U.S. equities marked another all-time high last week as the S&P 500 increased 0.9%. (1) Global equities reached new cycle highs for the second week in a row. Many investors have concerns that the gains will not last since the world economy remains lackluster and the liquidity driving the current rally will eventually stop.

It’s Too Early to Say What’s Next

As witnessed this summer, simply talking about the end of monetary easing can substantially impact the markets. The world economy is seemingly not sending bullish signals for risk assets, as growth expectations appear stationary. The Fed has stated it will initiate tapering and eventual tightening only when the economy is stronger and shows progress in more than one variable. When economic data improves and the Fed begins to reduce or remove monetary stimulus, the impact on risk assets (credit and equities) should be muted because the underlying fundamentals will be stronger. In our opinion, equities remain the best asset class under this scenario.

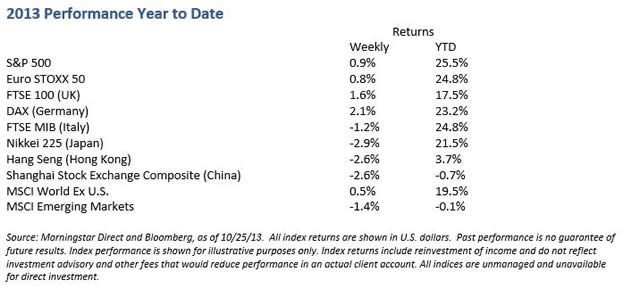

Fiscal policy discussions have overshadowed the simultaneous easing in three main reflationary variables: 1) the dollar is drifting lower, 2) U.S. Treasury yields have fallen slightly and partially recovered from the rapid advance earlier this year and 3) oil prices are easing, reducing the drain on consumer and business purchasing power. The reflationary push from these natural economic stabilizers should add to slow but steady positive economic momentum. U.S. equities have gained 25% year to date and the S&P 500 is above 1750,1 which is the outer end of the range we estimated at the start of the year. We believe the risk-reward tradeoff has become more neutral.

Weekly Top Themes

1. The U.S. budget agreement set these deadlines:

- December 13: The House-Senate Conference must reach agreement on a budget resolution.

- January 15: The continuing resolution that is funding the government runs out.

- February 7: The debt ceiling is currently suspended until this day, and the U.S. Treasury would need to begin extraordinary measures, potentially pushing off the true deadline until March.

We think the odds of a shutdown or another disruptive event are lower. A broader fiscal policy deal that will meaningfully impact the economy or future deficits remains highly unlikely.

2. The September employment report indicated a disappointing gain of 148,000 jobs. (2) Overall, this data confirms that the economy was soft in the third quarter, ahead of the government shutdown. This supports the growing perception that Fed tapering is unlikely before next March.

3. Almost 50% of S&P 500 companies have now reported third quarter earnings and 75% have posted earnings above the mean estimate, with aggregate earnings anticipated to exceed expectations by 3 to 4%. (3) Revenues are pacing slightly below expectations at -0.2%.3 Investors appear to be differentiating, as companies missing expectations are being punished and those beating expectations are being rewarded.

The Big Picture

The global economy has been solidifying recently and will likely continue on this track since the threat of a premature spike in bond yields has ended for now. Purchasing manager surveys have held their gains (4) and suggest better growth may be ahead. U.S. economic data will likely be somewhat uncertain over the next few months due to the impact of the government shutdown and subsequent startup. We expect the underlying firming trend to persist once the fog lifts. The payroll gain last week was less than expected, but forward-looking indicators remain upbeat and hiring plans and layoffs continue to move favorably.

Although the U.S. federal government has stolen the headlines, a stealth recovery seems to be underway at the state and local level, and finances have improved to the point that hiring is expanding. Equity valuations are now neutral in absolute terms, but we believe stocks compare favorably relative to bonds and short-term rates. Importantly, the slow-moving economic expansion and lagging central banks mean the window of opportunity for equity gains will stay open and a further re-rating is possible.

“If we are going to see significantly higher equity prices, at some point we need acceleration inearnings growth.”

Robert C. Doll, CFA

Chief Equity Strategist, Senior Portfolio Manager

Bob Doll serves as a leading member of the equities investing team for Nuveen Asset Management, providing reasoned analysis through ongoing market commentary and equity portfolio management. Follow @BobDollNuveen on Twitter.

1 Source: Morningstar Direct, as of 10/25/13. 2 Source: Bureau of Labor Statistics, “The Employment Situation – September 2013,” October 22, 2013, http://www.bls.gov/news.release/empsit.nr0. htm. 3 Source: FactSet Earnings Insight, October 25, 2013, http://www.factset.com/earningsinsight. 4 Source: Institute for Supply Management, “September 2013 Manufacturing ISM Report on Business,®” October 1, 2013, http://www.ism.ws/ismreport/mfgrob.cfm. Most recent data available.

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. Euro STOXX 50 Index is Europe’s leading Blue-chip index for the Eurozone and covers 50 stocks from 12 Eurozone countries. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. FTSE MIB Index is an index of the 40 most liquid and capitalized stocks listed on the Borsa Italiana. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Noninvestment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

© Nuveen Investments