Rates Update: Rationale for the Continuing Sell-off and Distinctions between 1994 & 2003

The bond market continues to struggle to find support, with 10-year Treasury yields touching 3%, a sell-off of roughly 140 bps in the last 4 months! While reduced dealer risk capacity and impaired investor loss tolerances are two underlying factors contributing to recent rates volatility, this violent move to higher yields has been primarily led by expectations that the Fed will begin to taper asset purchases in their upcoming meeting on September 18th. While recent weak data could reduce the exact size (and possibly start date) of tapering, a clear regime change has occurred within the committee – initiated by Jeremy Stein’s Overheating in Credit Markets speech and furthered by John Williams’ A Defense of Moderation in Monetary Policy. The Fed is now looking to reduce its overwhelming distortion of the rates market as the costs have been deemed to outweigh the benefits, given a dysfunctional portfolio balance channel that has resulted in increased wealth inequality but persistently tepid job growth.

Another dynamic pushing yields higher is the increased likelihood of Larry Summers getting the Fed Chair nomination due to his close relationship with President Obama. Summers has been vocal against the effectiveness of quantitative easing and with Summers emerging as a clear favorite over Janet Yellen, the market has priced in the Fed tapering asset purchases more aggressively.

The recent sell-off in Treasuries has been similar in magnitude to the sell-offs of 1994 and 2003. All three resulted in 140 to 190 bps sell-offs in the 10-year rate within a 4 month time period.

Comparing Recent 10-year Sell-offs

Source: Bloomberg

Yet, while the moves are similar, the catalysts for each sell-off have been strikingly different.

The 2003 sell-off was led by mortgage convexity related selling in the intermediate sector of the curve as durations extended and panicked selling led to further duration extensions and further selling. This recent sell-off has been focused in the same part of the curve and has been the result of some convexity led concerns, but by taking down a significant amount of agency MBS supply, the Fed has extracted a large amount of negative convexity from the marketplace, which they are not actively duration hedging.

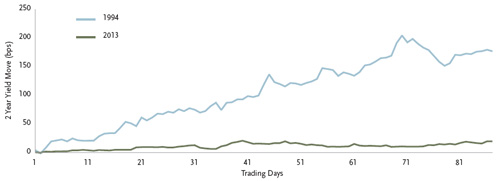

The most recent sell-off therefore has primarily been a reaction to concerns over Fed tapering. The 1994 sell-off coincided with Alan Greenspan hiking the Fed funds rate from 3% to 6%. These hikes took place in a different era of Fed transparency and were therefore not well telegraphed, catching the market by surprise. This current sell-off is fundamentally different because the Fed remains committed to keeping the Fed funds rate near zero as long as the quantitative thresholds of a 6.5% unemployment rate with 2.5% inflation remain unreached. As a result, the very front end of the curve has not re-priced to higher yields in the same manner that it would if the Fed was hiking, which can be seen by comparing the recent 2-year sell-off to that of 1994:

Current vs. 1994 2-year Sell-offs

Source: Bloomberg

Most of the current Fed funds rate hikes are priced for 2015 and beyond (largely beyond the maturity of a 2-year note). While this is consistent with an increased reliance on forward guidance, the fact that the current funds rate remains near zero creates uncertainty as to the path that will take us to those higher Fed funds expectations in the future. Put differently, the Fed’s expanded balance sheet obscures their reaction function to stronger economic growth going forward.

Which brings us back to a recurring premise: the current reach of Fed policy is unprecedented. Past policy comprised of increasing or decreasing the funds rate through economic cycles. Future policy will have to balance a reduction of purchases, re-investment of dividends, interest paid on excess reserves, maintaining a targeted balance sheet size, a traditional Fed funds target and forward guidance of that target.

The added complexity for future monetary policy should result in heightened uncertainty, higher realized rates volatility, increased risk premium out the curve, and fatter tails for the future distribution of yields. Portfolios should be protected accordingly.

Source: Bloomberg

Legal Disclosures

Any issuers or securities noted in this document are provided as illustrations or examples only, for the limited purpose of analyzing general market or economic conditions, and may not form the basis for an investment decision. TCW makes no representation as to whether any security (or the security of any issuer) mentioned in this document is now or ever was held in any TCW portfolio. TCW is not recommending the purchase, sale or holding of any security and is making no representation or indication of its own holdings of any securities. TCW may in fact be currently recommending the purchase of a security or the sale of a security regardless of any statement made in this document about that security or whether TCW owns it or not. Discussion of securities in this document are strictly for educational use only and are not intended to serve as investment advice. Any statement made in this document, including any statement or implication drawn from any discussion of individual securities, is subject to change at any time, without notice.

For Information Only

This publication is for general information purposes only. Past performance is no guarantee of future results. While the information and statistical data contained herein are based on sources believed to be reliable, we do not represent that it is accurate and should not be relied on as such or be the basis for an investment decision.

Subject to Change

Any opinions expressed are current only as of the time made and are subject to change without notice. TCW assumes no duty to update any such statements. The views expressed herein are solely those of the author and do not represent the views of TCW as a firm or of any other portfolio manager or employee of TCW. Any holdings of a particular company or security discussed herein are under periodic review by the author and are subject to change at any time, without notice. In addition, TCW manages a number of separate strategies and portfolio managers in those strategies may have differing views or analysis with respect to a particular company, security or the economy than the views expressed herein.

![]()

© TCW Asset Management