Tapering Uncertainty Means Volatile But Range-Bound 10-Year Rate

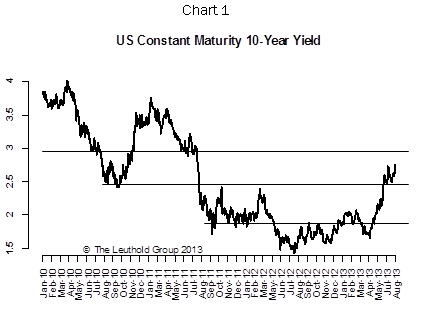

The U.S. 10-year yield was pretty much trapped within a 25 bps range between 250 and 275 in July (Chart 1), but intra-day volatility has picked up noticeably. In the last three months, there were 21 days of greater than 5 bps daily moves and 7 days of greater than 10 bps daily moves on the U.S. 10-year yield, the most in the last one and a half years.

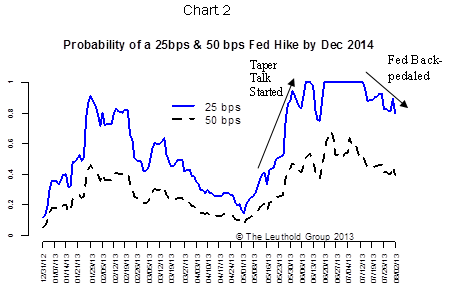

The Fed, of course, deserves all the credit for creating this volatility. The market seems to be sufficiently confused about what the Fed is trying to do. The probability of a 25 bps fed funds rate hike by Dec 2014 surged to 100% shortly after the June FOMC meeting. But since then the Fed has substantially tapered the taper talk, and the probability of a 25 bps hike has dropped below 80% (Chart 2). Although the bias is still towards a September taper, it is not a certainty.

In our last report, we stated that “ the Fed has a great track record of overestimating economic growth. ” We never thought we’d be proven right so quickly. In their July FOMC statement, the Fed already guided the outlook for economic growth lower from “moderate” to “modest.” This is more consistent with our “muddle through” view.

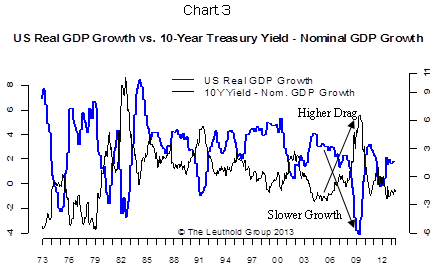

If interest rates keep going higher from here, we would run the risk of derailing a still-fragile recovery. Chart 3 shows a clear negative relationship between Real GDP growth and the interest rate drag (proxied by the difference between the 10-year yield and nominal GDP growth). In other words, a slow-growth economy simply can’t afford high interest rates. This is another reason we think the upside for interest rates is limited.

In our last report, we also mentioned, “ the dip in inflation should be a concern to the Fed ” and “ this should at least give the Fed pause when it comes to tapering decisions.” Apparently Bernanke read our report and promptly added a new sentence in the July FOMC statement that addressed the threats of “very low inflation” which “increases the risk of outright deflation.”

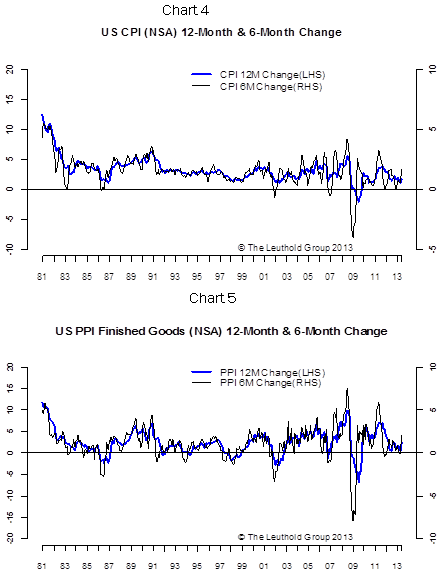

Both the CPI and PPI numbers showed a moderate uptick in June (Charts 4 and 5), but we haven’t seen strong evidence that inflation pressure is building up fast. This is true for both the U.S. and around the world.

Is the inflation picture bad enough to change the Fed’s view on tapering? We don’t think so. But the fact that Bernanke is stepping down after this year certainly is a factor. We believe he cares about his reputation enough to want to start tapering as long as the economic picture does not deteriorate significantly.

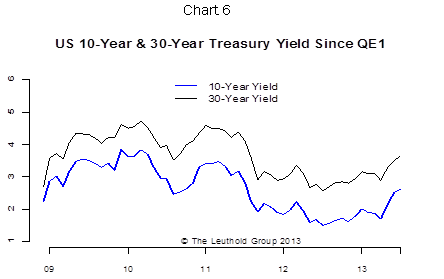

We believe the Fed knows that QE1-3 have not been as effective as they hoped. Chart 6 shows the 10-year and 30-year treasury yields since QE1. Even with massive bond purchases, long term yields are now higher than they were before QE1 started. Having seen what happened to Greenspan in the last few years, Bernanke would certainly feel safer with tapering than not. As long as the Fed tapering uncertainty exists, we expect higher volatility on the 10-year yield to persist.

© Leuthold Weeden Capital Management