The Fed’s decision in September to maintain it’s policy of asset purchases, better known as Quantitative Easing (QE), caught the broader market by surprise. Fed “tapering” of QE was broadly expected to begin in September. The Fed’s decision to delay the reduction of QE pushed back the date upon which anticipated tapering would begin. This resulted in a meaningful rally in Treasury bond prices in September. To the surprise of many media pundits calling for ever higher interest rates, US Treasury yields ended October at 2.55%, virtually unchanged from 7/31/13. During this same period the municipal bond market enjoyed a powerful rally as sophisticated, cross-over buyers and individual investors recognized the significantly oversold conditions that persisted in the municipal bond market.

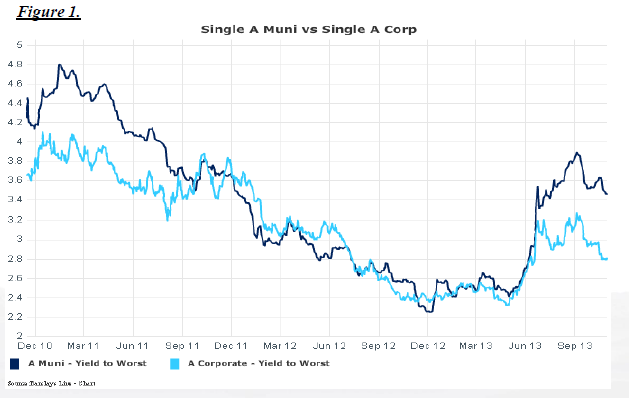

As our clients and loyal readers may recall, we extensively discussed the nature and scale of the municipal bond investment opportunity in our July market commentary. The Barclay’s Capital Municipal Bond Index returned +1.49%, or over +6.09% on an annualized basis, during the period beginning 7/31/2013 ending 10/31/13. The relative attractiveness of municipal bonds, when compared to other fixed income vehicles, provided investors the opportunity to achieve yields on tax-free municipal bonds that were well in excess of yields available on taxable fixed income securities on an absolute basis. This condition is often temporary given the substantially higher taxable equivalent returns taxpayers realize owning tax-free municipal bonds. Municipal bond market cheapening attracted the attention of traditional as well as non-taxable investors given the expectation that tax-free bonds look likely to continue to outperform in the future. Figure 1 clearly illustrates the currently wide yield advantage that single “A” rated municipal bonds offer relative to single “A” rated corporate bonds on an absolute basis.

Investors are also increasingly recognizing the added benefits offered by individual bonds, given that one can reasonably expect principle to be returned at final maturity. On the contrary, investors in bond mutual funds are perpetually exposed to fluctuations of a mutual fund’s net asset value with no assurance of when one’s principle investment may be returned, not-to-mention the varying degrees of leverage and corresponding duration risk associated with closed-end bond funds in particular. Investors should be aware that even during periods of rising rates, individual municipal bonds can deliver attractive tax-free cash flow on a hold- to-maturity basis.

Duration

We spent the third quarter seeking bonds with shorter effective durations and attractive total rate-of-return potential in an effort to capture the relative value created by the inefficient manner in which municipal bonds “roll down” the yield curve as the calendar changes from this year to next. Through the application of quantitative and empirical analysis we have identified several maturities that we believe should materially outperform over the coming weeks and months. We will continue to look for opportunities to overweight maturities that offer better risk-adjusted return potential in client portfolios going forward.

Then There Was Puerto Rico

I spoke to the potential risks investors face as a result of PR’s credit deterioration in an April 4, 2013 BloombergBusiness week story entitled Trouble In Puerto Rican Bonds Could Haunt US Investors. The most recent episode of credit uncertainty surrounding Puerto Rico (PR) erupted over the last few months. Dire headlines regarding PR’s credit deterioration have gripped investor attention. The exposure of mutual funds to the seemingly intractable credit challenges that face the Commonwealth caused greater uncertainty in the municipal bond market as investors scrambled to determine their individual exposures. Holders rushed to liquidate holdings as willing buyers quickly faded away. As our clients may recall, in anticipation of the problems that may lie ahead, we chose to liquidate client positions in Puerto Rico related credits early this year. With the exception of PR Housing Finance Authority, we felt strongly that the possibility of meaningful credit deterioration could effect other PR issuers from a credit and or liquidity perspective. PR Housing bonds, however, are backed by Congressional/HUD appropriations and are, therefore, supported by a stable and distinct source of revenue in our view. We are, therefore, comfortable and confident holding PR Housing bonds on behalf of our clients.

As yields on direct obligations of PR shot up over the past few months, prices fell dramatically, resulting in significant losses for investors who may have been unaware that they were exposed to credit risk on this scale. The worst performing PR bonds declined in value by over 30.00% over the past few months. While we continue to be very selective as it relates to the underlying credit quality of the bonds we purchase on behalf of our clients, we firmly believe that corresponding market uncertainty will continue to create opportunities in high grade municipal bonds as ongoing mutual fund redemptions force fund managers to liquidate higher quality, more liquid holdings, leaving remaining shareholders exposed to ever diminishing liquidity in remaining positions. Given the greater degree of transparency and individual investor control that separately managed accounts provide, this environment is ideally suited to professionally managed strategies in our view.

We expect the new issue supply of municipal bonds to diminish as investors square positions heading into year-end. While liquidity may be somewhat diminished due to a lack of focus on investing during the final weeks of the fourth quarter, we believe this time of the year can be a very good time to be a buyer of municipal bonds as investors look to optimize their tax situation through tax loss harvesting. This can represent an excellent seasonal period for investors to purchase municipal bonds as sellers tend to be less price sensitive when liquidating for tax purposes.

Investors would, therefore, benefit from a thorough review of that portion of their municipal bond holdings not managed professionally in an effort to better understand their risk exposures to determine whether there is an opportunity to optimally reposition portfolio holdings to take advantage of current market inefficiencies. Please do not hesitate to contact us directly if we can be of any assistance in this regard or if you should have any questions about the municipal bond market more broadly.

Andrew Clinton

President

Important Disclosure Information

Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product made reference to directly or indirectly in this newsletter (article), will be profitable, equal any corresponding indicated historical performance level(s), or be suitable for your portfolio. Due to various factors, including changing market conditions, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter (article) serves as the receipt of, or as a substitute for, personalized investment advice from Clinton Investment Management, LLC. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. A copy of our current written disclosure statement discussing our advisory services and fees is available for review upon request.

© Clinton Investment Management