After a very rough second quarter, TIPS posted modest returns in the 2013 third quarter. By our calculations, TIPS gained 0.97% in the quarter, better than the 0.19% gain on comparable maturity straight Treasury securities. After the sharp second quarter sell-off, bargain hunters found value in the intermediate maturities for both TIPS and straight Treasurys.

At the end of the third quarter, the average breakeven spread on both 5-year and 10-year TIPS were little changed from their 2013 second quarter levels.

Chart 1

Yield Spread Between Constant Maturity 5-Year Treasury Notes and 5-Year TIPS: 2011-2013

Source: U.S. Federal Reserve data

Chart 2

Yield Spread Between Constant Maturity 10-Year Treasury Notes and 10-Year TIPS: 2011-2013

Source: U.S. Federal Reserve data

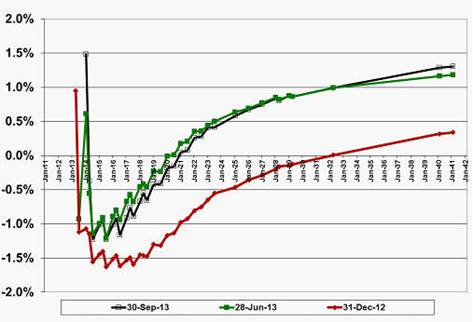

Chart 3 shows little change in the TIPS yield curve from the 2013 second quarter to the third quarter, but a big change from the beginning of the year.

Chart 3

TIPS yield curve: Dec. 30, 2012, Jun. 28, 2013 and Sep. 30, 2013

Source: Pricing obtained from Barron's and the Wall St. Journal; yields calculated by Lark Research.

During the 2013 third quarter, TIPS prices fell on average by less than 1/8 of a point, compared with a average plunge of more than 9 points in the second quarter. Short-term TIPS declined by about half a point and long-term TIPS fell by about 1 1/2 points, but intermediate-term TIPS gained a little over half a point.

At the end of the third quarter, TIPS yields were negative out to the 2020 maturities, about the same as at the end of the second quarter.

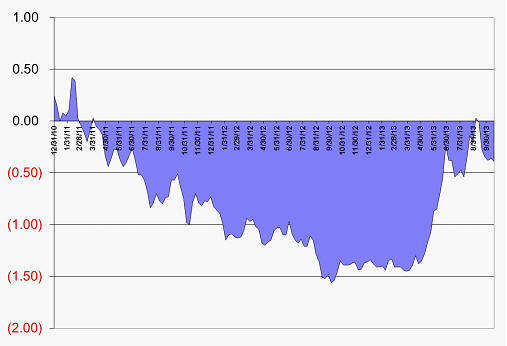

Chart 4

5-year Constant Maturity TIPS yields: 2011-2013

The yield on five year TIPS ended the 2013 third quarter at -0.35%, unchanged from the end of the second quarter and 102 basis points higher than the -1.37% yield at the end of 2012. Five-year constant maturity TIPS yields bottomed at -1.62% on October 4, 2012.

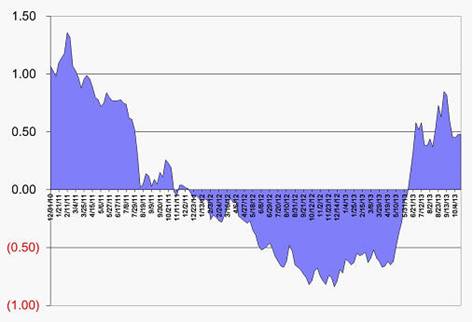

Chart 5

10-year Constant Maturity TIPS yields: 2011-2013

Source: U.S. Federal Reserve

10-year TIPS yields ended the 2013 third quarter at 0.45%, down 8 basis points from their 0.53% yield on June 28, 2013 and up 112 basis points from their -0.67% yield at December 31, 2012. The low water mark for 10-year TIPS yields on a weekly basis was -0.84 on December 7, 2012.

Table 1

Yield and Performance on TIPS vs. Comparable Maturity Treasurys: 2013 First Quarter

|

TIPS |

Comparable Treasury |

Breakeven |

Return |

Return |

|

|

Averages |

Yield |

Yield |

Spread |

on TIPS |

on Treas. |

|

2010-2015 maturities |

-2.45% |

0.16% |

2.60% |

0.2% |

0.1% |

|

2016-2021 maturities |

-1.48% |

0.96% |

2.45% |

0.3% |

0.4% |

|

2025-2040 maturities |

0.08% |

2.59% |

2.51% |

-2.0% |

-1.1% |

|

Totals |

-1.34% |

1.16% |

2.50% |

-0.3% |

0.0% |

Source: Lark Research estimates calculated from pricing data obtained from the Wall St. Journal. Returns on TIPS and comparable maturity Treasurys were calculated from Dec. 28, 2012 to Mar. 28, 2013.

Total TIPS returns were slightly negative at -0.3% on average in the 2013 first quarter, as small gains in the short- and intermediate maturities were offset by losses in the longer maturities. Comparable maturity straight Treasury securities produced breakeven returns. TIPS yields ended the first quarter at -1.34% on average, compared with -0.94% at the end of 2012, but the average is somewhat misleading because most of the decline in yields was realized on the shorter maturity TIPS. By comparison, yields on comparable maturity straight Treasurys were 1.16%, up from 1.13%.

Table 2

Yield and Performance on TIPS vs. Comparable Maturity Treasurys: 2013 Second Quarter

|

TIPS |

Comparable Treasury |

Breakeven |

Return |

Return |

|

|

Averages |

Yield |

Yield |

Spread |

on TIPS |

on Treas. |

|

2010-2015 maturities |

-0.73% |

0.22% |

0.96% |

-0.8% |

0.0% |

|

2016-2021 maturities |

-0.27% |

1.47% |

1.74% |

-6.6% |

-3.1% |

|

2025-2040 maturities |

0.94% |

3.09% |

2.15% |

-13.6% |

-6.0% |

|

Totals |

-0.07% |

1.61% |

1.68% |

-6.6% |

-3.0% |

Source: Lark Research estimates calculated from pricing data obtained from the Wall St. Journal. Returns on TIPS and comparable maturity Treasurys were calculated from Mar. 28, 2013 to Jun. 28, 2013.

In the second quarter, TIPS suffered an average loss of 6.6%, with the losses concentrated in the intermediate and long maturities. Straight Treasurys fell 3.0% on average, with losses also in the intermediate and long maturities. Breakeven spreads declined from 250 basis points on average in the first quarter to 168 basis points, as the losses on TIPS exceeded the losses on straight Treasurys. The decline in breakeven spreads was greatest in the shorter maturities, due primarily to a decline in inflation expectations.

Table 3

Yield and Performance on TIPS vs. Comparable Maturity Treasurys: 2013 Third Quarter

|

TIPS |

Comparable Treasury |

Breakeven |

Return |

Return |

|

|

Averages |

Yield |

Yield |

Spread |

on TIPS |

on Treas. |

|

2010-2015 maturities |

-0.62% |

0.19% |

0.81% |

0.0% |

0.2% |

|

2016-2021 maturities |

-0.39% |

1.48% |

1.87% |

1.5% |

0.6% |

|

2025-2040 maturities |

0.97% |

3.24% |

2.27% |

0.9% |

-1.0% |

|

Totals |

-0.10% |

1.65% |

1.75% |

1.0% |

0.2% |

Source: Lark Research estimates calculated from pricing data obtained from the Wall St. Journal. Returns on TIPS and comparable maturity Treasurys were calculated from Jun. 28, 2013 to Sep. 30, 2013.

In the 2013 third quarter, TIPS produced an average gain of 1.0%. Principal losses were slight in both the short and long maturities, but positive inflation adjustments mostly offset those losses. In the intermediate maturities, rising prices and a positive inflation adjustment produced modest gains. Short-term TIPS broke even for the quarter, but intermediate-term TIPS earned a total return of 1.5% and longer-term TIPS 0.9%. Straight Treasurys earned a total return of 0.2%, with losses in the long maturities. Breakeven spreads increased slightly from 168 basis points in the second quarter to 175 basis points, due to the increased yield on straight Treasury securities.

Table 4

Performance of TIPS Mutual Funds as of September 30, 2013

|

Performance |

Annual |

||||||||

|

NAV |

Assets |

One |

Three |

Five |

Expenses |

||||

|

Fund Name |

Ticker |

30-Sep-13 |

($B) |

13Q3 |

YTD |

Year |

Year |

Year |

as % |

|

Am. Cent. Inv. Infl. Adj. Bond |

ACITX |

12.19 |

3.8 |

0.74% |

-7.18% |

-6.68% |

3.44% |

5.00% |

0.47 |

|

Am. Cent. Inv. Infl. Prot. Bond |

APOIX |

10.32 |

0.9 |

0.68% |

-2.12% |

-1.29% |

2.95% |

4.74% |

0.55 |

|

BlackRock Infl. Prot. Bond A |

BPRAX |

11.07 |

3.5 |

0.74% |

-6.42% |

-5.02% |

3.28% |

5.14% |

0.76 |

|

Dimensional Infl. Prot. Sec. |

DIPSX |

11.78 |

2.6 |

1.28% |

-6.99% |

-5.71% |

4.27% |

5.69% |

0.13 |

|

Dreyfus Infl. Adj. Sec. |

DIAVX |

12.77 |

0.3 |

0.56% |

-7.04% |

-5.87% |

3.20% |

4.76% |

0.70 |

|

Fidelity Infl. Prot. Bond |

FINPX |

12.42 |

2.7 |

0.68% |

-6.99% |

-6.05% |

3.57% |

4.81% |

0.45 |

|

T. Rowe Price Inf. Prot. Bond |

PRIPX |

12.54 |

0.4 |

0.74% |

-6.71% |

-5.81% |

3.32% |

4.86% |

0.50 |

|

Schwab Infl. Prot. Sel. |

SWRSX |

11.17 |

0.3 |

0.66% |

-6.91% |

-5.64% |

3.49% |

4.69% |

0.29 |

|

Vanguard Inf. Prot. Bond |

VIPSX |

13.36 |

29.3 |

0.84% |

-6.88% |

-5.91% |

3.78% |

4.95% |

0.20 |

|

Averages |

0.77% |

-6.36% |

-5.33% |

3.48% |

4.96% |

0.45 |

|||

Sources: FINRA

The performance of TIPS mutual funds was roughly consistent with our calculated returns on individual securities. The average TIPS mutual fund in this sample gained 0.77% in the 2013 third quarter, compared with the average gain of 0.97% calculated for all TIPS securities. Any differences in performance among TIPS mutual funds probably relate to differences in average duration, fees and other items.

October 24, 2013

Stephen P. Percoco

© Lark Research, Inc.