Five Reasons Inflation Is Still Missing

by Chun Wang, CFA, PRM

Leuthold Weeden Capital Management

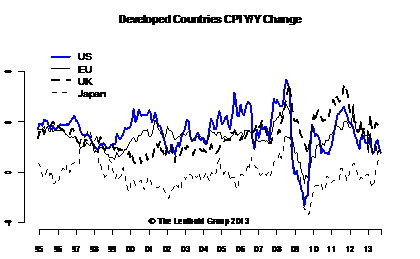

A key factor allowing the Fed to maintain QE is the lack of inflation. You would think after multiple rounds of synchronized global money printing and a recovering global economy that inflation would be felt in more noticeable ways. But the reality is, among the G4 and major emerging countries, only Japan is creating inflation (Chart 1). Even emerging countries have seen inflation weaken in the last few months (chart not shown). The lack of inflation is global in scope, not just within the U.S. Obviously this is much better for emerging countries, where inflation is a real risk, than for developed countries that keep flirting with deflation.

Chart 1

Japan’s recent inflation surge is in large part due to a much weaker yen versus a year ago. The key engines of inflation, such as wage growth and consumption growth, are still anemic. With the yen reversing part of its weakness, the outlook for a sustained rise in inflation is definitely pessimistic.

Inflation in the Eurozone is going in the wrong direction. The recent dip in inflation to 0.7% has put the fear of deflation back in the market and the pressure of further easing back on the ECB.

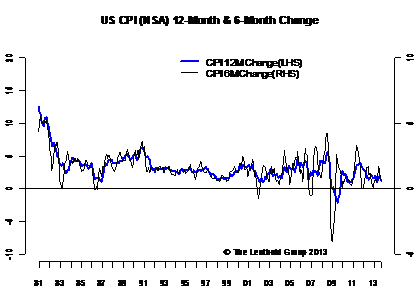

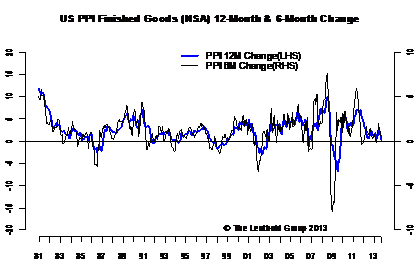

In the U.S., inflation is not much better either. At both the consumer and producer levels, inflation is weakening, not strengthening (Charts 2 & 3). This is puzzling because the Fed is one of the most accommodative central banks in the world, and the U.S. economy is in a better shape than most other countries.

Chart 2

Chart 3

Here are the five reasons we think best explain why inflation is missing in the U.S. There are many inflation drivers, but most fall into two categories: 1) demand, and 2) costs. The demand side, related to the underlying economic strength, tends to have a much longer lasting impact on inflation. The cost side, however, can be influenced by more market-oriented forces and tends to be a little more short-term.

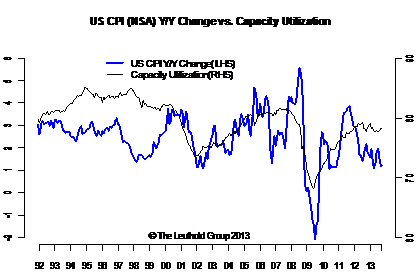

There are two drivers on the demand side. First, overall demand slack is a key contributor to the absence of inflation. Chart 4 shows the U.S. capacity utilization rate (a proxy for demand slack) vs. the CPI. The capacity utilization rate hasn’t gotten above 80 in the post-crisis period, and the trend has been flat-lining. This is consistent with the overall sideways pattern of inflation.

Chart 4

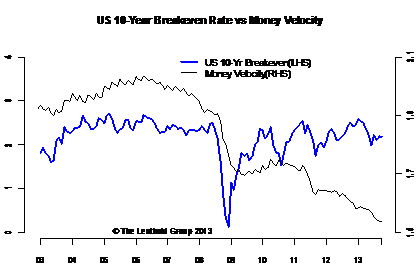

Second, the velocity of money is stubbornly low and getting lower (Chart 5). This has much to do with the clogs in the lending and credit channels. Credits are not easily available to smaller businesses that need them the most, which dampens growth-led investments and employment.

Chart 5

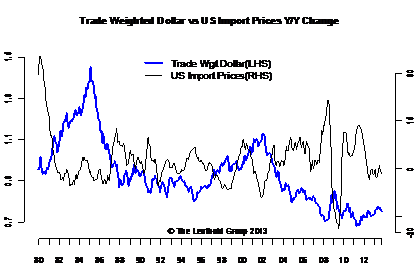

On the costs side, disinflationary forces from outside the U.S., such as exchange rates and import prices, play a big role. The overall stronger dollar in the last few years, in conjunction with lower import prices (Chart 6), has helped keep inflation at bay. As we’ve already alluded to, the U.S. has been importing disinflation from other major countries around the world and that helps put a lid on U.S. inflation.

Chart 6

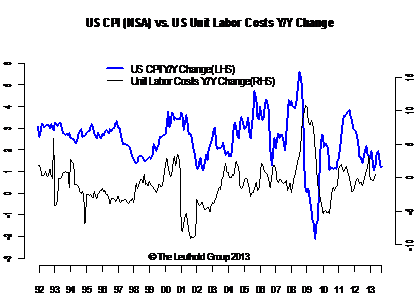

Another important driver on the cost side is unit labor costs. Labor cost inflation has been painfully low in the post-crisis era. The year-over-year change in U.S. unit labor costs has been negative for most of the last few years (Chart 7). This is a direct reflection of the weak employment environment and employees’ general lack of bargaining power when it comes to compensation and benefits. Unless the job picture brightens up soon, there is no reason to believe a wage-led inflationary scenario is imminent.

Chart 7

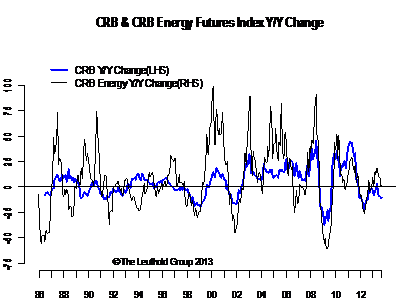

Finally, recent weakness in commodity prices presents a strong disinflationary force (Chart 8). The reasons for the recent drop in commodity prices are two-fold:

Externally, a combination of the new low-growth regime prevailing in emerging countries (particularly China) and the overcapacity issue plaguing the materials sector right now.

And second, domestically, the so-called “energy renaissance” sweeping through the U.S. has greatly reduced energy prices.

Chart 8

Apart from a couple of market-oriented drivers that could reverse course on a short-term basis, we are not seeing convincing evidence of an imminent pick-up in inflation.

Let us be clear. There is most definitely inflation in the financial markets, but that does not seem to benefit the average person in the U.S. The liquidity injected by various central banks went mostly into the financial markets first and foremost; only a small fraction of it trickled down to the average person. That is why all this money printing has not been reflected in various inflation measures.

© Leuthold Weeden Capital