U.S.equitiesfinishedlastweekinbarelynegativeterritory,endingthepositivestreakforthemarket.1 Economicdataconcerningthepost-governmentshutdownclimatehasimproved.Employmentdatabeatestimatesandincreasedby203,000jobsinNovember, and theunemploymentratefellto7.0%,alsosurpassingexpectations.2

Don’t Fear the Taper

Economic progress should provide the Federal Reserve (Fed) with the ammunition it needs to begin tapering purchases of Treasury and other securities possibly as soon as later this month. The Fed may still be concerned about the dip in inflation indicators, as they remain below the target level of 2%.

Weekly Top Themes

- The real GDP upward revision to 3.6% for the third quarter was the fastest quarterly growth rate in almost two years.3 The revision did not generate much enthusiasm since it reflected a buildup of inventory. Part of the inventory accumulation was probably intended, some of it was imported, and other segments will likely be diminished once fourth quarter reporting begins. This does not dampen our expectation of 2.5% to 3.0% real growth in 2014.

- 2013 job gains are running slightly ahead of last year.2 These advances are despite a two-year contraction in nominal federal outlays for the first time in more than five decades. The labor market has improved by almost every measure since last fall.

- The ISM Manufacturing Report for November ended above consensus expectations.4 ISM data tends to lead GDP,and over the last two quarters, the range has been consistent with more than 3.0% real GDP growth.

- The University of Michigan consumer sentiment survey jumped to 82.5 for December.5 This is the highest level since July.

- Positive chatter continues but a final budget agreement has not yet been reached in Washington. The proposed deal would provide a moderate fiscal boost next year by replacing scheduled sequester cuts with increased user fees and other savings spread over time.

The Big Picture

Macroeconomic risks have been diminishing as the global economic recovery slowly broadens and seems to be gathering momentum. The United States, Euro area, Japan and China are all expanding or accelerating simultaneously, which should make growth more durable and likely. Markets are already discounting an improving global economy in 2014. In our view, increased upside risks remain for both bond yields and equity prices, particularly in light of lingering investor uncertainty and cautious positioning. The imminent beginning of Fed tapering represents a possible source of volatility, but G7 central banks remain committed to monetary reflation, and conditions should remain supportive for risk assets.

Although stocks are vulnerable to a correction in the near term given recent significant strength, we continue to advocate a moderately pro-equity and growth posture on a 6- to 12-month time horizon. Skepticism about the fundamentals and durability of the equity rally is widespread, with many investors arguing that equities are expensive and profit margins are unsustainably high. We do not foresee a major risk to 2014 performance as long as the global economy shows an improving trend. A key risk to our forecast is a relapse into recession that could be caused by a policy mistake or a bond market blowup, but we don’t think this is likely.

1 Source: Morningstar Direct,asof12/6/13. 2 Source: Bureau of Labor Statistics, “The Employment Situation – November 2013,” December 6, 2013, http://www.bls.gov/news.release/empsit.nr0. htm.3 Source: U.S. Department of Commerce Bureau of Economic Analysis, “National Income and Product Accounts Gross Domestic Product, 3rd quarter 2013 (second estimate); Corporate Profits, 3rd quarter 2013 (preliminary estimate)” December 5, 2013, http://www.bea.gov/newsreleases/national/gdp/gdpnewsrelease.htm.4 Source: Institute for Supply Management, “November 2013 Manufacturing ISM Report on Business, ®” December 2, 2013, http://www.ism.ws/ismreport/mfgrob.cfm.5 Source: Thomson Reuters, “Surveys of Consumers University of Michigan December 2013 Preliminary,”http://www.sca.isr.umich.edu/.

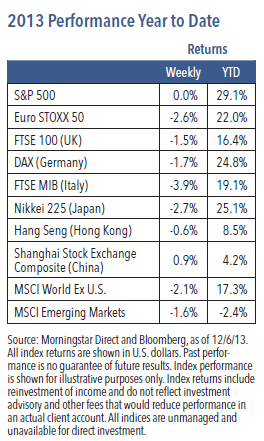

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. Euro STOXX 50 Index is Europe’s leading Blue-chip index for the Eurozone and covers 50 stocks from 12 Eurozone countries. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock

Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. FTSE MIB Index is an index of the 40 most liquid and capitalized stocks listed on the Borsa Italiana. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Non- investment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

GPE-BDCOMM2-1213P

© Nuveen Asset Management