Global factors influence market rise

Stocks generated robust gains last week on better-than-expected Chinese data and reduced likelihood of US military intervention in Syria. This led to sharp gains on Monday and Tuesday that carried through the rest of the week. The S&P 500 and Dow Jones Industrial Average gained 2.0% and 3.0%, respectively, in the period.

A resolution between Russia and the United States apparently averted unilateral US action last week in Syria. The nations agreed in principle to a plan to monitor, and ultimately remove, Syria’s chemical weapon stockpile. With few international actors willing to participate in an intervention, and the US’ own legislators conflicted about authorizing military force in the country, the compromise appears to solve for a moral conundrum for US leaders. Financial markets breathed a sigh of relief that the US would not become involved in another complicated foreign affair.

A series of economic indicators in China released early in the week pointed to a rebound in the world’s second largest economy. Exports kicked off the data cycle on Sunday, with shipments rising 7.2% in August year-over-year. This was well above the 5.5% figure expected by economists. It was followed by inflation figures that revealed consumer prices remain in check.

On Tuesday, China’s national statistics bureau announced that industrial production increased 10.4% over the past 12 months. This was higher than expected and represented an acceleration from the previous month. Additionally, retail sales grew 13.4% over the same period, two tenths higher than in July.

While some economists attribute the recent pickup in economic data in China to credit expansion earlier in the year (which has since trailed off), there is no doubt that the news is welcomed given the lack of organic growth elsewhere in the world. At a time when both developed and emerging countries are struggling to find their footing, China’s stumbles have served only to further spook global investors. August’s figures provide at least a temporary reprieve.

In the US, there were just a few reports of note during the week.

On Tuesday, the National Federation of Independent Business (NFIB) released its monthly Small Business Optimism Index. The series dipped by a tenth in August, approximately a point below expectations. NFIB’s index was decidedly mixed, with five components improving, four declining, and one unchanged. One thing that has not changed, however, is small business’ top perceived problems: taxes and government regulations/red tape.

On Thursday, the initial jobless claims series plummeted to 292,000, a decline of 31,000. This is by far the lowest reading of the recovery, but results should come with a very big caveat. According to officials, two states implemented computer upgrades, which prevented them from counting and submitting their data. One of these states was apparently a “large” state, which would presumably affect the measure in material fashion. Still, even excluding this past week’s report, this series has steadily trended down in recent months, indicating at least one side of the employment equation (layoffs) is improving.

The other major report form last week was retail sales, which came in soft in August. Sales rose 0.2% in the month, which was well short of expectations. This disappointment was somewhat eased, however, by an upward July revision from 0.2% to 0.4%. Moreover, the previous month’s core figure was 0.6%, which strips out the impact of motor vehicle and gasoline sales. Overall, it is yet another example of a mixed indicator for the US. The domestic economy appears to trudge ahead at a steady, if unspectacular, pace.

As we hit the home stretch for the third quarter, eyes will start to turn toward earnings reports in October. At least one observer noted that the recent pick up in the Citigroup economic surprise index is typically a good forward indicator for corporate results. As we have noted in recent quarters, with less room for margin improvement, earnings will be increasingly dependent on top line growth in a low growth world.

Source: Stocktwits.com

Consumers face an economy at a crossroads

As the Federal Reserve prepares to debate the merits of tapering its asset purchase program this week, a key area of the economy that will be closely analyzed by Bernanke and Co. is the health of the American consumer. There are tenuous signs that consumers are spending more, but attitudes towards the economic recovery are hardly encouraging. Consumers will find it difficult to stay the key cog of economic growth in the U.S., but at the very least, their participation in the recovery is imperative, and leaves much to be desired.

Entering the crisis, one of the biggest challenges faced by consumers was the amount of debt on their collective balance sheets. The household financial obligations ratio (FOR) as a percent of disposable personal income peaked at 18.9% in the third quarter of 2007. The FOR captures a broad mix of debt obligations across housing, auto, and consumer credit. Today, the FOR stands at 15.7%.

Source: Federal Reserve Bank of St. Louis

Despite a lessening debt load, consumers are feeling no better about their economic situation. A recent survey from Pew Research Center indicated that 63% of Americans feel “no more secure” than prior to the crisis and 33% feel “more secure.”

Source: Pew Research Center

Two challenges are causing broad frustration – wages and jobs. It is well publicized that the unemployment rate is stuck above 7% and there continue to be a dearth of available opportunities. According to the Bureau of Labor Statistics, there are 3.1 unemployed persons per job opening. That is improved from the 6.2 peak in mid-2009, but remains high on a historic basis.

Source: Bureau of Labor Statistics

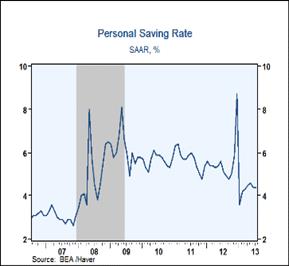

With job growth modest, there has been relatively little upward pressure on incomes. In the past year, personal incomes rose 3.3% and with wages growing slowly, consumers are once again relying more heavily on savings accounts to fund expenditures.

Source: Haver Analytics

Furthering the challenges, the recovery has not been identical for all segments of the population. In 2012, the top 1% of wage earners accumulated 19.3% of all household income and the top 10% of earners accounted for 48.2%. The income disparity between the top 1% and the 99% is at its widest margin since 1928.

Source: Center on Budget and Policy Priorities

The situation among lower income brackets is putting structural pressure on the economy. The supplemental nutrition assistance program (SNAP) now has nearly 50 million participants at a time when the employment-population ratio is near a generational low.

Source: Congressional Budget Office

Although income is becoming increasingly concentrated among the top 1%, jobs are a concern for everyone. Pew Research Center found that regardless of income or political party, the number one concern is the current job situation.

Source: Pew Research Center

The Federal Reserve may ultimately determine that economic conditions are “good enough” to warrant a reduction in asset purchases, but by most measures, the consumer is harvesting modest benefit from five years of Fed intervention. On the plus side, job growth is slowly returning and debt obligations are down significantly from before the crisis, but it will continue to be a challenged environment for the American consumer.

The week ahead

After a quiet week, economic data picks up significantly this week. Reports this week include consumer inflation, industrial production, housing starts, and existing home sales, among others.

More important than any data point, however, will be the FOMC meeting on Tuesday and Wednesday. All eyes will be on the Fed’s meeting announcement on Wednesday at 2pm, where it is widely expected that the initial tapering of QE policy will be announced.

One of the major topics that will dominate this week’s dialogue was Larry Summers’ withdrawal from consideration for the top Fed post over the weekend. Summers, along with Janet Yellen, were widely viewed as the front-runners for the job. While Yellen likely represents a continuation of the status quo, the enigmatic and outgoing Summers was seen as more of a wildcard for financial markets.

The other major piece of news this week surrounds German elections on September 22. Current chancellor Angela Merkel is expected to win again, although she may be forced to run a coalition government.

Other central banks meeting this week include Turkey, South Africa, Switzerland, Norway, and India.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value

© Fortigent