Since Ben Bernanke’s misinterpreted comments on tapering, Detroit’s bankruptcy filing and the even more recent, well-publicized concerns regarding Puerto Rico, the municipal bond market has struggled mightily. Year-to-date as of September 5, the Barclay’s Municipal Investment-Grade Index is down 5.3%, and the Barclay’s Municipal High Yield Index is down 8.3%.

The media has “piled-on” and the market has been vilified in the courtroom of public opinion. We’ve all heard the sayings, “Headlines sell papers” and “Don’t believe the hype,” but investors appear to be jumping on the negative bandwagon, even though key underlying municipal market fundamentals remain strong:

- Low default rates

- Improving state revenue collections

- High tax-equivalent yields

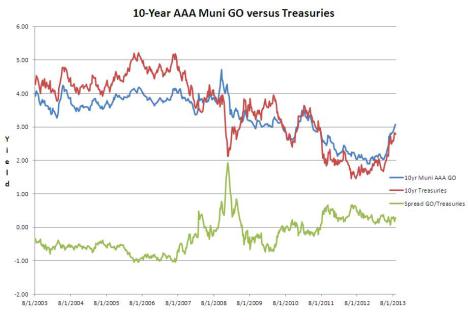

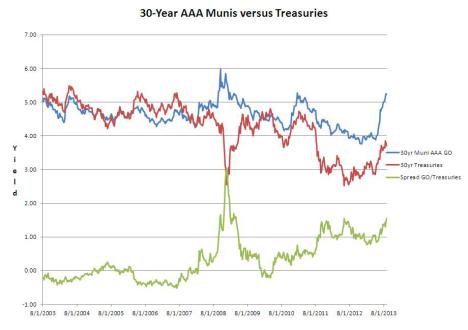

- And ever more attractive valuations (Rising Municipal/Treasury ratios – see chart below – are currently 113% and 119% on the 10-year and 30-year, respectively).

Source: Bloomberg. Last data points, 8/30/13

While the media may overgeneralize or paint this market with a “broad brush,” it is very important to note the following:

- The municipal market is substantial in size and represents an extremely diverse universe of states, cities, counties, districts, maturities and sectors. The market has about $3.7 trillion (debt outstanding) and is comprised of nearly 100,000 different issuers. The reality is that the municipal market is significantly larger than any singular troubled city, state or territory and can absorb isolated areas of stress.

- Troubled areas such as Detroit or Puerto Rico do not represent “new” news despite recent headlines. They have been distressed for some time. For example, in 2009, Moody’s downgraded Detroit to below investment grade (Ba2), and followed shortly with another downgrade to Ba3, foreshadowing the financial struggles that the city has today. The reality is that municipal defaults remain rare and this year (post-Detroit), defaults equate to only 0.18% of the $3.7 trillion market. It is true that other cities have their share of budget problems, but many are actively seeking solutions. Therefore, we do not believe Detroit will create a domino effect on the municipal market.

- On average, the broad and diverse municipal market is AA-rated, and about two-thirds of the market consists of revenue bonds; that is, bonds that are secured by income-producing facilities of the borrower, and generally include debt service reserve funds to further back the revenue pledge.

We believe the fundamentals of the municipal market signal opportunity. Tune out the noise!

© Pioneer Investments