there is low correlation among the stocks, the movements upward for some and downward for others, enable risk reduction for the index. In the case of MSFT and GE above, it turns out that on July 19th, 2013, MSFT fell by 11%, the same day that GE rose by 4.4%. While each stock individually exhibited a high degree of volatility, because the price movements were opposing, the SPX move on that day was more muted.

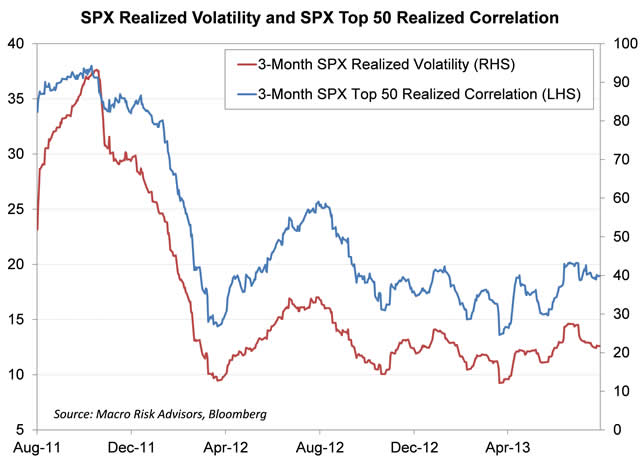

In the case of US equities right now, the individual stock volatilities are low and so too is the level of correlation among them. We show this in the chart below.

At present, the extremely low level of correlation of stocks is having a substantial dampening effect on the volatility of the SPX. Over the past month, the average level of correlation among stocks in the SPX is just 13%. For example, if instead the average level of correlation among the stocks in the SPX were 40% (more consistent with history), the volatility of the SPX would be 11.4%, fully 66% higher than its current level of just 7%. This is a very important point and illustrates the degree to which portfolio risk is tied not just to the volatility of its components, but also to how the individual securities interact.

Will Diversification Be There When You Need It?

The previous example highlights a frustrating reality for managers of portfolio risk. That is, the diversifying benefits of low correlation tend to accrue most in low volatility environments when such benefits are least needed. However, when a period of market stress emerges, asset prices become more volatile and at the same time, they become more highly correlated. The compounding effect can be quite challenging and for those who manage to a quantitative value at risk framework, the result of both higher volatility and higher correlation is clear: more risk.

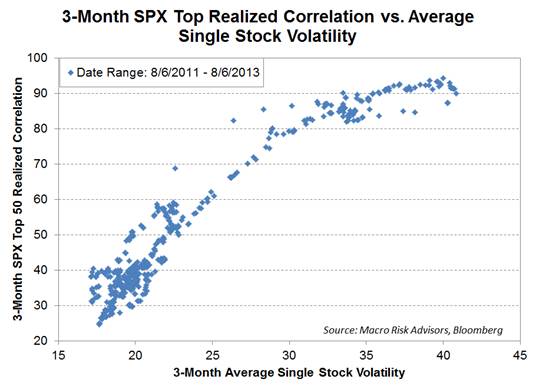

It is generally the case that macroeconomic uncertainty can make stocks both more volatile and more highly correlated at the same time. Common sources of macro risk include the Fed, energy prices, geopolitical risk, inflation shocks, unemployment, sovereign risk, elections and fiscal policy dysfunction. Conversely, low correlation and low stock volatility tend to coincide as the very economic environment that breeds low stock volatility, and also lacks any impactful macro risk factor. This was generally the case from 2004 to 2007 during the great mortgage credit boom. In the graph below we provide a scatter plot of 3-Month realized single stock volatility in the SPX and 3-Month realized correlation.

Using data over the past two years, we illustrate that periods during which stocks become more volatile are the same periods when they become more correlated to each other.

Why Correlation is So Important Now

While the US equity market has recently reached an all-time high, the past several months have illustrated vulnerabilities inherent in the market risk framework. With the Fed’s intention to taper asset purchases, market participants have been forced to contemplate what may be far reaching implications for risk management practices. What does the investment landscape look like in an era of less accommodative Fed policy? And how can investors build portfolios that remain durable in a changing risk regime?

The unwinding of the “risk on/risk off” framework carries significant implications for portfolio risk. At the center of this framework is a decidedly negative correlation between stock and US government bond prices. For example, in the period from May 2012 to May 2013, the daily returns of the 10 year note and the SPX exhibited a correlation of -55%. However, over the past three months, this correlation has changed dramatically, rising to near 0%. The strong inverse relationship between stocks and bonds had become deeply embedded in both the investment psyche and risk management fabric of today's markets. What now are the implications for portfolio risk and construction, if the negative correlation between stocks and bonds has broken down?

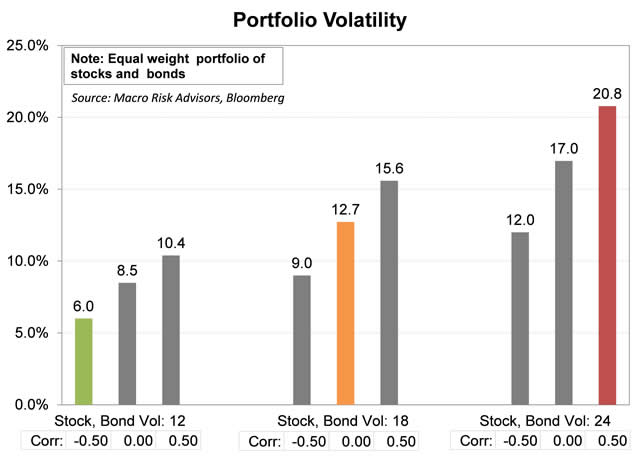

The point may be obvious, but it is worth showing mathematically. Portfolio variance is impacted dramatically when stock and bond prices become more highly correlated. Below we show six hypothetical portfolios, each composed of a 50% allocation to stocks and US Treasuries. We assume three different volatilities (12%, 18% and 24%) for both assets and three correlation levels between stocks and bonds (-50%, 0% and 50%).

Consider an equally weighted portfolio of stocks and bonds where each component has 12% volatility and where they have a -50% correlation with one another. As we illustrate in the graph above, this portfolio would have a volatility of 6%. If instead both assets have 18% volatility and the correlation is 0%, the portfolio volatility more than doubles to 12.7%. In the more extreme case where both assets have 24% volatility and the correlation is positive 50%, the portfolio volatility is 20.8%. Importantly, assuming both assets have 12% volatility, merely by shifting the correlation from -50% to zero while holding the volatilities constant, the portfolio volatility surges by 41% (from 6% to 8.5%).

The stylized example highlights the significance of changing correlations on overall portfolio risk. The size and duration of the Fed’s unconventional policies have contributed to a risk on/ risk off framework that investors have been forced to accept as semi-permanent. If the volatility and correlation assumptions that determine aggregate portfolio risk change, investors will need to reconsider how they allocate capital.

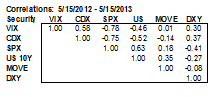

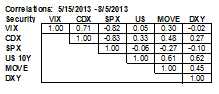

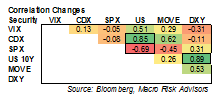

To illustrate further the wholesale changes in the market risk environment, we provide three matrices that show the changes in correlation of various risk measures. The first matrix uses data from May 2012 to May 2013. The second graph uses the recent period since May 2013. The changes, in many cases, are dramatic. For example, the correlation between daily % changes in the price of the 10 Year US Treasury note and corporate credit spreads has changed dramatically. For the first period, on days when credit spreads widened, the yield on the ten-year Treasury tended to fall, consistent with a risk off event, and leading to a correlation of -52%. More recently, as credit spreads widened, the yield on the 10-year tended to rise, leaving them 33% positively correlated. For fixed income credit investors, this shifting relationship has created more risk at the portfolio level.

Alternative Investments…

Uncorrelated, Sort Of

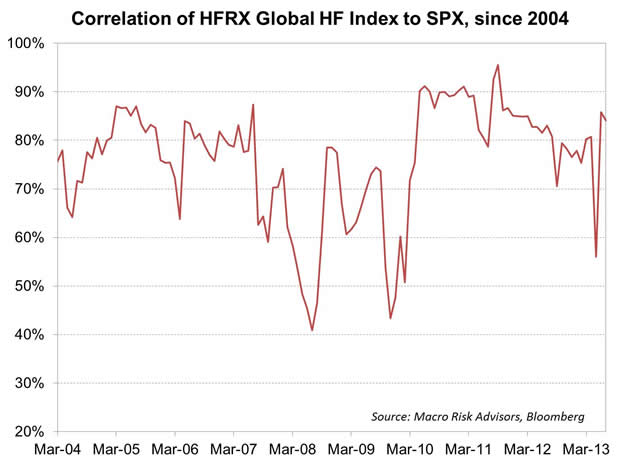

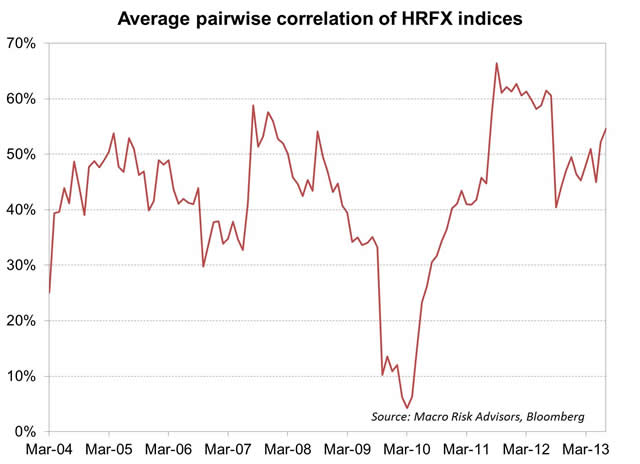

The volatility of equity markets that has been characteristic of much of the past 15 years has spawned a great deal of interest in alternative investments. Pitched as “all weather” strategies, hedge funds have sought to provide returns in both bullish and bearish market environments. This may have been the case when the industry was smaller and strategies like convertible bond arbitrage had fewer funds competing for the same opportunities. According to HFR, global hedge fund assets under management have reached $2.4 trillion, up from less than $500 billion fifteen years earlier. Now it is often argued, and the data show, that the performance of hedge funds is increasingly tied to that of the overall equity market.

The graphs below illustrate the point. In addition to hedge funds becoming increasingly correlated to the equity market, they are increasingly correlated to each other. As we have previously discussed, a higher degree of correlation among strategies can be expected in a higher volatility environment. In the chart below right, this can be seen especially during 2011 when the US was near the brink of default and the European sovereign crisis intensified

Source: Macro Risk Advisors, Bloomberg

RISK MEASURES USED:

- CBOE VIX index to measure equity implied volatility

- Markit CDX index to measure high grade credit spreads

- S&P 500 Index

- 10-Year Treasury Yields

- MOVE index to reflect interest rate implied volatility

- DXY index to capture movements in the US dollar

Source: Macro Risk Advisors, Bloomberg

What are the Implications for Portfolio Construction?

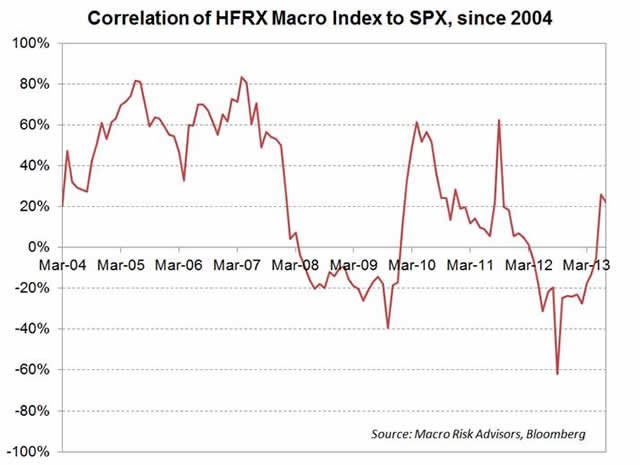

As we have shown, assets typically become more correlated during times of market stress, a reality that poses challenges for managers of portfolio risk. While once a solid source of diversification, many of the alternative investment strategies embraced by hedge funds have now become more correlated to the overall equity market. While this further complicates the challenge of earning return in a risk controlled manner, there remain strategies that provide diversification. Global macro investing, for example, has exhibited a noticeably lower correlation to the SPX, as we show below. Because it is focused on unique opportunities (the reflation trade in Japan, for example), the global macro strategy has proven a nicely diversified component of institutional portfolios.

Given the uncertainties inherent in the Fed’s evolving policy stance, a key risk management discipline going forward will be in finding uncorrelated investment opportunities. If achieved, the risk reduction impact of a diversified portfolio will prove important.

Concluding Thoughts

As investors construct portfolios, a key focus must be in understanding the risk factors that drive returns for the strategies being implemented. Are the strategies harvesting alpha from common sources of risk? How do the strategies perform in the rich set of shock scenarios experienced over the past fifteen years? By carefully selecting strategies that exhibit low correlation both to the market and to each other, investors can construct portfolios that will prove durable through the next period of market stress.

© Macro Risk Advisors