Markets Vacillate Between Stronger Economy and Fed Accommodation

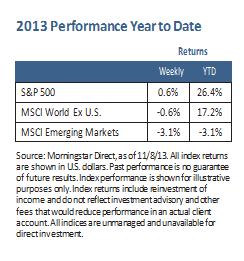

U.S. equities finished mostly higher last week as the S&P 500 increased 0.6%, ending higher for the fifth straight week.1 The return of central bank action was a primary concern. The European Central Bank (ECB) surprised investors with a 0.25% rate cut,2 while the debate over the Federal Reserve’s impending tapering decision continued in earnest.

Equities Continue to Enjoy Reflationary Tailwinds

The October employment report was stronger than expected — payroll job growth substantially exceeded estimates and positive revisions were made to prior periods. The average job growth over the last three months has been more than 200,000 (after revisions), which is above the average during the recovery.3 The unemployment rate rose to 7.3%,3 yet the drop in the labor force was abnormally large. The labor force participation rate reached the lowest level since March 1978.3 The employ- ment report provides ammunition for proponents of scaling back quantitative easing sooner. The odds have increased that tapering could begin in December or January, but next month’s employment report will help inform the Fed’s decision.

A good economy is generally positive for corporate earnings, so strong economic reports should be optimistic for equities. But currently investors appear to welcome a weak economy since it ensures the implicit guarantee of Fed easing, which has historically supported equities. This is a conundrum — the challenge of weak and strong data versus easy and neutral monetary policy — and it is likely to keep equities in a volatile range.

Recent new record highs for U.S. equities (S&P 500) have been accompanied by the weakest buying pressure in more than a year. This lack of buying pressure is similar to May 2011 and September 2012, and suggests the rally could give way to market consolidation.

Weekly Top Themes

1. The ECB rate decrease of 0.25% was unexpected.2 The ECB estimates that rates will remain at current or lower levels for an extended period.

2. Real GDP increased 2.8% for the third quarter, stronger than expected.4 The main surprise was related to inventories while other parts of the report were similar to expectations.

3. Prior to recessions, inflation accelerates. Today, both the Consumer Price Index (CPI) and Producer Price Index (PPI) are low and declining. Slowing inflation tends to help boost economic growth.

4. Corporate leverage remains historically low. We believe the combination of low borrowing costs, strong balance sheets and potentially declining ROE will motivate companies to increase leverage further in the coming quarters.

5. Headwinds to GDP from fiscal policy, known as fiscal drag, is projected to decline. Fiscal drag will decline from 1.2% in 2013 to 0.6% in 2014 to almost neutral in 2015, under current law.5

The Big Picture

Although we disagree that the stock market is forming a bubble, we have concerns about the internal strength of the current advance. So far, promises of abundant liquidity are trumping soft earnings and irregular forward guidance. It is likely that monetary conditions will stay stimulative until long after labor market slack has been eliminated. The stock market surge since the end of the government shutdown has been broad-based. Also, correlations among stocks continue to fall, signaling discretionary buying behavior rather than momentum chasing. Cash on the sidelines remains a powerful source of market support.

We believe the path of least resistance for equities is still upward, even though near-term conditions appear overbought. The major economic and financial mar- ket risks from recent years seem to have receded. Economic prospects are slowly improving, but not so quickly that it threatens the unprecedented global monetary experiment. Investors should begin to gravitate toward equities after avoiding them over the last five years. At some point, we believe sentiment, positioning, valuation and the policy backdrop will signal higher risks for equities, but these gauges are not near those levels today.

1 Source: Morningstar Direct, as of 11/8/13. 2 Source: European Central Bank, “Key ECB Interest Rates,” November 7, 2014. 3 Source: Bureau of Labor Statistics, “The Employment Situation – October 2013,” November 8, 2013, http://www.bls.gov/news.release/empsit.nr0.htm. 4 Source: U.S. Department of Commerce Bureau of Economic Analysis, “National Income and Product Accounts Gross Do- mestic Product, 3rd quarter 2013 (advance estimate),” November 7, 2013, http://www.bea.gov/newsreleases/national/gdp/gdpnewsrelease.htm. 5 Source: Strategas Research Partners, “Just How Large Will the Fiscal Drag Be in Calendar Year 2014?,” November 5, 2013; Source: Congressional Budget Office, “The Budget and Economic Outlook: Fiscal Years 2013 to 2023,” February 2013, www.cbo.gov.

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float- adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Non- investment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

GPE-BDCOMM2-1113P

© Nuveen Asset Management