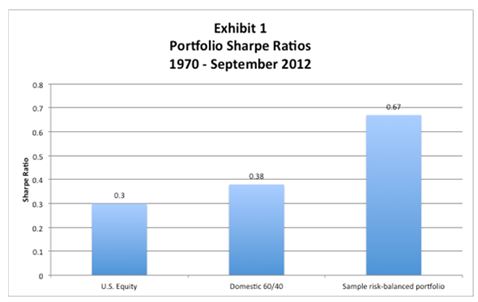

Last year in a white paper called “Engineering a better retirement portfolio”1, we demonstrated the long term benefits of investing with a balanced risk profile. Exhibit 1 shows the trailing Sharpe ratios reported in that paper for the S&P 500, a “traditional balanced” domestic 60/40 portfolio, and a “risk balanced” strategy invested to equalize the risk contribution from stocks, bonds and commodities.

The message from that chart is clear: Better balance leads to more efficient portfolio performance over time. Indeed, an emphasis on balance over the past decade or more has been essential to investment success given market volatility and low stock market returns.

That is, until this year.

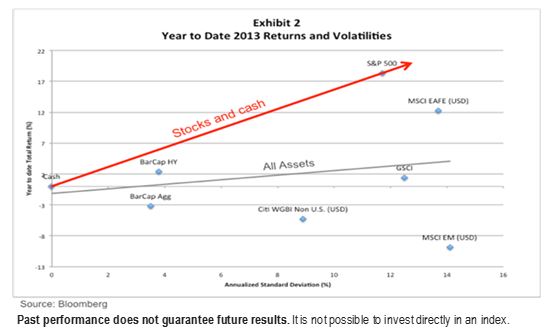

So far in 2013, investors have been hindered, not helped, by portfolio balance. Exhibit 2 on the following page plots year to date returns against annualized volatility for major asset classes in 2013. I have also plotted two lines across the scatter plot. The grey line shows a simple trend line through all of the points. This is a very rough way to visualize the trade-off between volatility and return across all of these asset classes. The slope of the grey line is upward sloping, but shallow, implying that well-balanced portfolios are likely to have delivered low returns this year, whether invested conservatively or aggressively along the risk spectrum.

The red line simply connects the two plot points representing cash and the S&P 500. This line shows the trade-off that has been available in portfolios invested only in a combination of cash and large U.S. company stocks. Here, the reward for risk has been much more generous, and the implication is that portfolios whose risks have been concentrated in U.S. stocks are likely to have delivered high returns this year. Taken together, these lines depict the two defining realities that investors have faced in financial markets in 2013. First, the payoff for taking equity risk has been very handsome. Second, the likely impact of broad diversification has been to subdue returns and create less reward per unit of volatility. The historical benefits of diversification are missing in 2013.

Investors now must surely be tempted to gravitate toward increasingly equity-focused risk allocations. Indeed, we ourselves continue to recommend a diminished risk exposure to plain vanilla bonds, and a commensurate overweight to equity risk, for investors who embrace a flexible allocation strategy. However, we think the impulse to abandon diversification and balance today should be resisted for two reasons. First, several catalysts for renewed stock market volatility lurk in September, including the likely onset of tapered asset purchases by the U.S Federal Reserve, ongoing struggles in emerging economies like India and Indonesia, and the developing impacts of one of the sharpest government bond yield spikes in history. Second, prospects for returns from some under-performing asset classes are beginning to improve, in our opinion. European stocks, commodities, emerging market stocks and even some areas of the bonds market all look more competitive with U.S. equities on a forward looking basis than they did at the beginning of 2013.

For the first time in years, returns from a diversified portfolio strategy are badly lagging returns from a simple stock market portfolio. Even for investors who believe (as we do) that stocks remain relatively attractive when compared with other assets, we think it is unwise to ignore the long-term evidence in support of diversification.

Keep your balance.

1Available at https://www.columbiamanagement.com/market-insights/white-papers/EngineeringRetirement. See Appendix B.

Disclosure

Diversification does not assure a profit or protect against loss.

The Sharpe ratio is a measure that indicates the average return minus the risk-free return divided by the standard deviation of return on an investment.

The views expressed are as of 8/26/13, may change as market or other conditions change, and may differ from views expressed by other Columbia Management Investment Advisers, LLC (CMIA) associates or affiliates. Actual investments or investment decisions made by CMIA and its affiliates, whether for its own account or on behalf of clients, will not necessarily reflect the views expressed. This information is not intended to provide investment advice and does not account for individual investor circumstances. Investment decisions should always be made based on an investor's specific financial needs, objectives, goals, time horizon, and risk tolerance. Asset classes described may not be suitable for all investors. Past performance does not guarantee future results and no forecast should be considered a guarantee either. Since economic and market conditions change frequently, there can be no assurance that the trends described here will continue or that the forecasts are accurate.

This material may contain certain statements that may be deemed forward-looking. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those discussed. There is no guarantee that investment objectives will be achieved or that any particular investment will be profitable.

There are risks associated with fixed income investments, including credit risk, interest rate risk and prepayment and extension risk. In general, bond prices rise when interest rates fall and vice versa. This effect is more pronounced for longer-term securities.

Investment products are not federally or FDIC-insured, are not deposits or obligations of, or guaranteed by any financial institution, and involve investment risks including possible loss of principal and fluctuation in value.

Securities products offered through Columbia Management Investment Distributors, Inc., member FINRA. Advisory services provided by Columbia Management Investment Advisers, LLC.

© 2013 Columbia Management Investment Advisers, LLC. All rights reserved. 719126