ECONOMIC DATA IS MIXED

Equity markets moved incrementally higher last week, as the Dow Jones Industrial Average gained 0.3% and the S&P 500 was up 0.1%.

Economic data proved slightly positive, but markets were focused on the latest FOMC meeting. It proved less exciting than expected.

Based on recent data, the FOMC decided to maintain its current level of asset purchases at $85 billion per month. The FOMC statement was similar to recent releases, citing a moderate pace of economic expansion, but highlighting concerns about inflation and unemployment. A subtle shift occurred regarding housing markets, which the FOMC acknowledged has “slowed somewhat in recent months.” Given recent events in Washington, along with the downshift in housing markets, investors are now moving towards an expectation of taper later into 2014.

In addition to the Fed, several notable economic releases came out. Retail sales for September were disappointing at the headline, which showed a 0.1% decline for the month. Excluding the impact of autos and gas, however, retail sales were up 0.4%. Results excluding autos and gas were reasonably robust, led by gains in a number of sectors, including food & beverage, electronics & appliances, and furniture. The result was a mild surprise, as economists were anticipating no change. October may offer a different story, though, as the debt ceiling debate and budget discussions weighed heavily on consumer sentiment figures.

Source: Econoday

Speaking of consumers, the Conference Board’s Consumer Confidence Index dropped from 80.2 to 71.2. Underlying the headline index was a very poor reading for the expectations component (from 84.7 to 71.5) and a somewhat less dire slowing of the current conditions component. When asked about availability of jobs, 35.8% of survey participants reported jobs as hard to get. This points towards further weakness in labor markets.

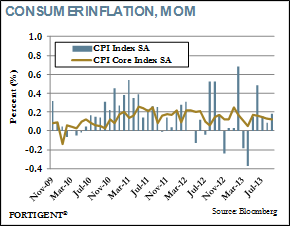

Beneficial for consumers, but frightening for Federal Reserve officials, is the recent trend in inflation. The consumer price index (CPI) increased 0.2% in September. Excluding the impact of food and energy, CPI was up 0.1%. Producer prices were similarly weak in September, with the producer price index (PPI) declining 0.1%. Excluding food and energy, PPI was up 0.1%. Federal Reserve officials are cognizant of the dangers of a deflationary environment and will work aggressively to ensure that does not occur, but with CPI up a mere 1.2% year-over-year, we are inching closer to a deflation scenario.

Manufacturing companies received more upbeat news with the ISM Manufacturing Index increasing from 56.2 in September to 56.4 in October. Readings above 50 indicate expansion in the manufacturing sector. Improvement to new orders was the notable positive, but there was some softness in employment.

EX-US PROPERTY BUBBLE PEAKING?

For several years now, a common storyline on China was the immense overcapacity in the country’s housing market. A mixture of easy credit policies and officials’ explicit economic growth plans based on capital investment yielded construction on a massive scale across the countryside. So-called ghost towns emerged as the pace of building and the migration of rural citizens into these cities fell out of sync.

Despite that overcapacity, property prices surged as investors and corporations snapped up real estate at a furious clip. Following the financial crisis, some property markets saw prices double and triple and squeeze out much of the country’s middle class from participating.

In recognition of these issues, Chinese officials moved swiftly to curb price gains in their property markets. They implemented policies such as increasing the required down payment on second homes, restrictions on the number of homes that could be owned, and a real estate transaction tax, among others. The ability for the central government to manage their economy left many observers sanguine about the potential property bubble, particularly as prices softened in late 2011.

However, a new dynamic emerging not just in China but across the world suggests a far greater problem is arising: property prices are surging in a number of the biggest metropolitan areas. The property bubble tag line is now being applied to places like London, Hong Kong, Singapore, and major cities in Australia, Canada, and, of course, China. And with US home prices now within 7% of their peak, according to data from the National Association of Realtors, some are also questioning the pace of US home price gains relative to stagnant income growth.

In Canada, for example, building permits recently reached record levels as building activity surges amid robust sales growth. Property sales in cities such as Vancouver, Toronto, and Calgary have reportedly jumped by more than 20%. But with housing-price-to-income ratios currently at 131.7 (a ten-year high), based on data from the OECD, it remains to be seen how Canadians can keep up with these price rises. For now, debt-to-income rations suggest it is occurring via increasing leverage.

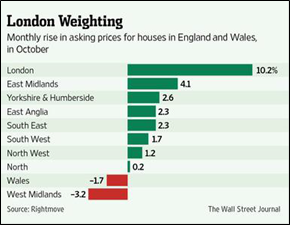

London, meanwhile, saw prices leap more than 10% in October alone, according to recent report by the Wall Street Journal. The country’s leadership is actively looking to impose a tax on foreign buyers, which are believed to be a major driver of recent price gains. Unlike local citizens who pay a capital gains tax on property gains for houses other than their primary residence, foreign owners are currently exempt from such taxation. Some estimates suggest that such buyers are purchasing approximately 70% of the newer, high-end construction.

Source: Wall Street Journal

The common thread, of course, is the massive level of coordinated quantitative easing occurring across the world. While the inflationary impact of all this liquidity has yet to manifest itself in much other than stock and bond markets, a secondary wave may now be spreading through global real estate markets. And globalization is contributing to the phenomenon: as previously described, foreign buyers are increasingly participating in the real estate markets of bigger urban centers.

China looms large given the relative size of its economy and impact on global demand. Despite the existence of measures designed to inhibit property price growth, many Tier 1 cities saw appreciation of nearly 20% year-over-year in September. This is a sharp acceleration from six months ago, and has left many fearing that officials are losing their handle on the sector. The influence of the global liquidity expansion could be an externality that China’s government just cannot account for.

Source: Financial Times

In an environment in which many of the world’s macroeconomic problems have seemingly receded, investors should keep their ears to the ground for potential left tail risks. Amid a period of relative calm, an unexpected calamity could throw financial markets back into a tailspin. An emerging global property bubble could be one such risk.

THE WEEK AHEAD

There remains a backlog of official government statistics to be released this week. Top of that list is October nonfarm payrolls, along with personal income, third quarter GDP, and consumer credit. The ISM will release the non-manufacturing survey on Tuesday.

A number of central bank policy meetings take place this week, include those in Australia, Russia, Poland, Czech Republic, and Peru. The European Central Bank will also hold a policy meeting Thursday, but there is no expectation of a change.

ABOUT FORTIGENT

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value

© Fortigent