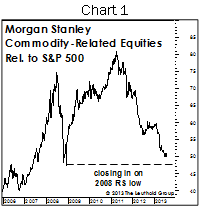

For more than two years we’ve discussed the supply-side risks to commodity producers stemming from capacity built during the manic “Third Act” of last decade’s Three Act Play in commodities. Commodity-oriented equities have indeed underperformed since 2011 (chart 1), but to date, most pundits have laid blame squarely on the demand side (i.e., the sharp deceleration in Chinese economic growth). We don’t have a strong opinion on the short-term direction of the Chinese economy, but the capacity overhang looks like a multi-year story to us, independent of China’s short-term direction.

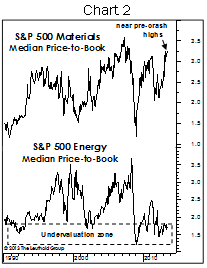

Given our longer-term outlook, we find it hard to believe that U.S. Materials stocks are trading at valuations seen at the secular commodity peak in 2008. Energy stocks, though, are trading at valuations that have usually represented good long-term entry points (Chart 2).

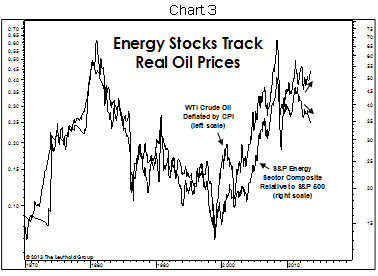

For decades, the relative price performance of Energy stocks has tracked the inflation-adjusted price of crude oil closely (Chart 3). But in the last 18 months, Energy stocks have badly lagged the predominantly healthy trading pattern in crude oil. This might be attributable to the belated plunge by some of the big oil producers into natural gas. Still, weakness in these equities could be a warning for the bigger commodity (oil) itself.

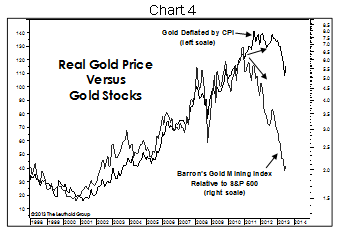

We don’t know whether trading patterns in gold and gold mining stocks provide an apt comparison. But, for what it’s worth, the gold mining stocks matched the secular bull market in gold bullion for ten years before the miners began to underperform (Chart 4). Many investors then pounced on the miners in hopes of a “catch up” phase vis a vis physical gold. But the alternate view—that physical gold would eventually join the sinking mining stocks—was the correct interpretation. Look for substantially lower oil if this pattern repeats.

© Leuthold Weeden Capital Management