As summer is trailing off here in Milwaukee, WI, my wife and I have been revisiting some classic children’s games with our young son and daughter. Most recently, the biggest hit has been “Duck, Duck, Goose.” And, it’s a real treat to watch the extreme anticipation in their faces as they wait for the goose to be called and the running to begin.

It’s probably a stretch to compare “Duck, Duck, Goose” with the stock market, but I certainly can relate to the anxiety associated with an upcoming change. And it feels as though, over the last several years, the active investment community has been caught in the world’s longest game of “Duck, Duck, Goose.”

Let me explain why.

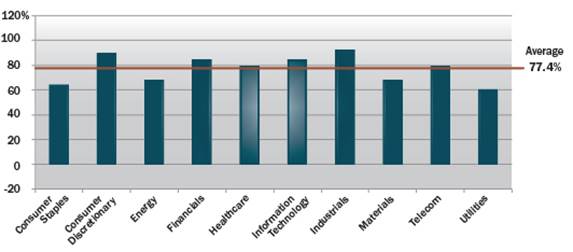

Since 1995, sectors within the S&P 500 have had a correlation with the broader market -- the Index, the S&P 500 -- of 77%.

Historical Correlations Among S&P 500 Sectors

Source: FactSet Research Systems, 12/29/1995 to 8/31/2013

A correlation of 100% would mean that a sector or a stock moves in line with the broader market. Conversely, a correlation of 77% would mean that there’s room for outperformance or underperformance versus the broader market.

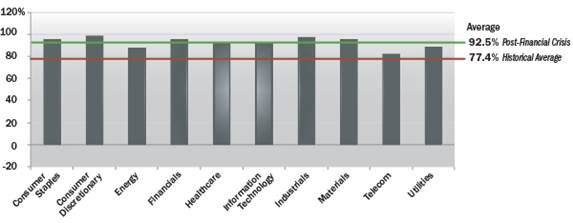

What’s interesting, over the last several years, really since the peak of the financial crisis in September of 2008 up until last month, correlations are up significantly -- nearly 20%* versus the long-term average.

Correlations: Historical vs. Post-Financial Crisis

Source: FactSet Research Systems. Post-financial crisis, as noted by the grey vertical bars and green horizontal line, is 9/1/2008 to 8/31/2013 Historical average, as noted by the red horizontal line, is 12/29/1995 to 8/31/2013.

So there’s been fewer big outperformers and underperformers within the stock market, and this has been excruciating for active investment managers like ourselves; we pride ourselves in identifying companies that we think will outperform the broader market.

I think there’s three reasons why correlations have picked up over this time period.

- It appears as though investors have been more focused on the macroeconomic landscape post the financial crisis -- and all the central bank actions that we’ve seen over this time period.

- And they appear to be acting more-so together, buying more together when they’re feeling more optimistic, and subsequently selling more when they get a little more worried. So, they’re moving en masse.

- And concurrently, over this time period, we’ve seen billions of dollars flow into passive investment strategies, such as ETFs.

Here’s the good news: It appears as though the “goose” is coming, or perhaps already has been called.

Why do we feel this way?

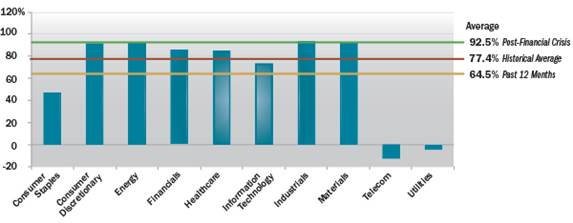

If you look at correlations over the past 12 months, they’ve dipped below the longer-term average.

Correlations: Past 12 Months

Source: FactSet Research Systems. Past 12 months, as noted by the blue vertical bars and yellow horizontal line, is 9/1/2012 to 8/31/2013. Post-financial crisis, as noted by the green horizontal line, is 9/1/2008 to 8/31/2013 Historical average, as noted by the red horizontal line, is 12/29/1995 to 8/31/2013.

So, it seems as though investors are more focused on the particular attributes or prospects for an individual company versus the macro.

And this is great news for investors like Heartland Advisors. We pride ourselves in understanding the merits and liabilities associated with a particular company. This is inherent in our 10 Principles of Value Investing™. So, while the market has not rewarded our active investment style over the last five years like it has over the longer-term, we believe the tide has turned and this painfully long waiting game could be finally coming to an end.

For more market perspectives, visit heartlandadvisors.com.

*Nearly 20% is based on a calculation of percent change, where 92.5 minus 77.4, then divided by 77.4 is 19.5%

Nasgovitz is CEO and Portfolio Manager for the Select Value Fund, and he is CEO of the Heartland Funds. He is also Portfolio Manager for one of the Firm's separately managed account strategies, Opportunistic Value Equity. He has 13 years of industry experience, 9 at Heartland.

Past performance does not guarantee future results.

The statements and opinions expressed herein are those of the presenter. Any discussion of investments and investment strategies represents the Funds' investments and portfolio managers' views as of the date of the video, and are subject to change without notice. All information is historical, not indicative of future results, and subject to change. The audience should not assume that an investment in the securities mentioned was or would be profitable in the future. This information is not a recommendation to buy or sell.

The S&P 500 Index is a widely used U.S. equity benchmark. It contains 500 U.S. stocks chosen for market size, liquidity, and industry group representation. Correlation is a statistical measure of how two securities move in relation to one another. A measure of 1 means the securities are highly correlated and move in conjunction. A measure of 0 means the securities are not at all correlated and do not move in conjunction.

The Heartland Funds are distributed by ALPS Distributors, Inc., and Will Nasgovitz is a Registered Representative of ALPS Distributors, Inc.

Separately managed accounts and related investment advisory services are provided by Heartland Advisors, a federally registered investment adviser. ALPS Distributors, Inc., is not affiliated with Heartland Advisors

© Heartland Advisors