STOCKS SLIDE AMID NON-TAPER

Equity markets sold off last week, as investors continued to shed risk in the wake of the Fed’s unexpected “non-taper” two Wednesdays ago. The stock market has finished lower in six of seven trading sessions since then, including four of five last week. The S&P 500 is down nearly 2% since the FOMC decision.

Adding to market anxiety last week was the lack of progress by Congress in agreeing to a budget resolution to stave off a government shutdown. The drama has spilled over through the weekend, with equity markets plunging lower in early Monday trading. Treasury Secretary Jack Lew has publicly stated that the department can survive until October 17, but thereafter would be at risk of default.

Economic data was mediocre last week, as a handful of high profile reports hit the newswires.

On Tuesday, the S&P/Case-Shiller index indicated that home prices continue to rise, albeit at a somewhat slower pace than observed earlier in the year. The 20-city index rose 0.6% in July over the month, which was below analysts’ expectations of a 0.8% increase. Since reaching a 1.9% monthly gain in March, the series has gradually slowed on a month-to-month basis. Over the past 12 months, however, the report indicates housing prices have increased 12.4%, the highest level of the recovery.

New home sales came in roughly in line with expectations, increasing to a seasonally adjusted annualized rate of 421,000 sales. This follows a very weak July in which the series declined by 14.1%. In contrast to the Case-Shiller index, the median sales price is now down for the fourth straight month. The impact of higher mortgage rates appears to be filtering through to the new home market.

On Wednesday, the final estimate of second quarter GDP was released. The Bureau of Economic Analysis, which prepares the statistic, announced no change from August’s second estimate of 2.5%. This represented a slight disappointment to economists, who predicted a modest uptick to 2.7%. Still, second quarter growth more than doubled Q1’s 1.1% rate, although many believe the third quarter will be another weak period.

Personal spending and income data inform part of this opinion on Q3 growth, which was released on Friday. Personal consumption expenditures are chugging along at a fairly steady but muted level. In August, PCE increased 0.3% after 0.2% growth in July. August’s figure was in line with consensus estimates.

Incomes fared somewhat better, coming in at 0.4% for the month. This also was in line with expectations. Encouragingly, the wages & salaries component of the figure rebounded from a 0.3% decline in July. Other sources of income in the report include components like proprietor’s income, rental income, and investment income, among others.

Overall, it was another middling week for economic data in the US. The economy appears locked into a stable, yet unexciting, trajectory of growth.

EUROPE POKES ITS HEAD OUT FROM THE SHADOWS

With all the focus on affairs in the US, China and developing nations, Europe has largely been given a free pass in recent months. The lack of attention gave Europe the opportunity to fix some of its troubles, but challenges remain and are likely to surface in the weeks ahead.

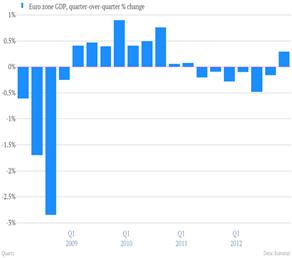

From an economic standpoint, the second quarter showed the first positive signs of growth for the Eurozone following six quarters of economic contraction.

Source: Quartz

Also encouraging is the economic improvement in countries like Spain. Spain’s trade deficit fell to $1.07 billion in July with exports rising 1.3% in the past 12 months and imports falling 3%.

Source: Quartz

In the manufacturing sector, European countries are showing improvement as well. The European flash PMI held above 50 in September, indicating expansion in the manufacturing sector.

Source: Econoday

Relative improvement in the economy is reflected in government bond markets, where yields on any number of peripheral European countries are dramatically lower than early 2012. Greece, Portugal, Italy, Spain and Ireland have all seen their yields collapse.

Source: Reuters

As economic data improves, the political landscape remains fractured. In Italy, the center-right People of Freedom (PDL) party resigned after being unable to reach a budgetary agreement designed to keep the deficit below 3.0% of GDP. The resignations were unexpected and the timing is sub-optimal as Italy is scheduled to submit its draft budgetary plans to European cohorts by mid-October. It is believed that Italy’s government will cobble together a plan for the time being before general elections next spring. It remains to be seen where Italy’s parliament goes from here, but at the very least, economic and market volatility is likely to increase as a result.

In Portugal, weekend elections for municipal mayors sent a strong austerity message. The ruling Social Democrat party only won 26.5% of the vote against 36.3% for the Socialist party. It proved to be the worst defeat for the Social Democrat party in more than two decades. Voters are no longer tolerant of the austerity measures accepted by politicians in conjunction with the country’s 2011 bailout. Once again, the timing may be sub-optimal, as there is some expectation Portugal will be forced to request a second bailout in the coming months. Standard & Poor’s placed Portugal’s BB debt rating on negative watch based on those concerns.

The last pending challenge for European officials could be the banks. Excess reserves in the banking sector are falling quickly, relative to the US where they expand week after week. This is a function of banks repaying funds borrowed from various government programs, but the end impact is a tightening of monetary conditions. For an already weak economic environment, tighter monetary conditions will restrict lending and act as headwind to growth. European Central Bank President Mario Draghi will not want to immediately react and fix the problem, but he may be left without a choice if reserves continue on their current trajectory.

Source: SoberLook

Europe has shown modest signs of economic improvement in 2013, but many of the previous issues remain intact. The political landscape is divided and unlikely to resolve itself easily. It will be important to pay close attention to countries like Italy and Portugal in the months ahead, where volatility could reemerge quickly.

The Week Ahead

As the third quarter closes out and the fourth quarter begins, there will be a few important reports for investors to digest this week. That includes the Employment Situation report released on Friday, where investors will gain additional information on the health of the labor markets. Economists expect a gain of 184,000 in nonfarm payrolls and no change in the headline unemployment rate for September.

On Tuesday and Thursday, the Institute for Supply Management releases its twin indicators, the manufacturing and non-manufacturing indices. Both have exhibited strength in recent months, but analysts foresee a modest retrenchment from robust levels.

Overriding all of the data this week will be negotiations in Washington over the budget. With a shutdown looming after the September 30 deadline, lawmakers are frantically attempting to cobble together legislation to avoid that income. Making matters worse for investors, media outlets have reported that Friday’s jobs report would not be released should the shutdown occur and persist through the week. Absent a last minute agreement, market participants should brace for some level of volatility this week given the added uncertainty of this situation.

On the central bank front, important policy meetings take place by the ECB and Bank of Japan. Neither group is expected to change policy. Other banks meeting include Romania, Australia, and Poland.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value

© Fortigent