My colleagues Mauro Ratto, Head of Emerging Markets, and Yerlan Syzdykov, Head of Emerging Markets – Bond & High Yield, offered these thoughts on emerging markets.

The emerging markets (EM) bond space experienced significant changes in the last decade, surging in size, improving in quality, offering investors a composite asset class with higher liquidity, transparency and potential for diversification.

Have we seen constant demand in the emerging market bond space similar to the U.S. fixed income markets?

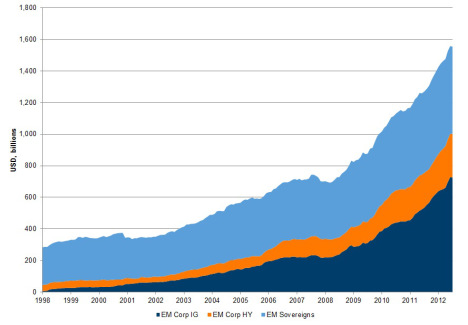

The EM bond universe has grown at an average annual rate of 12% in the last 15 years, passing from a niche market, valued at $285 billion at the end of 1998 to $1.555 billion as of June 2013¹. Its size (including corporate and sovereign) is now larger than the U.S. and Euro high yield space combined, making it an increasingly important segment for bond investors.

How has the emerging market bond space evolved over time?

The evolution of the market is not just a matter of size, but also a matter of composition. From being an asset class mainly limited to sovereign bonds, which accounted for more than 80% of the EM bond size in 1998, this industry has now become a more diversified space with corporate bonds accounting for over 50% of the EM bond market.

With a more diversified composition, has there been an increase in issuance?

Yes, another structural change has occurred in the EM corporate bond segment, which has moved from being a small universe of mainly high yield issuers based in Latin America in the late 90s, to a varied universe, which now includes issuers from all of the emerging areas (Asia, Europe, Middle East, Africa and Latin America). The majority of these bonds are investment grade. The growth of the EM investment grade corporate segment in recent years is impressive, with the size of the segment being almost 6 times that in 2005. Today, the EM corporate segment accounts already as much as the U.S. high yield market, and its size looks to continue to rise, as the market sets new records in EM corporate issuance.

Growth of Emerging Markets Bond Universe

¹Source: Bank of America Merrill Lynch, data as of June 30, 2013

What are some of the changes we’ve seen with the investment grade corporate issuers?

Another important development both in the sovereign and corporate spreads is the improvement in the quality of issuer. At the sovereign level, the debt to Gross Domestic Product (GDP) ratios generally improved and public finances have become stronger. This has allowed some emerging market countries to implement expansionary fiscal policies to contrast global contraction. Corporate fundamentals have also improved. Emerging market corporates are operating with more liquid balance sheets and lower financial leverage, which has resulted in higher credit ratings.

What other indications towards financial globalization have we seen in emerging markets?

While developed economies have been on the side of this last globalization phase, EM have been at the center, absorbing capital and also providing capital through foreign direct investments outflows, especially directed into other emerging economies.

Proceeding on the path of financial globalization requires that financial markets are able to handle and manage capital inflows. The expansion and evolution of the EM bond universe, as outlined, is moving in this direction. Improvements in liquidity, transparency, and the potential of diversification, which this composite asset class is experiencing, are important for answering the needs of global demand. Demand, that is expected to remain supported by low interest rates in advanced economies and the positive perspectives of emerging economies.

© Pioneer Investments