Macro Themes: 2H13

U.S.

- The Fed will be late in removing monetary accommodation as the economy strengthens.

- Consumers will be strong contributors to economic growth.

- Political uncertainty, and its impact on markets and the economy, is declining.

GLOBAL

- As austerity wanes, Europe is poised for growth.

- A resurgent Japan will have a positive impact on global markets.

- Improving global growth and continued ample liquidity should help emerging market assets stabilize.

OUTLOOK

- Highly accommodative monetary policy has depressed real sovereign yields and distorted valuations across fixed income. As such, security selection is vital.

- Market returns will depend on the developed world’s ability to maintain economic momentum despite softness in many emerging market economies.

Willing a Fiscal Win

Why can’t we just will our desired political outcomes the way the most fervent seemingly can impact ballgames? After watching Fenway Park packed to the rafters with Red Sox faithful exercising their sovereign and ethereal right to psychically encourage baseballs out of the yard — and knowing that millions of others in Red Sox nation were doing the same in front of their televisions — we’re left wondering if the fans of Team U.S.A. can apply a little of that classic Carlton Fisk mojo a few hundred miles down I-95.

In your (field of) dreams! Because hooting and hollering for grand political bargains is a superstitious exercise in futility when the will of the people — as represented by their elected leadership — becomes acutely polarized. Besides, the October standoff in Washington wasn’t exactly a Fall Classic; it was more like a slopfest between a pair of bottom-dwellers, chock full of booted grounders and misjudged flies until the winning run was ingloriously balked in after nine tortuous innings. But if we the fans take the brown bags off our heads and consider the upside in 2014, we may start to believe that even our bush-league political strategy — i.e., doing just enough to avoid a complete meltdown — may be enough to seal the win for Team U.S.A. without necessarily having to resort to the heroics of jacking one over the fiscal Green Monster.

That’s a tough sell for policymakers to make and for the market to judge, of course, considering the economic and psychological spillover effect the October government shutdown and other political impasses of recent vintage have had on the private sector’s ability to trust its public leadership. The lack of political will to really tackle our fiscal issues has had a direct impact on the real economy — U.S. growth has been repeatedly beaned by political dysfunction since 2010, and there’s also the less-tangible confidence blow delivered to consumers, investors and businesses. Even prior to the latest debacle, a number of indicators suggested that fiscal issues continue to make consumers uneasy and businesses reluctant to spend. Moreover, concern persists about the hit the U.S. credit ranking could take should a rating agency sour on our potential — as Standard & Poor’s did in 2011 when we almost whiffed on the decision to raise the debt ceiling. October’s budget and debt-ceiling fiasco not only furloughed workers and undermined confidence, it also forced the Fed to further extend its already-unprecedented monetary stimulus campaign. The reduction in central bank asset purchases — widely anticipated to begin in September — was delayed, with the FOMC citing significant risks to the fiscal outlook as one reason to hold off.

However, despite a track record marred by blunders and brinksmanship our lawmakers have by and large managed to keep policy on a reasonable trajectory. The United States moved faster and more dramatically toward stimulus during the global financial crisis than the other large economies of the world and achieved a more rapid recovery as a result. The consequence of this stimulus was an unsustainable deficit, which the government has been wise to pare back while the Fed’s record accommodation held open a window of opportunity. Now, as the labor market improves and the Fed prepares to step back from the plate, policy makers can afford to narrow that deficit more slowly and avoid stressing what is still a somewhat fragile recovery.

Indeed, while grand bargains in Washington likely will remain elusive, there’s a good shot fiscal drag will diminish in 2014, which is one of the reasons we expect GDP growth next year to run faster than the long-term trend. Incremental spending cuts will be less impactful, tax rates will not go up as they did in 2013, and the need for additional cutbacks will be reduced thanks to recovering state and local government revenues. Even the negative impact of October’s shutdown on fourth quarter GDP has a silver lining, as it will make it easier for the economy to post solid quarter-over-quarter growth in early 2014. Regardless of what happens in Washington — whether the sequester stays in place or a budget deal with back-loaded spending cuts as well as some tax reforms can actually be reached — this improvement is an encouraging sign for the real economy considering that employment gains in 2013 have been relatively robust, at 180,000 jobs per month, despite a fiscal drag on GDP growth amounting to nearly 2.5% annualized.

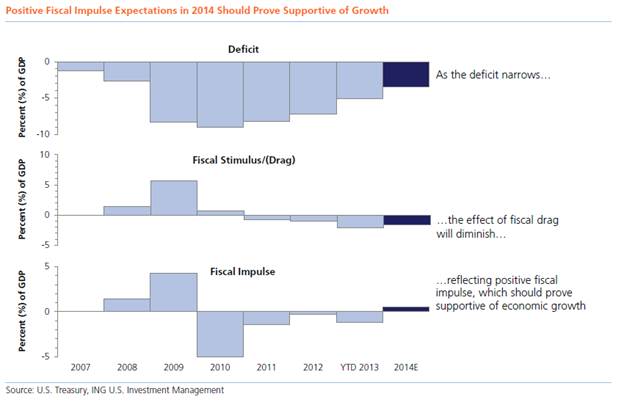

Recent deficit trends and our expectations for this year and next are illustrated in the figure below. The federal government can engage in “fiscal stimulus” by growing the federal deficit or create a “fiscal drag” by shrinking it; “fiscal impulse” reflects the year-over-year change in this measure, with a positive impulse indicating a stimulative bias. While we still expect some fiscal drag in 2014, it should shrink relative to 2013 — the first positive fiscal impulse since 2009 — and could contribute to accelerating GDP growth.

Of course, the agreement laid down by lawmakers in October only funds the government through January 15, 2014, and we know the Treasury will once again bump up against the debt ceiling less than a month after that. This means the potential for more growth-eroding outcomes in Washington — the October government shutdown hacked about 0.3% off fourth quarter GDP — remains intact. If the next self-imposed crisis coincides with another hit to the consumer, via higher gas prices, for example, or a stock market swoon, the damage could be even greater.

As we pass the five-year anniversary of the Federal Reserve’s zero interest rate policy, the real risk is that stubborn lawmakers force the Fed to bite off more than it can chew. Fed Chair Bernanke himself has reminded Congress repeatedly that the negative economic impact of a true fiscal blunder could easily be greater than the Fed’s ability to counter it through stimulus. If higher asset prices and lower volatility can be viewed as the upside of QE, it’s tough not to wonder about the downside of retaining QE even as the unemployment rate reaches levels hawkish spectators consider consistent with the Fed’s criteria of sustained improvement in the labor market. What are the unintended consequences of the Fed continuing to juice the economy, especially when citing ongoing political uncertainty in Washington as key reason?

While tapering does not mean the end of monetary accommo-dation, of course, it could be painful for the real economy if the Fed stays in the game, for example, for too long and for the wrong reasons. The Fed continuing to buy such a high share of mortgage-backed securities and Treasuries can distort valuations and create frothiness in asset prices or even consumer price inflation in coming years. That could cut especially hard the other way if the market perceives a continued postponement of tapering as evidence of an FOMC held captive by fiscal policy; the Fed’s credibility could be undermined, and with it the ability to aggressively fight unemployment as well as control inflation.

But it would appear that the will for additional dysfunctional standoffs in Washington has diminished, as the Republicans have already signaled that taking the country once again to the brink of default is not their preferred strategy going forward. Furthermore, the need for further budget cuts has eased. After the sequester and the winding down of stimulus post-2008, the fiscal deficit is more manageable and spending cuts should be much less of a concern, especially as the impulse for austerity wanes globally. More cravenly, politicians are unlikely to risk being blamed for a destructive impasse mere months before Congressional midterm elections.

This represents a potential turning point. Like an ace pitcher working around miscues in the field, U.S. private sector growth backed by monetary accommodation has managed to work deep into the game relatively unscathed despite fiscal policy missteps. With Fed bond buying approaching its final innings, however, we find ourselves with less room for error.

As the Fed begins to wean the economy off of the QE payroll, we believe it has fostered enough talent in a resurgent housing sector and recovering labor market to put the economy in a position to win. While another political blunder could cost us the game, we look to Congress to record the last few outs and close out the win for Team U.S.A. as we enter 2014. We believe they will do just that, as enough political will exists to avoid a late-innings collapse. In light of this scouting report, we continue to favor home-team U.S. credit-backed assets, including high yield and commercial mortgage backed securities.

This commentary has been prepared by ING Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults (5) changes in laws and regulations and (6) changes in the policies of governments and/or regulatory authorities.

The opinions, views and information expressed in this commentary regarding holdings are subject to change without notice. The information provided regarding holdings is not a recommendation to buy or sell any security. Fund holdings are fluid and are subject to daily change based on market conditions and other factors. Past performance is no guarantee of future results.

© 2013 ING Investments Distributor, LLC • 230 Park Avenue, New York, NY 10169