Many investors were conditioned to accept that the economy would be in the rehabilitation ward for the foreseeable future, rates would remain low, and monetary stimulus would continue unabated. It was an increasingly dangerous mindset. Now that’s changing with the slow but steady recovery of the economy and the Federal Reserve’s announcement in August that it may begin “tapering” its billions in monthly bond purchases designed to keep rates low and boost asset prices. These fiscal, financial and policy changes usher in the next great risk for bond investors: the potential return of higher interest rates. So I continue on the subject of “duration” and the risk that it poses to fixed income investors.

Not All Duration is Equal. Not All is Bad.

We’ve defined duration as: a measure of a fixed income instrument’s sensitivity to rising rates. In general, the longer the instrument’s maturity, the longer its duration, and the more sensitive its price will be to changes in market yields. The instrument’s value is the sum of cash flows received (interest payments and principal payments), discounted at the current rate demanded by investors for that instrument until its maturity.

While duration can be a harbinger of potential loss of principal – interest rates rise, bonds decline in value – not all duration is bad. There is spread duration, the calculation of the amount of spread (the yield difference over Treasuries) associated with a debt instrument’s underlying duration. The more spread (and therefore the higher the spread duration) the better. In fact, spread duration has the ability not only to help cushion the loss when rates are climbing, but provide strong and positive excess returns in a rising yield-curve and interest-rate environment. This is because “top-down” spread compression, which is often associated with an improving economy and therefore decreasing credit risk, can more than offset spread compression from the “bottom-up” (the result of higher yields demanded by investors in a rising rate environment).

Running to Short Duration for Cover

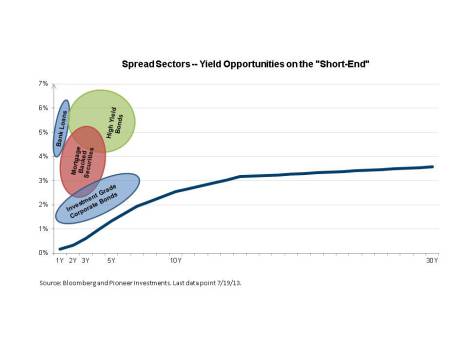

The math of spread duration and compression is not lost on bond managers. Investors in recent months have increasingly shifted exposure away from the long-end of the curve towards the short-end of the curve. This has led to dramatic spread and yield compression in the 0- to 5-year part of the high-grade corporate curve and has been largely responsible for the tremendous interest in high yield bonds (average duration of 4.2 years), bank loans (.25 years), non-agency mortgages (2-3 years) and generally anything that “floats” or adjusts to interest rates.*

But will this “rush” toward low duration end in tears as more and more investors abandon the long end of the curve, crowd into the short end, and ultimately drive spreads to levels that no longer even remotely compensate for credit risk or the risk of rising interest rates?

“Safe Haven” Sectors of the Past. Still Safe?

Are investors over exposed to fixed income? Or, given the strong recovery in high yield bonds and the relatively benign loss in bank loans, do they just have too much exposure to the wrong sectors? In my latest Pioneer Blue Paper, The Next Big Challenge to Investors: Duration, the third in a series on the subject, we examine each of the fixed income subsectors that have in the past been “safe havens” to investors in a rising rate environment, and ask the question: are they still “safe?”

© Pioneer Investments