As Uncertainty Abounds in September, Sideways Consolidation Continues

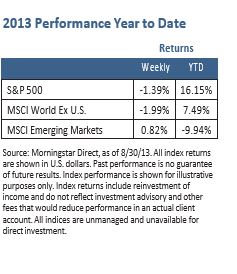

Global equities struggled last week, with the S&P 500 declining -1.39%.1 Volatility rose from geopolitical uncertainty over the military strike in Syria.2 Oil prices spiked with concerns about escalation and tension but retreated due to dampened international support and expectations that a military campaign would be short-lived. The U.S. Treasury announced its borrowing capacity will be exhausted by mid-October, exposing contentious fiscal battles. Reports mentioned former Treasury Secretary Larry Summers may be leading the succession race for Fed Chairman.

GDP is Rising but Sustained Progress is Not Evident Yet

Second quarter real GDP was revised upward to 2.5% from 1.7% due to higher net exports. The economy appears to be gaining momentum, after bottoming at 0.1% in the fourth quarter of 2012 and increasing to 1.1% in first quarter.3 However, we think momentum may be interrupted based on recent weak data.

Current Macro Themes

1. Deleveraging pressures and growth conditions vary across the globe. Policy settings are accommodative and support stronger economic activity. Global economic recovery remains subdued but is gradually gaining traction and broadening. Inflation is below target in almost all economies, permitting policy makers to keep rates anchored. Substantial slack within product and labor markets of major developed economies has put downward pressure on labor, materials and selling prices. Longer-term implications should include gradually increasing government bond yields and higher equity prices.

2. Comparing equities versus Treasuries is not conclusive in the short term. In our opinion, Treasuries have become oversold, and the expected date for federal funds rate hikes has been moved too far forward. Equities have experienced double-digit gains, while consensus earnings expectations have fallen steadily this year. We expect an extended stretch of sidewise consolidation and cooling off period. We believe equities remain attractively priced relative to Treasuries and other fixed income. Catalysts such as earnings growth may be needed for equities to advance. Our long-term view continues to support equities over Treasuries.

3. The federal budget deficit is falling sharply due to tax increases and the sequester. The deficit should continue to improve unless recessionary conditions resurface. The growing cost of entitlement programs will likely have negative implications for the deficit around 2015. We don’t foresee an agreement to reduce the deficit soon, making the long-term U.S. budget outlook unsustainable.

4. A confluence of fiscal and monetary policy factors could lead to greater policy uncertainty and market volatility. The likelihood of volatility increases with issues occurring simultaneously such as Fed tapering, selection of the next Fed Chairman, 2014 budget resolution and the debt ceiling increase. Working through the fiscal policy stalemate to reach agreement will be needed as the Fed begins tapering. We believe the key to reducing uncertainty about fiscal policy is House Republicans unifying around a plan.

5. Cyclical factors are lining up for a new capital expenditure (CAPEX) cycle. The key cyclical driver behind CAPEX is the difference between the return on capital and the cost of capital. So far, returns on capital seem to be greater than the cost of borrowing, suggesting profitable investment opportunities. Bank loans are growing and corporate bond yields are low, confidence in the corporate sector is increasing, and corporations have built up large cash positions, which could lead to capital investment.

The Big Picture

The combination of overbought conditions, rising bond yields and uncertainty about monetary policy has triggered a modest correction in developed and emerging market equities. Although a bond bear market appears to be underway, we remain optimistic about equities. We anticipate the current setback will give way to renewed gains once Fed tapering starts and the bond market calms, and revenue and earnings growth begin to accelerate.

The global economic expansion is just over four years old, but we don’t yet see the environment that typically signals an end to a recovery. Importantly, the major central banks continue to actively stimulate growth. Corporate earnings seem to have further cyclical upside, perhaps as do valuations, if bond yields rise more gradually going forward.

1 Source: Morningstar Direct, as of 8/30/13. 2 Source: Volatility as represented by CBOE Volatility Index® (VIX®), http://www.cboe.co2. 3 Source: U.S. Department of Commerce Bureau of Economic Analysis, “National Income and Product Accounts Gross Domestic Product, 2nd quarter 2013 (second estimate); Corporate Profits, 2nd quarter 2013 (preliminary estimate),” August 29, 2013, http:// www.bea.gov/newsreleases/national/gdp/gdpnewsrelease.htm.

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float- adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Non- investment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

GPE-BDCOMM5-0813P

© Nuveen Asset Management