Please note the Economic and Market Update will be on hiatus until January 5, 2014.

Stocks Slide In Leadup To FOMC Meeting

Equity markets sank last week amid investor expectations that the Federal Reserve will begin its tapering process this coming week. The S&P 500 slid 1.6%, its first weekly decline in more than two months, while the Dow fell by a similar magnitude.

It was a relatively quiet week of economic data, but the major indicators released suggested the US economy continue to firm – perversely, a negative in the eyes of most market participants as it heightens the likelihood of QE reduction.

On Tuesday, the National Federation of Independent Business (NFIB) released its monthly small business optimism survey. The index improved to 92.5 in November, slightly ahead of expectations. Eight of the 10 underlying components increased, led by “plans to increase employment” and “now is a good time to expand.” While exhibiting improvement, the net reading for both of those metrics remains fairly close to neutral. Substantially more negative readings persist in the “expect economy to improve” and “earnings trends” components both of which softened further in the month.

NFIB Chief Economist Bill Dunkelberg noted that one emerging concern among many business owners is the impact of the Affordable Care Act and its insurance requirements. Now that the legislation is beginning to take hold, “concern about the cost and availability of insurance [increased] after a long period of no real change. Small business owners who provide health insurance may soon…be obliged to either pay more for the coverage or abandon it and pay the benefit in cash.”

On Thursday, retail sales exhibited continued momentum by increasing 0.7% in November. The prior month was also revised upward, from an original print of 0.4% to 0.6%. A significant chunk of the month’s increase was attributable to motor vehicle sales, which expanded by 1.8%. That sector saw similarly robust results in October, when it gained 1.1%. After excluding the effects of motor vehicles, retail sales increased 0.4%.

After a slow downtrend in retail sales in the middle of 2013, consumer spending appears to have rebounded in the past two months, defying economists’ expectations that negative economic sentiment would erode the measure. According to the economic analysis firm Econoday, the report should bode well for fourth quarter GDP. This takes on greater importance given the undue influence of inventory growth in Q3 figures, which can often reverse in subsequent quarters.

The one primary negative from last week was weekly initial jobless claims. The series spiked on what appears to be a distortion of some kind; claims increased by 68,000 to 368,000, a level not witnessed since October amidst the government shutdown. While this series is notoriously volatile, the four-week moving average indicates that the labor market is slowly gaining ground. While softening slightly this past week, that measure has slowly improved since October’s distortion.

Will 2014 bring an end to central bank intervention?

Nearing the final two weeks of the year, it is customary to look forward to the trends and events that will shape the coming year. A theme that may come to the fore in 2014 revolves around central bankers, specifically the diverging fates in various economies of the world.

Indicative of the challenging global economic climate, website Central Bank News reported that through the first 50 weeks of 2013 there were 486 policy decisions by central banks. Out of those 486 decisions, 112 resulted in interest rates being lowered and rates were raised only 26 times. The remaining decisions resulted in no change.

Here in the U.S., the notion of taper has been weighing on the markets for several quarters now. Economists and strategists alike tried to guess the timing of the Federal Reserve’s move away from asset purchases, but for the most part, their projections were wrong. Fund manager DoubleLine estimates Fed purchases of Treasury and Agency securities accounts for as much as 70% of total net supply in the past six months, the highest level of the past several years.

Source: Business Insider, DoubleLine Funds

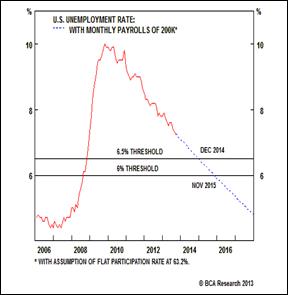

High unemployment, low inflation and a largely dormant economy have been cited as reasons for extending asset purchases. The picture is evolving gradually, as unemployment is declining, inflation stabilizing, and economic growth picking up ever so slightly.

Source: BCA Research

As that improvement became apparent, the FOMC began to communicate its intentions for tapering. To this point, though, uncertainty from the budget and debt ceiling debates in October caused the Fed to stay the course. The FOMC meeting on Tuesday and Wednesday will be the final opportunity for the Fed to begin tapering this year, but with new Fed Chair Janet Yellen waiting to take over early next year, any policy shift appears unlikely at this point.

Based on most expectations, it will be all but inevitable that taper takes effect in 2014, meaning the Fed will be one of the first major central banks to begin stepping away from asset purchases. Depending on the Fed’s communication strategy and the economic climate, the initial stages of taper could present a rocky environment for risk assets, but as the markets adapt, stocks, along with the US Dollar should benefit. Treasury bonds will be less inclined to participate in that benefit.

Europe is an altogether different story. Eurozone unemployment currently stands at all-time highs, just north of 12%, and unemployment in countries like Spain is over 26%. High levels of unemployment will dampen wage growth across the Eurozone and potentially raise deflationary pressure. Combating deflation is a central goal for the European Central Bank and will likely lead to additional market intervention from the ECB in 2014.

Source: Pragmatic Capitalism

The other major economy embracing “unusual” policy measures is Japan, where Prime Minister Abe enacted a series of stimulative fiscal and monetary policy measures. Since implementation, those policies raised growth, increased inflation, and boosted domestic consumption. Despite the early success, questions remain for Japan. Japan’s economic growth picked up, but is already slowing again, wages are falling, and a consumption tax will rise from 5% to 8% in April. With so much uncertainty, the Bank of Japan is expected to undertake further monetary stimulus measures in 2014, leaving Japan in a tenuous situation.

Central banks played an integral role during and post-financial crisis. Major central banks are learning that all economies are not created equal, leading to divergences as we head into 2014. The U.S. looks to be the “cleanest dirty shirt” for the upcoming year, with monetary policy beginning to take a less prominent role. In Europe and Japan, central banks will remain heavily involved in markets, furthering the divergence over the next 12 months.

The week ahead

The forthcoming week includes a full schedule for investors, with a number of economic data reports and the FOMC meeting on Tuesday and Wednesday. The latter will certainly take center stage, with investors looking forward to the Fed’s policy prescription at 2pm on Wednesday.

On the data front, reports include the final estimate of third quarter GDP, industrial production, consumer inflation, housing starts, and existing home sales. No change is expected to Q3 GDP from the second estimate of 3.6%.

Aside from the Fed, other central banks meeting this week include Australia, Czech Republic, Turkey, Hungary, India, and Colombia. The Bank of England will also release minutes from its most recent meeting.

Fortigent Research’s weekly economics report will be taking its usual holiday break this year; we will return on January 5, 2014.

About Fortigent

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value

© Fortigent