Our recent client conference saw the unveiling of our new forecast methodology for the U.S. stock market, a methodology that we are extending to all of the other equity asset classes that we forecast. It is the result of a three-year research collaboration by our asset allocation and global equity teams, and involved work by a large number of people, although Martin Tarlie of our global equity team did a disproportionate amount of the heavy lifting. In a number of ways it is a “clean sheet of paper” look at forecasting equities, and we have broadened our valuation approach from looking at valuations through the lens of sales to incorporating several other methods. It results in about a 0.7%/year increase in our forecast for the S&P 500 relative to the old model. On the old model, fair value for the S&P 500 was about 1020 and the expected return for the next seven years was -2.0% after inflation. On the new model, fair value for the S&P 500 is about 1100 and the expected return is -1.3% per year for the next seven years after inflation. For those interested in the broader U.S. stock market, our forecast for the Wilshire 5000 is a bit worse, at -2.0%, due to the fact that small cap valuations are even more elevated than those for large caps.

So much for 36 months of work. One could say that we didn’t know that we would wind up with the same basic forecast we started with, and that is true, but on the other hand we didn’t have any particularly large concerns that our forecast was giving us the wrong answer in the first place. This makes the S&P 500 forecast significantly different from the emerging equity forecast, where, as we have been telling our clients for a while, we believed that our forecasting methodology overstated the attractiveness of the group. Our revised emerging forecast is noticeably lower than that generated by the old model, and clients are welcome to contact their relationship manager for more information about this change if they would like.

What was the point of doing all of this work on the S&P 500 forecast if we were pretty confident that the old model was doing its job well? There were several reasons. First, we are always trying to improve our forecast methods, and this was merely a larger project than a number of others we’ve tackled over the past 20 years in this area. Second, we want our process to adhere as closely as possible to our basic beliefs that stocks should sell at replacement cost and that the return on capital and cost of capital need to be in equilibrium in the long run. And third, we want a process that makes it as straightforward as possible to slice the equity markets in a different way and still be confident in the resulting forecast. On both the second and third points, we believe the new methodology is superior to the old.

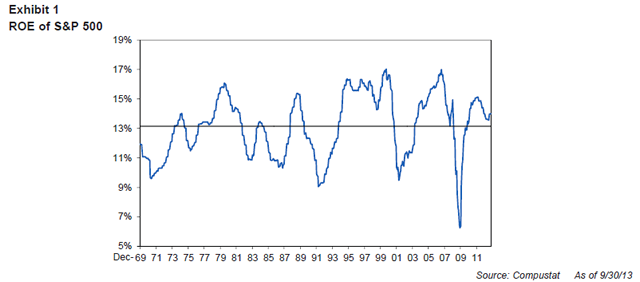

The primary issue with turning our beliefs into forecasts is that the key input to valuing the market is an unobservable item: economic capital. Economic capital – aka replacement cost – is central because it is the “thing” that generates earnings. Book value of common equity is the accounting figure that is supposed to approximate this term, but it is subject to multiple distortions that make it a clearly inadequate proxy for true equity capital. One way of seeing this is to simply look at ROE – that is, return on book value of equity – over time. In the U.S., the average ROE for the S&P 500 has been 13% since 1970, as we can see in Exhibit 1.

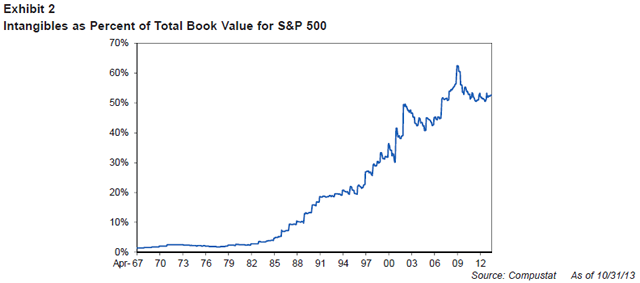

If the true return on equity capital had been 13% and other things remained equal, real book per share growth should have been more than 7% above inflation over the last 43 years, and total returns should have been over 11% real. In reality, returns have been about 5.7% real and real book growth has been approximately 2% per year. So, the true return on equity capital must have been significantly lower than the 13% ROE.1 And investors have certainly acted as if they believed true economic capital has been greater than book value, as the S&P 500 has traded at approximately twice book over the past 43 years. If we declared that economic capital is twice book value, the math works out much better. With that assumption, “true” ROE has been 6.5%, against a real return of 5.7% for the S&P 500 since 1970, which is certainly in the ballpark, if not quite spot on. You could simply stop there and declare that the S&P 500, which is currently trading at about 2.5 times book value, must therefore be overvalued by 25%. The problem is, even if book value has been half of economic capital on average over the last 40 years, how do we know it is still half of economic capital today? Exhibit 2 shows one way that book value has changed over time in the U.S. – the increasing percentage of total book, which consists of intangible assets such as goodwill. This has risen from less than 10% of total book in the 1970s to over 50% today. The change has been driven by accounting changes and merger and buyback activity. It doesn’t mean that today’s book values are less “correct” than those of 40 years ago. It may well be that today’s numbers are much closer to economic capital than historical numbers, and we can certainly hope that changing accounting standards push us in the right direction over time. But insofar as they push us in any direction – right or wrong – they make it more difficult to compare today’s ROE and price to book ratios with historical figures.

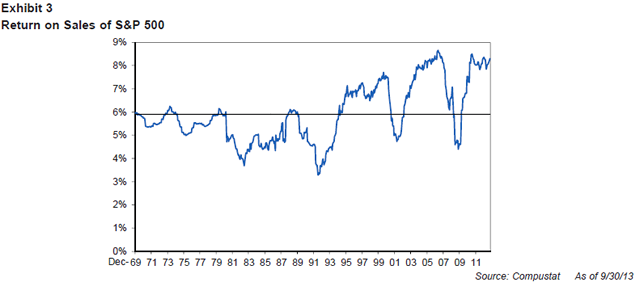

One way to get around the problem of accounting changes on book value is to look instead at return on sales. Sales have the nice feature that accounting changes have relatively little impact on them. Sales figures from 1970 were calculated on basically the same basis as sales figures today, and probably the same as they will be in 2050. Return on sales has looked fairly stable historically, and as you can see in Exhibit 3, we are significantly further above normal profit margin on sales than we are above normal ROEs.

Combining the current P/E of over 19 for the S&P 500 and a return on sales about 42% over the historical average, we would get an estimate that the S&P 500 is approximately 75% overvalued. But the assumption of stable return on sales is problematic for a different reason than ROE. Book value is at least an accounting estimate of equity capital, and as imperfect as it is, return on equity capital is what is supposed to mean revert in a capitalistic system. There is not such a strong argument for reversion when it comes to return on sales. Historically it has been mean reverting, but a high return on sales for a given company does not necessarily mean that competition will follow. Intel has a high return on sales on its microprocessors, but being in a position to sell those microprocessors requires huge amounts of investment and intellectual capital. An economy driven by Intels could easily support higher profit margins than one of supermarkets.2 So there is a chance that this return on sales framework overstates the degree of overvaluation in the U.S.

Our old methodology for equity forecasting made adjustments for this, and we assumed that profit margin on sales would revert to something higher than its long-term average. This helps explain why there hasn’t been much change to our actual forecast for the U.S., but it required a fair bit of manual adjustment to come up with our equilibrium number and the adjustments were harder to estimate properly for groups of stocks where we have less good historical data than we have for the S&P 500. This has made it difficult to readily generate a forecast for sets of stocks that we want to build a forecast for that we hadn’t previously researched as a coherent group, such as eurozone stocks or emerging market stocks ex-resource companies, which we have had reason to look at recently.

In our new forecasting apparatus, looking at such groups becomes significantly easier. Because we have multiple ways to calculate proxies for true economic capital, there is less pressure on ensuring that any single measure has characteristics that are stable over time. We still have to look out for situations in which the distortions all wind up pushing in the same direction, but for a quick first pass on a group to see whether more detailed work is warranted, the new methodology makes it easier to get a reasonable number on the first try.

As were built our models, we took the opportunity to take a fresh look at our other assumptions, including the expected period of reversion to equilibrium valuation and profitability, and our assumptions about the “slippage” between accounting earnings and true economic profit. We have concluded that a seven-year period of reversion for valuation still looks to be about right. There is plenty of variation in the time it takes equity valuations to revert – a seven-year average period doesn’t mean a market can’t spend 15 or 20 years being overvalued or undervalued. But in a given year, the historical evidence says it is fair to expect that a stock market will move one-seventh of the way back to fair value.

One assumption we have tweaked a bit is the “slippage” factor in equity earnings that we have been building in for over a decade. The idea behind slippage is that there seems to be a gap between the average earnings yield of the market and the average real return. As an example, since 1970 the average earnings yield for the S&P 500 has been 6.7%, while the compound return has been 5.7%. The most straightforward way to think about this is that accounting earnings are not an exact representation of true economic profits and the gap between the stated earnings yield and the actual return, adjusted for valuation shifts, is an indication of the average difference between the (unobserved) true economic profit and accounting earnings. We are reducing our estimate of this slippage from 15% of earnings to 9%, which increases equilibrium P/E from 15 to 16.3 This change is actually responsible for almost all of the change to the forecast, as our estimate of return on capital is very similar to our estimate based on sales.

But enough about the details. The basic point for us remains the same – the U.S. stock market is trading at levels that do not seem capable of supporting the type of returns that investors have gotten used to receiving from equities. Our additional work does nothing but confirm our prior beliefs about the current attractiveness – or rather lack of attractiveness – of the U.S. stock market. To answer the question we get most often about our forecast – “How could you be wrong?” – there are a couple of ways we could be wrong. One of them is pleasant and implausible, the other is more plausible, but far less pleasant.

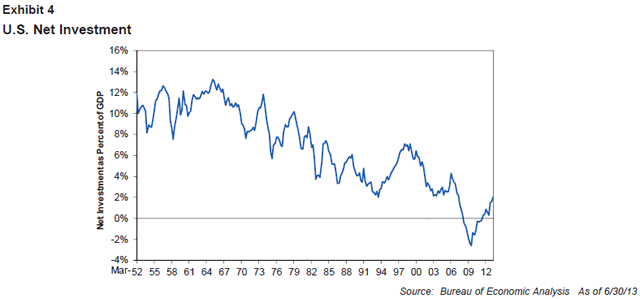

The pleasant way we could be wrong is if the U.S. is about to embark on a golden age of corporate investment and economic growth that will gradually compete down the current return on capital such that overall profits manage to grow decently as the P/E of the stock market wafts slowly down. This would solve lots of problems, including the federal deficit and unemployment and, quite possibly, health care costs as well, but there is sadly no evidence whatsoever that it is occurring, as can be seen in Exhibit 4.

The investment boom to drive such strong growth would almost certainly have to be at least as large as what we saw in the 1950s and 1960s, but as you can see, not only is corporate investment down significantly in the post-GFC years, it had been on a downward trend for 40 years prior to that. That doesn’t mean it absolutely cannot change, but investing on the basis that it will occur makes only slightly more sense than basing your retirement plans on winning the lottery.4

The less pleasant way we could be wrong is if 5.7% real is no longer a reasonable guess at an equilibrium return for U.S. equities. If equity returns for the next hundred years were only going to be 3.5% real or so, today’s prices are about right. We would be wrong about how overvalued the U.S. stock market is, but every pension fund, foundation, and endowment – not to mention every individual saving for retirement – would be in dire straits, as every investors’ portfolio return assumptions build in far more return. Over the standard course of a 40-year working life, a savings rate that is currently assumed to lead to an accumulation of 10 times final salary would wind up 40% short of that goal if today’s valuations are the new equilibrium. Every endowment and foundation will find itself wasting away instead of maintaining itself for future generations. And the plight of public pension funds is probably not even worth calculating, as we would simply find ourselves in a world where retirement as we now know it is fundamentally unaffordable, however we pretend we may have funded it so far. William Bernstein wrote a piece in the September issue of the Financial Analysts Journal, entitled “The Paradox of Wealth,” which explains far too plausibly why generally increasing levels of wealth might drive down the return on capital across the global economy. It’s well worth a read, although perhaps not on a full stomach, as it is one of the most quietly depressing pieces I have ever come across (and this is coming from someone who has spent the last 21 years reading Jeremy Grantham’s letters!).

Bernstein’s is definitely an intriguing idea, and we will have to look seriously at it in the years ahead, but for now we have not changed our estimate of equilibrium returns to equities or other assets. We still believe that 5.7% real is a decent estimate of long-term equity returns and today’s valuations for the U.S. stock market are a temporary issue that will be resolved either through a relatively quick bear market or a longer period of more or less flat returns – as the last 13 years, for all of their periodic excitement, have turned out to be.

And even if we are underestimating the potential for the U.S. stock market to deliver returns from here, it’s still not obvious to us that our portfolios are that far off from optimal. After all, any plausible argument that can make U.S. equities attractive, given that they are trading at above historic average P/Es with profit margins close to all- time highs, should make non-U.S. equities, generally trading at lower P/Es with margins much closer to historical averages, a screaming buy. It is not as if the U.S. is a uniquely well-governed country or U.S. companies are run in a way that cannot be emulated elsewhere around the world. To be clear, we don’t consider non-U.S. equity markets a screaming buy. But as value managers listening for any assets, anywhere, that are screaming to be bought, the world currently sounds a deathly quiet place. The hoarse whisper of “buy me” coming from European and emerging equities (as well as the polite cough for attention coming from U.S. high quality stocks) comes through loud and clear. For the purpose of doing the right thing by our clients, our major worry today is about whether our straining ears are hearing the whispers of the least overvalued equities as louder than they really are and that we consequently own more of them than is warranted. The “risk” that the U.S. stock market is significantly more attractive than we estimate it to be strikes us, by contrast, as a low probability, as well as one that is exceedingly unlikely to hurt our clients’ portfolios.

1At first blush it seems that you could make an argument that ROE is really 13% but corporations do something systematically stupid with retained earnings that causes the low level of growth we have observed. The trouble is that book value is a direct consequence of retained earnings, so it becomes logically inconsistent to believe that actual returns are 13% and that corporate investment behavior is fundamentally flawed.

2This is even true under the macro-economic profit framework of the Kalecki equation that my colleague James Montier has written about at some length. Macro-economically speaking, corporate investment is a positive source of profits, so a high investment/high profit margin economy can persist without requiring any macro-economic instability. In the real world, however, investment rates have fallen in the U.S. and across the developed world over the past couple of decades, so it is almost inconceivable that we have achieved a stable new “Intel equilibrium.”

3The technical reason for this change is that in the presence of volatility in equity valuations, an average earnings yield is slightly higher than the expected return to equities even if there is no slippage. A better measure to use is the square root of the ratio of the average earnings yield to average P/E, and this figure is slightly lower than the average earnings yield. This is apparently a very elegant result to those with advanced degrees in math or physics, so feel free to corner your local mathematician for an explanation of why this is so and why it is cool.

4 There is a strange feature of the relationship between investment rates and profits. In the short term, as long as the profits are spent in some fashion or other, lower investment is probably good for margins, as it means less competition. In the long run, low investment makes it extremely difficult to grow earnings much, except in cases of a market trading at low P/Es where the money is used to buy back stock, which can increase earnings per share even though aggregate earnings wouldn’t grow much. Today’s buybacks, however, are not a particularly good buy, as the high P/E of the market means the return on capital of that “investment” is fairly low and therefore cannot lead to a lot of earnings growth.

Mr.Inker is the co-head of asset allocation.

Disclaimer: The views expressed herein are those of Ben Inker as of November 18, 2013 and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such.

© GMO

© GMO