The following commentary summarizes prior financial market activity and uses data obtained from public sources. This commentary is provided to financial advisors and their clients as a resource for the management of assets and evaluation of investment portfolio performance.

The Economy

The economic environment in the third quarter was one of growth, albeit at a slower pace than most economists, and the Federal Reserve (“Fed”), believe can be self‐sustaining. The slow but steady gains the economy made were enough to buoy the stock market, but likely only because the Fed has seen it necessary to maintain its aggressive monetary policy. While employment gains were anemic during the quarter, the unemployment rate actually declined to 7.3%, largely due to a contraction in the labor force. Inflation, another key Fed indicator, remained benign, and well within the Fed’s target range. After establishing multi‐year highs in July, consumer confidence dropped significantly in August and September, primarily as a result of the rise in mortgage rates. Bright spots during the quarter were housing, which continued its robust recovery, and manufacturing, which reached its highest level since April 2011.

Globally, the situation in the eurozone continued to stabilize with several measures of economic activity improving both at the individual country level and in aggregate. Yields on sovereign bonds of countries that had previously encountered severe difficulties continued to trend downward, finishing the quarter at their lowest levels. In addition, the European Central Bank (ECB) has maintained a more accommodative posture, giving indications to the market that it will stand behind the bonds of troubled member nations. Against this backdrop, the euro currency ended the quarter at its highest level relative to the U.S. dollar since January.

One of the primary drivers of the lagging performance of emerging markets equities has been China’s economy. The country’s annualized GDP growth of 7.5% is slowing, and is not far above the post‐recession low of 6.6%. The country’s retail sales growth inched up a bit during the quarter but remains far below the pace of the past several years. China and the rest of the emerging Asia‐Pacific region are particularly sensitive to U.S. monetary policy, and the concerns about tapering that occurred in the third quarter had a material effect on those economies and markets.

The employment situation, one of the Fed’s key indicators for current economic conditions, took a step backward in the third quarter. The August payroll data (the latest available) disappointed, and the results from both June and July were revised downward significantly. The net effect was a further reduction in the average number of jobs added per month to the lowest levels this year. The disappointing employment situation is one of the primary reasons the Federal Open Market Committee (FOMC) opted not to scale back its quantitative easing program at its September meeting. Most economists continue to believe that employment gains will remain relatively muted the remainder of this year before accelerating in the latter half of 2014.

Once again there was no formal change to the Fed’s monetary policy in the third quarter. After much speculation that the Fed would taper its quantitative easing program, the central bank announced following its September meeting that it would be maintaining its program of monthly purchases of $45 billion of Treasury securities and $40 billion of mortgage‐backed securities. The Fed did leave open the possibility of scaling back bond purchases later this year depending on whether economic data shows sufficient improvement.

Highlights and Perspectives

GROSS DOMESTIC PRODUCT (GDP)

The Bureau of Economic Analysis released the third estimate of the second quarter 2013 real GDP, a seasonally adjusted annualized rate of 2.5%, up from the 1.1% annualized growth of the prior quarter. The acceleration was paced by investment in non‐residential structures, as well as an increase in exports and reduction in imports. In addition, the drag from government cutbacks lessened during the quarter, but this effect was partly offset by slower growth in consumer spending. Domestic corporate profits grew by 3.3% (non‐annualized) during the quarter, offsetting the profit decline of the first quarter. The profit gain was paced by domestic corporations, with financial companies posting the biggest advances. Inflation remains benign, with the personal consumption expenditures (PCE) index of prices gaining a modest 0.2% during the quarter. Many economists believe that the current lackluster GDP growth rate that has marked the last four years of the recovery should accelerate in 2014. If policymaking remains reasonable, and if the modestly positive trends remain in place, real GDP growth of 3% next year is feasible.

HOUSING

During the third quarter of 2013 the housing segment continued the upward trajectory of recent prior quarters. Analysts continue to assert that one of the primary reasons for the overall economy’s steady recovery is the positive turnaround in housing. Existing‐home sales for August (the latest monthly data available) advanced at an annualized rate of 5.48 million units, the fastest growth rate since the 2008 recession. The inventory of existing homes remained tight, with 4.9 months of supply. Existing‐home prices also continue to rise, with the median price up 14.7% from a year ago. In the new‐home segment, the NAHB Housing Market Index, a measure of homebuilding activity, ended the quarter at a level of 58, its highest point since 2005. The new‐home market may be facing some minor headwinds going forward, as mortgage rates have begun to rise and the supply of available land is becoming tight. Nevertheless, housing analysts believe any slowdown may be temporary due to short supply, pent‐up demand and an economy that is poised to accelerate.

EMPLOYMENT

The employment situation turned modestly disappointing in the third quarter, posting weak and lower‐than-expected payroll gains. Much of the weak gains came from slow growth in the service sector, including financial services firms. The August payroll report, the latest available, showed a gain of 169,000 jobs, below consensus expectations of a gain of 180,000. Perhaps more troubling, the gains posted for the prior two months were revised downward by a total of 74,000. The average number of jobs added for the three months ended August was only 148,000, the lowest so far this year. Despite the slow payroll growth, the unemployment rate actually declined in August to 7.3%.

However, while this may seem like good news, the reasons for the decline were that the labor force contracted by 312,000, and the labor force participation rate fell to a post‐recession low of 63.2%. Signs of encouragement in the latest report were gains in manufacturing and a lengthening of the workweek in some segments. The lackluster employment gains were a primary reason the Fed decided not refrain from tapering its quantitative easing program at its recent meeting. Economists believe that payroll growth will remain in the 160,000-180,000 range for the remainder of the year before accelerating to about 200,000 per month in the second quarter of 2014.

FED POLICY

The Federal Open Market Committee (FOMC) once again stood pat during the third quarter, maintaining existing policies. The FOMC kept in place its monthly program of buying $45 billion of Treasury bonds and $40 billion of mortgage‐backed securities, going against the consensus expectations the FOMC itself had helped establish. Since late May, markets had been handicapping a tapering in the bond‐purchase program, largely because of statements Fed Chairman Ben Bernanke made in congressional testimony. The consensus that emerged expected a tapering of approximately $10 billion per month to be announced at the FOMC’s September meeting. In the statement released following that meeting, the FOMC noted that its policymakers wanted additional signs that the economic recovery is sustainable before scaling back the quantitative easing program. Many economists believe the FOMC will move to taper in either October or December as the economy begins to gain momentum. The FOMC also maintained its existing target of 0%‐0.25% for the fed funds rate, and the consensus among Fed policymakers is that the rate will remain below 2% until the end of 2016.

INTEREST RATES

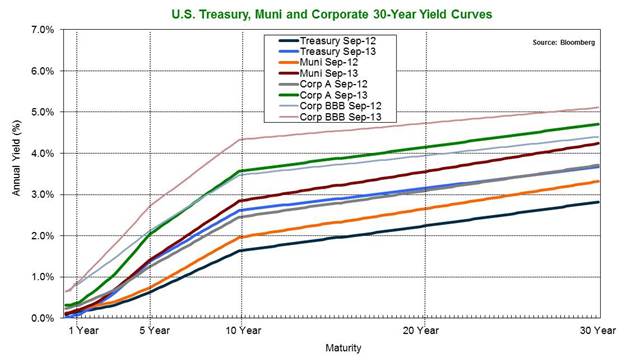

During the third quarter, fixed‐income securities continued to bear the brunt of investor expectations of Fed tapering, turning in volatile performance. Many fixed‐income benchmarks stabilized in July after posting their worst declines since 2009 in May and June, but then dropped again in August on renewed speculation about tapering. Prices rebounded sharply in September following the Fed’s announcement that it would not taper after all, at least not yet. Many market analysts and investors now expect the Fed to announce a modest reduction in bond purchases in either October or December, depending on the trajectory of the economy. When the smoke cleared at the end of the quarter, the yield on the benchmark 10‐year U.S. Treasury had risen to 2.61% from 2.49% on June 28th. Yields reached a quarterly high of 2.98% in early September, but dropped as investors bid up the prices of the bonds following the Fed’s announcement that it would maintain the current levels of bond purchases.

With this environment as a backdrop, yields were generally higher, particularly further out on the yield curve. The yield on the 3‐month T‐bill fell to 0.02% at the end of the third quarter from 0.03% the previous quarter. The yield on the five‐year Treasury remained relatively steady at 1.38% on September 30th compared to 1.40% on June 28th, and as mentioned above, the yield on the 10‐year Treasury rose to 2.61% from 2.49% over the same period. Inflation expectations heightened moderately during the quarter, with the Fed’s gauge of five‐year forward inflation expectations rising to 2.63% on September 30th from2.38% on June 28th.

Credit securities were less impacted by the speculation about when, and by how much, the Fed might taper its quantitative easing program. The yield on the Barclays 1‐3 Year Credit Index fell to 1.08% from 1.23% during the quarter. Intermediate credit yields were modestly higher, with the yield on the Barclays 7‐10 Year Credit Index rising slightly to 3.95% on September 30th from 3.88% on June 28th.Thegenerally positive environment for the equity market during the quarter was a positive for high‐yield securities, which bucked the general trend toward higher rates. The yield on the Barclays U.S. Corporate High Yield Index declined to 6.79% from 7.02% at the end of the second quarter. Municipal bond yields also trended higher during the quarter. The yield on the Barclays Municipal Bond index rose modestly to 3.08% at the end of the quarter from 2.91% as of June 28th.

EQUITIES

If one looked only at the quarter‐over‐quarter results, the domestic equity market seemingly continued to plod higher in a low‐volatility manner.

However, the third quarter was really a tale of three markets, each conveniently circumscribed by the individual months. In July the market rebounded sharply (the S&P 500 advanced +5.09%) from the negative performance posted in June, which was largely a result of fears about tapering. August’s dreadful equity market performance (the S&P 500 declined ‐2.90%) was attributed to two causes: 1) investors discounting the increasing likelihood of tapering in September and 2) concerns over the situation in Syria. In September, however, the market once again posted substantial gains (S&P 500 up +3.14%), both as a result of lowered geopolitical tensions as well as the Fed’s decision not to taper. For the entire quarter, the S&P 500 gained +5.24%.

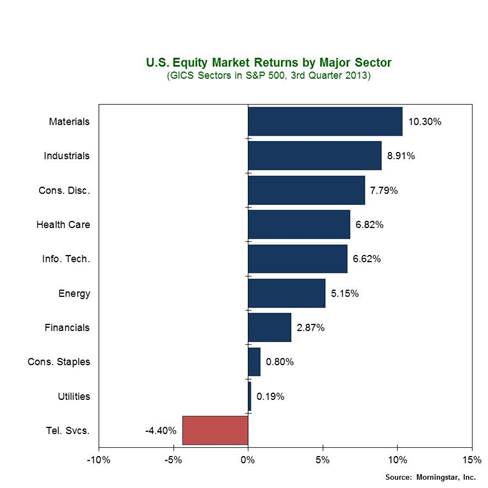

Sector selection during the quarter was of primary importance, as the ten primary economic sectors posted extremely varied performance, likely a result of the outlook for interest rates. Three of the most economically sensitive sectors were the top performers during the quarter. The materials, industrials and consumer discretionary sectors generated gains of +10.30, +8.91 and +7.79%, respectively. The telecommunications services, utilities and consumer staples sectors brought up the rear on a relative basis, generating ‐4.40%, +0.19% and +0.80% returns, respectively.

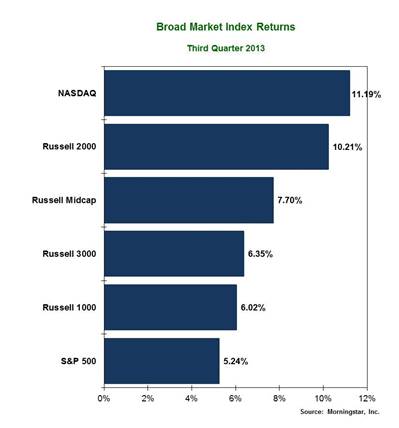

For the quarter, the Russell 1000 Index of large capitalization stocks posted a +6.02% total return. Within the large‐cap segment, growth stocks outperformed value stocks by a wide margin of 417 basis points. Small capitalization stocks, as represented by the Russell 2000 Index, outperformed large‐caps, ending with a total return of +10.21%. Growth stocks also outperformed value stocks within the small‐cap segment. The Nasdaq Composite, dominated by information technology stocks, generated a return of +11.19% during the quarter. The Dow Jones Industrial Average of 30 large industrial companies gained +2.12%.

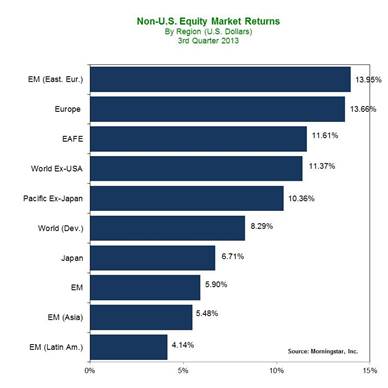

International stocks finally turned in a strong showing relative to U.S. equities during the third quarter. For several consecutive prior quarters international stocks had lagged domestic equities, in part due to the ongoing fiscal issues in the eurozone as well as a slowing in emerging markets economies. But the situation in the eurozone has quieted down, at least for the present, and valuations were attractive enough that investors looked for opportunities in foreign issues. The MSCI EAFE Index of developed markets stocks advanced +11.61% during the three months ended September 30th.International developed markets stocks have now outperformed U.S. stocks (as represented by the S&P 500) by 495 basis points over the past 12 months. One of the regions performing particularly well during the quarter was Europe, which saw yields on sovereign debt decline as tensions eased. The MSCI Europe Index ended the quarter higher by +13.66%. As with the past several quarters, emerging markets stocks lagged, but during September performed quite well on both absolute and relative bases. The MSCI Emerging Markets Index generated a return of +5.90% for the quarter but advanced +6.53% in September alone.

DISCLAIMER

The information, analysis, and opinions expressed herein are for general and educational purposes only. Nothing contained in this quarterly review is intended to constitute legal, tax, accounting, securities, or investment advice, nor an opinion regarding the appropriateness of any investment, nor a solicitation of any type. All investments carry a certain risk, and there is no assurance that an investment will provide positive performance over any period of time. An investor may experience loss of principal. Investment decisions should always be made based on the investor’s specific financial needs and objectives, goals, time horizon, and risk tolerance. The asset classes and/or investment strategies described may not be suitable for all investors and investors should consult with an investment advisor to determine the appropriate investment strategy. Past performance is not indicative of future results.

Information obtained from third party sources are believed to be reliable but not guaranteed. Envestnet|PMC™ makes no representation regarding the accuracy or completeness of information provided herein. All opinions and views constitute our judgments as of the date of writing and are subject to change at any time without notice.

Investments in smaller companies carry greater risk than is customarily associated with larger companies for various reasons such as volatility of earnings and prospects, higher failure rates, and limited markets, product lines or financial resources. Investing overseas involves special risks, including the volatility of currency exchange rates and, in some cases, limited geographic focus, political and economic instability, and relatively illiquid markets. Income (bond) securities are subject to interest rate risk, which is the risk that debt securities in a portfolio will decline in value because of increases in market interest rates. Investing in commodities can be volatile and can suffer from periods of prolonged decline in value and may not be suitable for all investors. Index Performance is presented for illustrative purposes only and does not represent the performance of any specific investment product or portfolio. An investment cannot be made directly into an index.

OUTLOOK

With many equity indices having posted solid double‐digit gains for the year in spite of lackluster economic progress, it seems appropriate to take a step back to analyze the prospects for stocks moving ahead. While markets cheered the Fed’s announcement that it would not taper in September, perhaps lost in the market’s subsequent rally was the fact that the Fed’s decision was made because the economy is not gaining the self‐sustaining momentum economists had previously expected. Equity markets, however, are known to be discounting mechanisms that forecast economic circumstances 6‐9 months in advance. So, even though economic growth hasn’t lived up to expectations in the past quarter or two, the market is likely looking ahead into 2014, when economists generally believe there will be an acceleration in activity. Should the Fed decide to taper either in October or, more likely, December, the market should be sufficiently conditioned to the possibility. In addition, the Fed is likely to taper only if economic conditions warrant, meaning growth – and the employment situation ‐ will be on an upswing. Despite the market’s rise over the past 12 months, valuations appear to remain reasonable, and the equity risk premium remains higher than its historical average. So, while a significant expansion in multiples is not likely, neither are multiples at levels indicating overbought conditions. One risk factor that bears close watching over the next few weeks is the environment in Washington, DC. Negotiations to keep the federal government funded remained at a stand‐still at the end of the quarter, and as of October 1st federal agencies suspended the vast majority of activities. How this eventually plays out, and whether it may have any lasting impact on the markets, remains to be seen. Of course, the longer it takes to resolve, the larger the impact on the economy.

INDEX OVERVIEW

The S&P 500 Index is an unmanaged index comprised of 500 widely held securities considered to be representative of the stock market in general. The S&P/Case‐Shiller Home Price Indices measure the residential housing market, tracking changes in the value of the residential real estate market in 20 metropolitan regions across the United States. The Morgan Stanley EAFE Index represents 21 developed markets outside of North America. The MSCI Emerging Markets Index is a free float‐adjusted market capitalization index that is designed to measure equity market performance in the global emerging markets. The Barclays U.S. Aggregate Bond Index is a market capitalization‐weighted index of investment‐grade, fixed‐rate debt issues, including government, corporate, asset‐backed, and mortgage‐backed securities, with maturities of at least one year. The Barclays U.S. Corporate High Yield Index covers the USD‐denominated, non‐investment grade, fixed‐ rate, taxable corporate bond market. Securities are classified as high‐yield if the middle rating of Moody’s, Fitch and S&P is Ba1/BB+/BB+ or below. The index may include emerging market debt. The Barclays Municipal Bond Index is an unmanaged index comprised of investment-grade, fixed-rate municipal securities representative of the tax-exempt bond market in general. The Barclays 1-3 Year Credit Index includes publicly issued U.S. corporate and specified foreign debentures and secured notes that are rated investment‐grade (BBB- or higher) by at least two of the major ratings agencies, have maturities between one and three years, and have at least $250 million par amount outstanding. The Barclays 7‐10 Year Credit Index includes publicly issued U.S. corporate and specified foreign debentures and secured notes that are rated investment‐grade (BBB‐ or higher) by at least two of the major ratings agencies, have maturities between seven and ten years, and have at least $250 million par amount outstanding. The DJ‐UBS Commodity Index Total Return measures the collateralized returns from a basket of 19 commodity futures contracts representing the energy, precious metals, industrial metals, grains, softs and livestock sectors. The Russell 1000 Index is a market capitalization‐weighted benchmark index made up of the 1000 largest U.S. companies in the Russell 3000 Index (which comprises the 3000 largest U.S. companies). The Russell Midcap Index is a subset of the Russell 1000 Index. It includes approximately 800 of the smallest securities based on a combination of their market cap and current index membership. The Consumer Price Index (CPI) measures the change in the cost of a fixed basket of products and services. The Gross Domestic Product (GDP) rate is a measurement of the output of goods and services produced by labor and property located in the United States.

Brandon Thomas

Managing Director

Chief Investment Officer

Envestnet | PMC

© 2013 Envestnet | PMC. All rights reserved