Part 1. The Nobel Prize

Economics is a very soft science but it has delusions of hardness or what has been called physics envy. One of my few economic heroes, Kenneth Boulding, said that while mathematics had indeed introduced rigor into economics, it unfortunately also brought mortis. Later in his career he felt that economics had lost sight of its job to be useful to society, having lost its way in a maze of econometric formulas, which placed elegance over accuracy.

At the top of the list of economic theories based on clearly false assumptions is that of Rational Expectations, in which humans are assumed to be machines programmed with rational responses. Although we all know – even economists – that this assumption does not fit the real world, it does allow for relatively simple conclusions, whereas the assumption of complicated, inconsistent, and emotional humanity does not. The folly of Rational Expectations resulted in five, six, or seven decades of economic mainstream work being largely thrown away. It did leave us, though, with perhaps the most laughable of all assumption-based theories, the Efficient Market Hypothesis (EMH).

We are told that investment bubbles have not occurred and, indeed, could never occur, by the iron law of the unproven assumptions used by the proponents of the EMH. Yet, in front of our eyes there have appeared in the last 25 years at least four of the great investment bubbles in all of investment history. First, there was the bubble in Japanese stocks, which peaked in 1989 at 65 times earnings (on their accounting) having never peaked at over 25 times previously, to be followed by a loss of almost 90% in the MSCI Japan index! Second, we had the Japanese land bubble peaking a little later in 1991. This was probably the biggest bubble in history and was certainly far worse than the Tulip Bubble and the South Sea Bubble. And, yes, the land under the Emperor’s Palace, valued at property prices in downtown Tokyo, really was equal to the value of the land in the state of California. Seems efficient to me … California is so big and unwieldy. Next, we had by far the largest U.S. equity bubble in 2000, which peaked at 35 times earnings compared to a peak of 21 times in 1929, yet had had previous growth rates less than half of those in 1928 and 1929. Finally, we had what I described in 2007 as the first truly global bubble. It covered all global stocks, fine arts and collectibles, and almost all of the real estate markets. The last of these was led by the U.S. housing market, which, having benefited from its great diversity, had historically been remarkably stable until Greenspan got his hands on it. Compared to previous ultra-stable data, this measured as a 3.5 sigma event, which, according to the EMH assumption of perfect randomness, should have occurred only once every 10,000 years. Yet, encouraged (brainwashed might be a more accurate description) by the EMH, Bernanke (and Yellen) could not, or would not, even recognize the risk, to our very substantial cost.

The edifice of unproven and totally inaccurate assumptions represented by the EMH was not defended as having useful output, but was defended, especially by the high priests of the theory, as being the most accurate reflection of reality that could be rolled out. Thus, 12 reasons were given as to why the 22% drop in one day (over one-third in a day and a half) in the 1987 crash was a rational economic response to a suddenly changed world. (My then partner, Dick Mayo, typically immersed in market trading 10 hours a day, was indeed braced that day for remarkable events. He, like other professionals, had paid no attention to any of these reasons, but had focused on the new, unproven so-called portfolio insurance and the moral hazard and false confidenceit brought with it – a reason, by the way, that did not appear on the list of 12!) Similarly, Japan at 65 times earnings was justifiedby accounting errors and low interest rates, and the Tech Bubble by Greenspan’s “permanently” increased productivity that appeared everywhere except in the data, which showed a subsequently reduced level of productivity. I must admit that I have never heard an EMH rationale for the Emperor’s Palace, but you get my point.

It has also been suggested that Fama’s work led to indexing. Not really. When we offered indexing at Battery march in 1971 we did so because we knew it was a zero-sum game. That for us was a complete and sufficient reason for indexing: active managers summed to market returns less large fees and commissions while indexers summed to market returns less small fees. To prove our belief, we simultaneously ran an active portfolio that ended its first eight years – a random number selected to coincide with my stay there – up 7% a year relative to the S&P. Battery march more or less shared the indexing business in its first few years with Wells Fargo, with the considerable propaganda skills of Dean Le Baron, our senior partner, more or less offsetting their huge size. They however did talk about the market’s efficiency, which, particularly back then, only existed in the minds of a few professors and apparently one or two academically inclined Wells Fargoans. To nail home this point, Jack Bogle’s Vanguard Index Fund in 1975 was, like us, also emphatically based on the concept of a zero-sum game and the certainty it offered that most players would underperform.

None of this efficient market nonsense was detrimental to us value managers so I should find time to thank all those involved for producing and passionately promoting the idea. During the 1970s and 1980s I am convinced it helped reduce the number of quantitatively-talented individuals entering the money management business. Why waste your PhD in particle physics on an efficient market? The field was left for an extra 20 years or so to very ordinary, not particularly quantitatively-minded individuals. And very nice it was too. And, by the way, the proponents of the EMH not only promoted their theory, but via the academic establishment the high priests badgered academic researchers into leaving, resigning themselves to non-tenure, or getting religion, as it were.

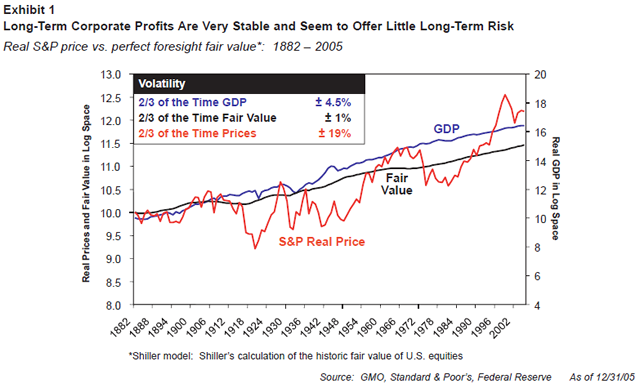

Into this morass of false assumptions there did come a ray of light back in 1981, when Robert Shiller proposed a simple test of market inefficiency. He assumed total clairvoyance and asked the question: What were markets worth back in, say, 1880, 1915, 1961, etc., if you knew both the long-term market return, or discount rate (in the 6% to 7% range after inflation), and, more importantly, you also knew the complete and accurate future stream of dividends?

Exhibit 1 shows our simplified version. Even on its own the dividend stream really is fairly smooth, but because the market is worth the sum of all future discounted dividends, it becomes remarkably smooth so two-thirds of the time the “fair value model,” as we’ll call it, is within ±1% of its long-term trend. The trend turns out to be about a rather modest 1.5% real. (The relatively stable series of GDP is put in here for reference. It is within ±4.5% two-thirds of the time.) The red series is what we emotional and career-protective investors do to this stable world. The S&P 500 is within ±19% of its trend two-thirds of the time! This almost ridiculous volatility, 19 times more than is really justified by the underlying fundamentals, is in my opinion caused mainly by individual investors driven by behavioral factors that result in herding: non-experts simply feel more comfortable in a herd and, indeed, “prudent” investing has long been legally defined as doing what others do. For professional investors it is caused by the need to report upwards to decreasing levels of market familiarity – the top decision-makers usually look and feel very much like individual investors (with some very notable exceptions) and impose their will on the institutional investors, whose number one imperative is to keep their jobs. Being wrong on your own, as Keynes describes so eloquently in Chapter 12 of TheGeneral Theory, is the cardinal crime for an investment manager. To avoid this, the professionals try very hard to ensure that if they are going to run off any cliff they will: a) have a lot of company; and b) that most of the company will be one step ahead. In short, the management of career risk results in very destructive herding. It also produces a great deal of extrapolation, also designed to protect their careers. After all, if you make a forecast, Lord knows, you can be wrong. So, instead you use extrapolation, which Keynes said is a convention we adopt even though we know from personal experience that it is not applicable in the real world. (Keynes was 47 years ahead of all other economists in understanding markets. And counting, for they are still nowhere near catching up.)

Going back to Shiller’s simple experiment: was it enough to cause a pause in the march of market efficiency? Not for a second. It was batted away like a bothersome fly for reasons that I cannot explain with a straight face.

This brings up an interesting question. What would it take to become as volatile as the market? I believe there are only two choices here, one bad and one good. The bad one is typically self-referential: that investors change the discount rate minute by minute. In this way we would have to believe that they did not panic in 1987 as portfolio investors all tried to squeeze through the small door of the burning theatre, but that they merely reassessed the distant future that morning as very much less attractive than the day before! Whatever the ridiculous move in the market, the math will “solve” with an equally ridiculous change in the assumed discount rate. The second theory, though, is compatible with everything I know about the market (or what I accepted from Keynes): that extrapolation dominates the workings of the market.

Let me briefly give you my prime evidence. I will spare you one of my favorite exhibits in the interest of saving space. What it would show is that the 30-year U.S. government bond peaked in 1982 at a 16% yield, because inflation had spiked for a second to 13% (even though Paul Volcker was already on the anti-inflation warpath). Yes, you might expect the T-Bill to be 14% or so, which it was. But a 30-year bond! To extrapolate a full 13% inflation– a complete outlier event, by its very nature bound, kill or cure, to be temporary – for a full 30 years! More recently, of course, we extrapolate currently very low inflation for 30 years. My case rests.

Well the stock market apparently does the same. If for every time profit margins spiked up or down you were to extrapolate forever those abnormal temporary levels and ignore their obviously mean-reverting nature, you would get the same volatility as the market delivers! Well, actually, a little less. What an amazing testimonial to the periodic idiocy of the market players. (An honorable reference might be made here to another of my favorite economists – Hyman Minsky – who said rather similarly that periodic financial crises were “well-nigh inevitable,” because a form of extrapolation would occur with stability generating more risk-taking and on into a spiral until something inevitably would go wrong. A useful outsider like him would, alas, never have a prayer of winning a Nobel Prize.)

So, economics has been more or less threadbare for 50 years. Pity then the plight of the Bank of Sweden with all that money to give away in honor of Alfred Nobel and in envy, perhaps, of the harder sciences. If you had $1.2 million to give away but few worthy recipients, what would you do? I would suggest making it a once-every-three-year event, although that would make $3.6 million per winner, which would seem a little unfair to the almost infinitely more serious scientists. Still, I would adopt the three-year routine. Then the handful of Modiglianis – the real McCoys as it were – would not have had to share the glory or the money with so many ordinary soldiers. But what does the Bank do this year? It gives the prize to three economists as if there were far too many worthy recipients for a puny one-prize-a-year to satisfy. And to further prove how completely they have lost the plot, they gave two-thirds of the prize to two economists who attempted to prove market inefficiency and one-third to another who claimed it was efficient and seriously efficient at that. What a farce. And to read all these genteel descriptions, or rather rationalizations, as to why this made sense is to realize to what extent the establishment is respected, regardless of its competence level.

Robert Shiller at least served society – Kenneth Boulding would have approved – by loudly warning us of impending doom from the Tech Bubble with his superbly timed book Irrational Exuberance in the spring of 2000. Not bad! He also warned us well in advance of the much more dangerous housing bubble; in a more rational world, Greenspan, Bernanke, Yellen, and a few bankers might have taken his warning to heart. In a parallel universe those practical services alone might be worth a Nobel Prize. As for Fama, who conversely provided a rationale for all of us to walk off the cliff with confidence, the less said the better. For believers in market efficiency and all the assumptions that go along with it, the real world really is merely an annoying special case.

Part 2. Yellen and the Prospect of the Same Ole, Same Ole at the Fed.

The case against Summers was made often and eloquently. The most cutting negative for me was his famous suppression – with his allies Rubin, Greenspan, and, surprisingly, Levitt – of the sensible and determined stand by Brooksley Born to do her job and regulate obviously out-of-control financial instruments. In order to facilitate the giantification of banks, pointedly Citicorp, he and Rubin also cheerfully helped dispatch Glass-Steagall, presumably so that Rubin, when he more or less immediately became Citi’s Chairman, could have an even larger bank to run off the cliff at tax payers’ expense. Yellen, on the other hand, has sat in positions of some authority near Fed bosses Greenspan and Bernanke as their desperate experiments in overstimulation, amelioration of ensuing collapses, and moral hazard intensified to a level where apparently almost everyone in finance had their prudence overwhelmed by short-term greed. Some of Yellen’s supporters, rather desperately I think, claim that she warned of an impending housing bust, yet she has quotes out there, so like Bernanke’s that I forget which quote is which, to the effect that housing merely reflected a strong economy. She also sounded like early Greenspan in suggesting that bubbles don’t exist, and even if they did, it would not be the Fed’s business to intervene, and even if it were, there would be nothing they could do, and even if there were, the guaranteed pain of intervention would not be worth the possible benefits. (The Canadian running the Bank of England, Mr. Carney, claims to know better: that housing bubbles do indeed exist and are worth keeping an eye on. He’ll need some luck with the level of U.K. housing prices today – even as the

U.K. government encourages more leveraged mortgages. Do they never learn? Guaranteeing new mortgages over 5% will serve to further push the prices up so that for any new buyers, houses will be affordable only at low mortgage rates. But England has floating mortgage rates for heaven’s sake! And one day, dear home buyer, mortgage rates will become more normal, possibly even nasty – it has happened – and you will simply not be able to afford the payments. What a bad idea this is.)

But back to Yellen, who has happily gone along with the failed Fed policy of hoping madly for a different outcome despite repeating exactly the same thing. The past consequences of this strategy have been so dire on two occasions and threaten to be just as bad again sometime within two or three years that, yes, given a choice I would have picked Summers over Yellen just for the small possibility that being super confident, to be polite, he just might have done something different. Yes, I agree, desperate logic for desperate times.

In short, my feeling was and is “none of the above!” In a “shades of Volcker” approach, I would put a requirement for backbonefirstalongwiththeabilitytothinkforyourselfandstandfirm.We have little to lose by taking a different course, and much to gain. “Relevant experience” is difficulttoappraiseindealingwitha Fed boss, and previous proven excellence has anyway not always been targeted. Greenspan notably had had no success at any previous serious job; in fact, come to think of it he had had no serious job, really. He did, though, have a proven record of almost laughable failure as an economic prognosticator to the stock market back in the 1970s. So, who meets my description? Brooksley Born, Sheila Bair, and possibly Thomas Hoenig (who voted quite often but always in vain against the Fed’s policies) would catch theflavorofmypoint.No,nota prayer, I know. Still it’s the thought that counts.And if my suggestions fall flat, how about a Canadian or a Brit or even a German? Can you even for a minute imagine a foreigner at the Fed? And it used to be the Brits who were considered stodgy.

A Comment on all of the “Explanations of the Crash, Five Years on”

Much has been written in recent months, reviewing the crash of 2008 on its fifth anniversary. Almost all reviews, as usual, see it overwhelmingly as a financial event. Of course, finance is involved in every aspect of the economy almost by definition but, in my opinion, there are two aspects of the real world as opposed to the paper world of debt that are understated in their influence on the crash: commodity price rises and the housing bubble. Commodity prices often spike as part of a general inflation, but this time there was no inflation in wages or consumer prices. Therefore, the remarkable rise in commodity prices – especially oil, which went up almost eight times in nine years with most of the increase in the last year before the peak – took a particularly hard toll on demand. This time prices were driven by both the rapidly rising long-term costs of finding and delivering oil and short-term shortages. Previous spikes in oil have been documented as having caused downturns in the economy, notably in the period between 1972 and 1980. Back then oil was admittedly a larger fraction of U.S. GDP: the direct impact from resource prices as their share of GDP temporarily spiked was a squeeze on the economy of about 8.5% from 1972 to 1980. This time resource price increases squeezed the U.S. economy by a smaller 5%, but that was still a huge impact even spread out over six years, particularly because almost half of the effect was in the 12 months to mid-2008. (See my report in GMO’s Quarterly Letter of October 2012.)

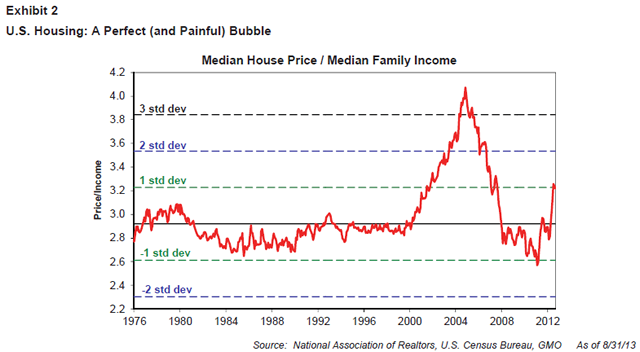

The second factor – the housing bubble – really accounted for why we at GMO saw the trouble coming. Focusing on the financial ratios of banks, on the quality and quantity of their obligations on and off the balance sheet, was so complex – the bank CEO’s were clearly out of their depth for starters – that it is easy to sympathize with those who missed the big picture. The housing market in the U.S., in contrast, was like a lesson in Bubbles for Beginners. Exhibit 2 shows our updated version of the housing bubble. As usual, it was easy to get excited about this too early, but how on earth could you miss it? (Famously, Greenspan, Bernanke, and Yellen, not only could not or would not see this 3½ sigma outlier, but they added words of encouragement that it was somehow a normal response to a decently strong economy.) Much stronger economies, including some with greater inflation, had somehow not had the same stimulating effect on housing. Certainly at GMO, because we make a fetish of studying bubbles, we had to eat and sleep with the knowledge that this bubble would go the way of all bubbles. And what a beautiful looking bubble it became. Nice lines. With a modest overrun before moving back to trend. The best aspect to this was that you could easily calculate the primary impact of the bust: it would involve the loss of $7 trillion of perceived personal wealth to get to trend and reach an $8 trillion loss with a modest, typical overrun. Most of which had been borrowed against. To have a serious economic setback you didn’t even need John Paulson and Goldman Sachs to go out of their way to create decidedly odd real estate instruments! Add to this the secondary effects – the building of an extra million houses above trend – clearly unnecessary in the short term. The overrun here was bound to be painful. A record extra 3% of the public had been encouraged, cajoled, or conned into buying a house despite the unprecedented lack of growth in household income and hourly wages tragically being unchanged in real terms since 1970. (If you don’t believe it, check it!) An extra cumulative two million plus houses were built to accommodate them. In this respect the capitalist process here in the U.S. responded to higher prices in the classic way. As it also did in Ireland and Spain, but even more so since their housing bubbles did the impossible and out-bubbled ours. Painfully after the bust, home building would have to cool down half a million or so a year below normal in order to balance the books. And stay below trend for quite a few years. In the U.S. that has all happened according to Hoyle, and we are almost back to normal in home ownership, certainly three-quarters of the way, perhaps within a year of full readjustment. All in all this was an incredibly well-behaved, predictable cycle. The secondary pain of fewer jobs in construction, real estate sales, and real estate financing also added quite predictably to the misery. The tertiary effect is harder to calculate and, I suspect, less predictable: what is consumer behavior after realizing their net worth is so much less than thought and their pension capabilities sometimes brutally reduced? We all generally assume that the wealth effect from housing is greater than that for the stock market and more dangerous, for home ownership involves over 30% more of the general public than stock ownership and those additionally impacted had typically far less liquidity to deal with a crisis than did stockholders.

This is my point: we had the largest price jumps in oil and other commodities ever. Even after adjusting for their lower relative size in GDP it was one of the two most painful commodity squeezes on the economy in a century. Second, you had the only U.S.-wide housing bubble in history. It inflicted $8 trillion of direct losses and trillions of dollars in secondary and tertiary effects. The effect was guaranteed to last for several years. You had them hit together, guaranteeing a deep economic setback and a slow recovery. To me, there seems hardly any room for other financial effects to play a very important role let alone the overwhelming role that they are represented as having played. It is all part of a general bias in our economic thinking that exaggerates the significance of the financial, paper world at the expense of the more mundane, but more important, real world. This exaggeration makes the financial world and all of its pieces seem more important and any partial failure more potentially disastrous than it really is, and works, unless we are careful, much to the advantage of the financial sector and much to the cost of the balance of the economy.

Timing Bear Markets

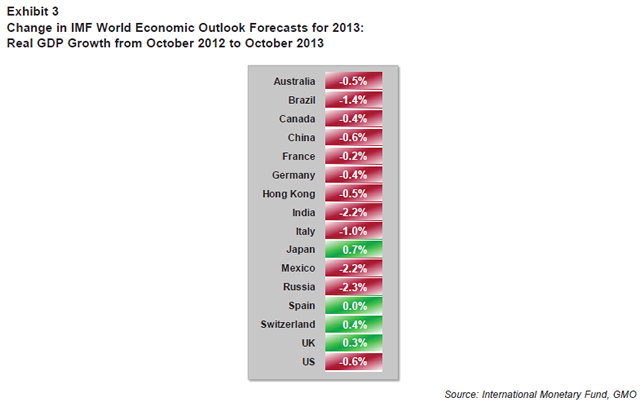

My personalview is that the Greenspan-Bernanke regime of excessive stimulus, now administered by Yellen, will proceed as usual, and that the path of least resistance, for the market will be up. I believe that it would take a severe economic shock to outweigh the effect of the Fed’s relentless pushing of the market. Look at the market’s continued advance despite almost universal disappointment in economic growth. Exhibit 3 shows the economic forecasts for major economic countries made a year ago by the IMF compared to what actually happened. Only Japan was a modest pleasant surprise at 0.7% ahead of forecast and the U.K. and Switzerland scraped home by the skin of their teeth. Everyone else fell short. There have been few such occasions when such broad disappointment with economic growth still allowed the U.S. and most other major economies to make material upward moves in their stock markets. It is yet another testimonial to the global reach of the Fed’s stimulus of equities (as was the very substantial decline in emerging market equities on just talk of tapering!).

In equities there are few signs yet of a traditional bubble. In the U.S. individuals are not yet consistent buyers of mutual funds. Over lunch I am still looking at Patriots’ highlights and not the CNBC talking heads recommending Pumatech or whatever they were in 1999. There are no wonderful and influential theories as to why the P/E structure should be much higher today as there were in Japan in 1989 or in the U.S. in 2000, with Greenspan’s theory of the internet driving away the dark clouds of ignorance and ushering in an era of permanently higher P/Es. (There is only Jeremy Siegel doing his usual, apparently inexhaustible thing of explaining why the market is actually cheap: in 2000 we tangled over the market’s P/E of 30 to 35, which, with arcane and ingenious adjustments, for him did not portend disaster. This time it is unprecedented margins, usually the most dependably mean reverting of all financial series, which are apparently now normal.) By June this year, markets felt relatively quiet and under the surface there was still a considerable undertow of risk aversion in the institutions. The Russell 2000 and the GMO High Quality universe1 were both just level with the S&P, all up 16%. Normally we would have expected the Russell to outperform handsomely. However, since then speculation has perked up so that today, the broad U.S. market is up 20% and the Russell 2000 is a more typical six points ahead while stocks in the GMO High Quality universe are several points behind. We have also had a sharp and unexpected uptick in parts of the IPO market in the U.S., so I would think that we are probably in the slow build-up to something interesting – a badly overpriced market and bubble conditions. My personal guess is that the U.S. market, especially the non-blue chips, will work its way higher, perhaps by 20% to 30% in the next year or, more likely, two years, with the rest of the world including emerging market equities covering even more ground in at least a partial catch-up. And then we will have the third in the series of serious market busts since 1999 and presumably Greenspan, Bernanke, Yellen, et al. will rest happy, for surely they must expect something like this outcome given their experience. And we the people, of course, will get what we deserve. We acclaimed the original perpetrator of this ill-fated plan – Greenspan – to be the great Maestro, in a general orgy of boot licking. His faithful acolyte, Bernanke, was reappointed by a democratic president and generally lauded for doing (I admit) a perfectly serviceable job of rallying the troops in a crash that absolutely would not have occurred without the dangerous experiments in deregulation and no regulation (of the subprime instruments, for example) of his and his predecessor’s policy. At this rate, one day we will praise Yellen (or a similar successor) for helping out adequately in the wreckage of the next utterly unnecessaryfinancial and asset class failure. Deregulation was eventually a disappointment even to Greenspan, shocked at the bad behavior offinancial leaders who, incomprehensibly to him, were not even attempting to maximize long-term risk-adjusted profits.Indeed, instead of the “price discovery” so central to modern economic theory we had “greed discovery.”

(Memo: “price discovery” is the process that happens in an open and competitive and unregulated market, where the interplay of supply, demand, and cost structures determines the efficient price. “Greed discovery” is the process by which a vastly and unnecessarily complicated financial system is exploited by expert insiders. These insiders have far more knowledge than the lambs – formerly known as clients – and without adequate regulations the lambs are defleeced in a surge of “rent seeking.”)

In the meantime investors should be aware that the U.S. market is already badly overpriced – indeed, we believe it is priced to deliver negative real returns over seven years – and that most foreign markets having moved up rapidly this summer are also overpriced but less so. In our view, prudent investors should already be reducing their equity bets and their risk level in general. One of the more painful lessons in investing is that the prudent investor (or “value investor” if you prefer) almost invariably must forego plenty of fun at the top end of markets. This market is already no exception, but speculation can hurt prudence much more and probably will. Ah, that’s life. And with a Fed like ours it’s probably what we deserve.

Inconvenient Conclusion

Be prudent and you’ll probably forego gains. Be risky and you’ll probably make some more money, but you may be bushwhacked and, if you are, your excuses will look thin. Your call. We of course are making our call.

Postscript 1

What can go wrong for the market? There is a slow and for me rather sinister slowing down of economic growth, most obviously in Europe but also globally, that could at worst overwhelm even the Fed. The general lack of fiscal stimulus globally and the almost precipitous decline in the U.S. Federal deficit in particular do not help. What are the odds in the next two years? Perhaps one in four.

Postscript 2

Hot off the press, for a less serious moment at our client conference comes the latest update (or data mining, if you prefer) of the… ta da…Presidential Cycle. Since October 1977 when GMO started, 36 years have passed. In that time – when logic and experience say you stimulate to help the next election – the third year has been over 1½ times the other three added together and years one and two, when you should be tightening, have been commensurately weak. For the weakest five cycles, the average of years one and two was negative but for three cycles it was strong, even very strong. These three cannot be blamed totally on the Greenspan-Bernanke regime’s tendency to overstimulate, but mostly they can. Bearing in mind that for us Presidential years run October 1-September 30, these three two-year returns were 1996, +48%; 1984, +43%; and 2004, +19%. Now, this is the scary part. 1996 ended in the 2000 crash, 1984 in the crash of 1987, and 2004 in thefinancial crash of 2008. In the current cycle we are already up 19% with a year to run! Of course, it may turn out to be a very strong two years and all will be well. Who knows?

1 High Quality Universe represents the simulated performance of a market capitalization-weighted portfolio of stocks in the highest 25% of a universe comprised of the top 1000 U.S. stocks by market capitalization based on GMO’s quality definition. GMO defines quality companies as those with high profitability, low profit volatility, and minimal use of leverage.

Disclaimer: The views expressed are the views of Jeremy Grantham through the period ending November 18, 2013, and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Copyright © 2013 by GMO LLC. All rights reserved.

© GMO

© GMO