Government Shutdown Doesn't Shut Down Markets in October

- The stage was set for an October selloff, but markets treated investors to another round of across-the-board gains.

- Headlines comparing today’s equity market with 1999 are way off; the current rally has been driven by solid corporate fundamentals, and the market remains compellingly valued.

- Global economic growth remains sluggish, and eventual Fed tapering is likely to introduce volatility into markets worldwide.

October’s first day was greeted by a shutdown of the U.S. government, and by mid-month the country was mere days away from a debt default that Treasury Secretary Lew predicted would lead to a “profound financial crisis”. Top it off with a bumbling rollout of the Obamacare website, and October had all the makings of a market disaster.

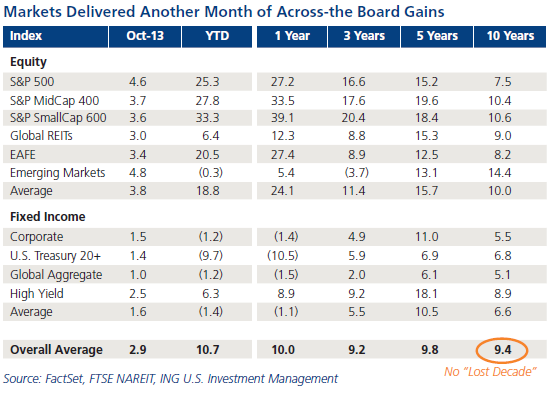

Not so fast. Instead of calamity, investors were treated to another round of across-the-board gains. The S&P 500 notched another huge advance to bring its year-to-date return to 25.3%, and mid- and small-cap stocks have delivered even better performances thus far in 2013. But the big — and somewhat overlooked — story in equities continues to be the turnaround in emerging markets, which have been outperforming the red-hot U.S. market over the last couple months.

Bonds, too, reveled in positive territory. Notably, long Treasury bonds — though still negative for the year — returned 1.4%, as yields fell on expectations that Fed tapering is far off. U.S. corporate and global bond indexes have narrowed their year-to-date declines and are now down only 1.2% each. Compare these performances to the supposed safe haven of gold. Gold has lost 22% so far in 2013 and is actually worth less on an inflation-adjusted basis than it was in the 1980s. Gold is a tricky asset to value because it pays no interest or dividends; essentially it is worth whatever someone is willing to pay for it. Investors have flocked to gold since 2008 on fears of hyperinflation and financial Armageddon; five years later, these fears have yet to come to fruition.

What Is Driving Markets to New Highs?

Should investors be worried about the rally that has pushed a number of markets to new record levels? We say no — this market is being driven by corporate earnings growth and supported by an influx of cash coming off the sidelines, fundamental factors that have little in common with the irrational exuberance that can sometimes push markets too far, too fast. While it is hard to ignore the headlines comparing this market to the party of 1999, there are in fact very few similarities between the two other than record-high index levels; for example, the price-to-earnings ratio of the S&P 500 in 1999 was 40, while today it trades at a much more compelling 15 times earnings.

Below we take a closer look at some of these fundamental factors.

Advancing corporate earnings. With more than 75% of S&P 500 companies having reported third quarter results, year-over-year earnings growth stands at about 2.7% and is on track to exceed the second quarter’s 2.1% growth. More important, sales growth seems to be keeping pace with earnings growth this quarter, suggesting good earnings quality.

Broadening manufacturing. Manufacturing contributes significantly to corporate earnings and has been expanding robustly; despite an idling government, the latest ISM manufacturing reading of 56.4% was the highest since 2011. Cheap natural gas — which we have been touting for several years as one of the tectonic shifts changing the global economic landscape — will continue to provide a tailwind for U.S. manufacturers. In fact, the U.S. is expected to overtake Russia this year as the world’s leading producer of energy.

Consumer as the game changer. Consumer spending funnels directly into corporate coffers; it has held up consistently in the face of various headwinds, and October’s slight downtick of 0.1% in retail sales is not surprising given the chaos in Washington and the loss of confidence that accompanies it. Additionally, the rocky start to the Affordable Care Act (aka Obamacare) has created uncertainty among a large block of consumers — notably the reported 16 million people potentially facing policy cancellation as a result of the law’s enactment — and damaged consumer sentiment in general.

There are positive signs from the consumer, however, which should help offset some of the challenges coming out of Washington. The housing rebound remains intact, with Case-Shiller reporting 12.8% year-over-year growth in prices in its latest release. An additional wealth effect from the stock market gains this year helps to further bolster confidence. Furthermore, it seems we have finally reached a turning point when it comes to confidence in U.S. equities. The Investment Company Institute (ICI) reported that funds holding U.S. stocks attracted $9.2 billion of inflows in the week ended October 23, the biggest weekly flow into the funds since ICI began tracking this data in January 2007. Investors are beginning to recognize that what they don’t own is one of the biggest risks they face today.

Developing markets. The International Monetary Fund (IMF) recently dialed back its expectations for 2014 global growth to 3.6%, from 3.8% previously. The devil is in the details, however; the IMF forecasts emerging markets to expand at a 4.7% rate, more than twice the pace of the developed markets’ meager 2.1% growth.

Global Risks Still Loom

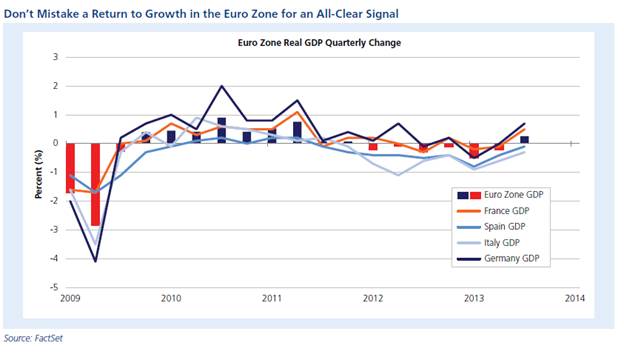

So what can rain on this parade? Europe, for one thing. Yes, the euro zone recently emerged from an 18-month recession, and even Spain notched positive growth last quarter. But don’t mistake very slight growth for an all-clear signal. The euro zone is still reporting unemployment of more than 12%, and economic momentum is nearly nonexistent. Additionally the latest inflation numbers out of Europe are troubling; annualized inflation fell sharply from 1.1% to 0.7%, the lowest level in four years and well below the European Central Bank target rate of 2%. We need only look to Japan and its struggles over the past two decades to see the economic havoc deflation can wreak.

We also have seen inflation slow here in the U.S. This has undoubtedly been on the Fed’s mind and coupled with the poor rate of jobs creation has lent credence to the belief that tapering will be delayed into 2014 despite the U.S. economy growing at a 2.4% clip. The nomination of the dovish Janet Yellen is likely to set the taper hurdle rate higher — or so the market believes and has priced in. But Ben Bernanke has one more chance to pull the trigger at December’s meeting. While the market likely would perceive tapering at that point as negative, it would actually represent an overall positive signal for the health of the economy.

Emerging markets are also a concern. Over the summer we watched a dress rehearsal of the likely impact of policy normalization; as interest rates in the U.S. began to rise, all of the hot money parked in emerging markets turned tail and fled. Interest rates will indeed rise at some point, and it is unclear whether or not the recent tapering reprieve has given countries like India and Indonesia sufficient opportunity to devise a Plan B that will avoid a currency crisis. Meanwhile, plummeting oil prices may have arrived just in the nick of time for economies dependent on oil imports like India, where crude oil accounts for one-third of its total imports. Interestingly, frontier markets have remained above the fray. They were not recipients of speculative inflows and therefore have enjoyed relative immunity from outflows. In fact, the MSCI Frontier Markets Index is up more than 20% this year.

A final risk is overall fundamental growth from the private sector versus that induced by government or central bank policy. While global central bank stimulus can provide an economic kick-start, it is an unsustainable substitute for fundamental economic activity. Despite the impact that eventual policy normalization likely will have on economies, opportunities abound; as mentioned earlier, the IMF expects emerging economies to more than double the economic pace of developed economies in 2014.

Investment Strategy in any Environment

Broad global diversification may seem like an outmoded concept when U.S. equity markets are climbing at breakneck speed. Investors can enjoy the ride of a surging domestic market, but they must also accept that ongoing global risks will from time to time present speed bumps in the form of volatility.

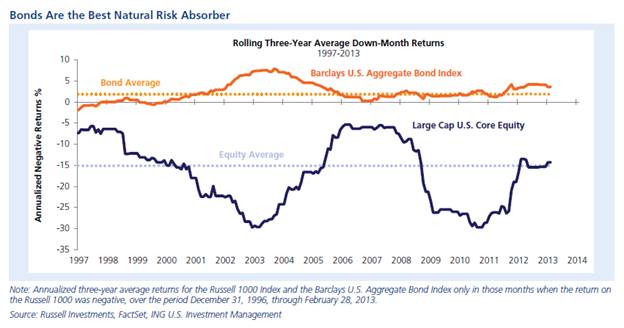

A diversified portfolio with broad exposure to equities and bonds both here and abroad helps smooth those bumps.

First a September surprise and now another one in October. Surprises are always welcome when they are on the upside, but we know that not all surprises are positive. So while this market definitely has room to run, it would not be imprudent to prepare for some of the less-welcome, but inevitable downside surprises likely to emerge in the future.

This commentary has been prepared by ING U.S. Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults (5) changes in laws and regulations and (6) changes in the policies of governments and/or regulatory authorities.

The opinions, views and information expressed in this commentary regarding holdings are subject to change without notice. The information provided regarding holdings is not a recommendation to buy or sell any security. Fund holdings are fluid and are subject to daily change based on market conditions and other factors.

Past performance is no guarantee of future results.

© 2013 ING Investments Distributor, LLC • 230 Park Avenue, New York, NY 10169

CID 7877