What Happens if the Government Shuts Down and Nobody Notices?

Yes, this is a facetiously philosophical title (what is the sound of one hand clapping?) that pokes fun at the current situation in Washington. And we’re well aware that if Republicans and Democrats can’t reach a compromise in a couple of weeks to deal with the debt ceiling “time-bomb”, none of us will be joking around.

Apart from laying out a number of well-reasoned (we hope) hypothetical scenarios on how all of this mess will get resolved, there isn’t much we can fruitfully analyze. We are in the realm of “political uncertainty” in which emotions, hidden agendas, party affiliations and media grandstanding are the dominant drivers. And besides, with the shutdown in place, we can no longer access the numbers to pick them apart.

Contribution Analysis

As is the wont of most analytical types when faced with the unanalyzable, we turn to something we can analyze. And so I thought I’d take this occasion of political chaos to highlight a very interesting trend that has been developing over the past five years in this country… namely, the case of the incredible shrinking government!

Most people, when asked, would conclude that government has grown in size, influence and importance to the economy. Certainly, in terms of media attention, the government appears to be commanding more air-time. In fact, if you think about it, the office of the Presidency has increasingly taken on rock-star/monarchy type status while the House and Senate feel like a scene from Animal House. But, in terms of economic importance?

Well, as the saying goes, not so much . . .

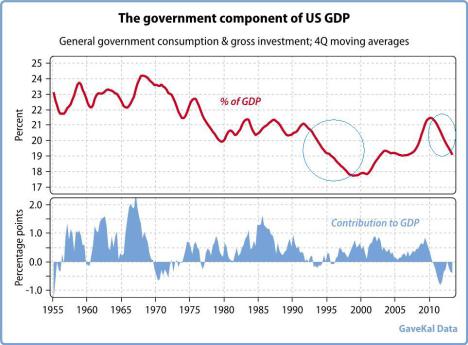

Our friends at GaveKal, an independent research firm, provided us with the chart below, which details the contribution of government spending (local, state and federal) to GDP growth over the last (almost) 60 years.

Source: GaveKal Data. As of 6/30/13.

There are a couple of interesting things to point out. During the equity bull market of the ‘90s, government expenditures as a percentage of GDP were shrinking and the contribution to GDP was negative. Many credit the decline in expenditures to Ronald Reagan’s supply side reforms, others to Clinton’s “peace dividend.” I’ll let you decide which political camp claims ownership.

I frankly don’t care what political party takes credit for the decline, as it’s clear that the economy and the U.S. equity Market (S&P 500 Index) benefited. Now, of course, this may be too simplistic a statement for some. There were a number of other factors contributing to the bull market era, including a secular decline in interest rates and the explosion of global trade. Neither of these trends appear to be likely catalysts in the coming years for a bull market in risk assets.

But it is curious that, in the recent period of awful average returns for the U.S. equity market (1/1/2000 – 3/1/2009), government expenditures as a percentage of GDP increased substantially. And, as the government’s contribution to GDP once again began to decline in 2009, the equity risk assets rallied. Hmmm . . .

It’s worth contemplating, given how anemic GDP growth has been over the past 5 years (~2%) relative to how strong equities have performed since their depths in 2009 (100%). Perhaps the conundrum is partially explained, at least, by the decline in government spending relative to the overall economy. Indeed, if we look at private vs. public contribution to GDP growth since 2009, it becomes evident that private sector GDP has been quite strong, on average +5% per year, while public sector GDP has detracted 1% per year from overall economic growth.

Maybe an extended vacation is just what the doctor ordered . . .

© Pioneer Investments