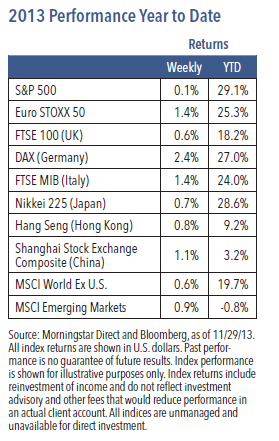

U.S. equities finished higher for an eighth consecutive week as the S&P 500 increased 0.1%,1 representing the longest positive streak since 2004. Inertia may have carried markets forward in a relatively quiet trading week without major headlines. Retail news appeared fairly positive in anticipation of a strong start to the Thanksgiving shopping weekend. Economic data was mixed.

The Big Question: Will the Economy and Earnings Continue to Improve?

In recent Federal Reserve (Fed) communications, Ben Bernanke, Janet Yellen and other prominent FOMC members suggested the tapering of asset purchases requires three conditions:

1. GDP growth must show clear signs of accelerating

2. Employment growth should follow GDP growth and move sustainably higher

3. Inflation has to show signs of moving closer to the 2% target set by the Fed

While there is hope that all three areas will come together, so far the data have not been strong enough. On the growth front, real GDP increased by 2.8% in the third quarter; however, most of the upside surprise was due to faster inventory accumulation.2 Real private final sales grew at a tepid rate of 2.0%.3 The drop in gasoline and other energy prices has likely boosted real disposable income by about 0.5% in the fourth quarter, which can explain some of the rebound in retail sales. On balance, it appears underlying real GDP growth remains stuck at around 2%, close to where it has been for the past three years. We expect GDP growth to increase and the labor market to improve over the coming year, in part due to diminished fiscal drag, easier credit conditions, strengthening household balance sheets, recovering housing market and revival in corporate spending.

Based upon reliable news sources, it appears the Fed will almost certainly stop asset purchases next year and replace QE with forward guidance. The Fed has not been the only central bank considering how to continue monetary easing to support growth. Early last month, the European Central Bank (ECB) cut its official policy rate by 0.25%, bringing the rate to 0.25%.4 The ECB move was clearly meant to reinforce that short-term rates will stay low for a long time. Falling inflation in the Euro area provides a case for maintaining loose monetary policy. If Europe was to succumb to deflation, this could create problems for the common currency, potentially triggering another global financial crisis. In China, the Third Plenum meeting of the Central Committee of the Communist Party produced a reform blueprint that focuses heavily on supply side reforms with respect to spurring market competition and reducing the direct role of the state in economic affairs.

Recent global economic data has softened somewhat, but we anticipate growth will accelerate next year as fiscal drag diminishes and deleveraging pressures abate. A key question for investors is whether this improved economic outlook has already been priced into markets. Economic surveys suggest most investors expect stronger growth, but until recently global cyclical sectors underperformed defensive sectors, implying the ability for equities to price in a healthier environment. Although the path of least resistance for equities continues upward, valuations in several areas appear stretched, signaling a slower pace of appreciation. High levels of spare capacity and falling inflation rates in the developed world should ensure that monetary policy remains accommodative for the foreseeable future.

The Big Picture

In conclusion, the U.S. equity market is likely to continue to grind higher as a result of central bank liquidity, modest economic acceleration, quiet inflation and an improving fiscal situation. We expect the U.S. and global economy to improve in early 2014, permitting some pickup in revenue and earnings growth. However, the gradual improvement will not likely be strong enough to threaten the unprecedented global monetary experiment that has helped underpin the rise in equity valuations. Even though equities may still advance, the rapid run-up in 2013 (and since 2009) has reduced our view of forward long-term return potential to mid- to high-single-digit annual percentage gains. Within the equity market, we prefer companies with positive free cash flow profiles, low valuations, economic sensitivity and/or above-average secular growth.

1 Source: Morningstar Direct, as of 11/29/13. 2 Source: U.S. Department of Commerce Bureau of Economic Analysis, “National Income and Product Accounts Gross Domestic Product, 3rd quarter 2013 (advance estimate),” November 7, 2013, http://www.bea.gov/newsreleases/national/gdp/gdpnewsrelease.htm. 3 Source: U.S. Census Bureau, U.S. Department of Congress, “Advance Monthly Sales for Retail and Food Services October 2013,” November 20, 2013. http://www.census.gov/retail/. 4 Source: European Central Bank, as of 11/29/13, Key ECB Interest Rates, http://www.ecb.europa.eu/ stats/monetary/rates/html/index.en.html.

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. Euro STOXX 50 Index is Europe’s leading Blue-chip index for the Eurozone and covers 50 stocks from 12 Eurozone countries. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. FTSE MIB Index is an index of the 40 most liquid and capitalized stocks listed on the Borsa Italiana. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Non- investment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

GPE-BDCOMM1-1213P

© Nuveen Asset Management