Is it Lift off Time for Commodity Prices?

Martin is the Investment Strategist to the AdvisorShares Pring Turner Business Cycle ETF (DBIZ)—and since 1984, he has published the “Intermarket Review,” a monthly global market report revered among analysts and market technicians. Martin shares his technical analysis on short and long term market momentum and the potential effect for commodity prices.

Since records began in the early nineteenth century industrial commodity prices have alternated between secular bull and bear markets averaging 20-years. Sometimes, such as the post 1980 period, “bear markets” have taken the form of trading ranges, but the alternating pattern nevertheless still exists. The current secular bull began in December 2001. If 2011 marked its peak it will have been one of the shortest on record. Our work though, argues otherwise.

One indicator that we have found to be helpful in this regard is a price oscillator (trend deviation) based on the relationship between a 60- and 300-month simple moving average. Secular buy and sell signals are triggered when it crosses above and below its 48-month MA. These turning points have been flagged in the lower panel of Chart 1 with the red and green arrows. The secular model, referred to in the text, uses these signals along with a trend reversal factor as confirmation. Hence the occasional black highlighted neutral status.

Chart 1 US Commodity Prices versus a Secular Trend Oscillator

Up until a couple of months ago the indicator itself had been in a declining phase and was getting pretty close to its fifth secular sell signal since the mid-nineteenth century. However, it has now started to tick up and that suggests higher prices. We would be skeptical of this small change were industrial commodity prices at the top of a primary bull market. However, long-term momentum in Chart 2 has just started to turn up. This clearly points more in the direction of a youthful bull than a tired bear.

Chart 2 CRB Spot Raw Industrials and Smoothed Long-Term Momentum

Directional changes in the secular oscillator are quite rare. Even though the latest uptick may appear miniscule, it strongly suggests that a new up leg in the secular bull market is now underway. In this respect three of the four olive green arrows in Chart 1 show that previous mid-course trajectories were all followed by above average rallies.

Our conclusion is that this propitious conjunction of positive cyclical and secular forces, will result in a lift off for commodity prices.

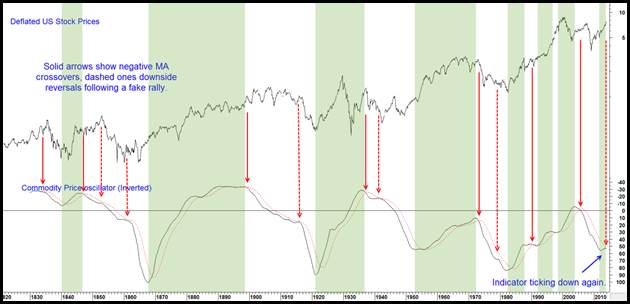

Equity investors will be interested to learn that the direction of our secular commodity oscillator has a broad influence on secular trends of stocks. Actual downside reversals in this oscillator have all represented confirmation that a new secular bull market for equities was underway.

Chart 3 Secular Equity Trends versus Secular Commodity Momentum

To make this concept come alive the oscillator has been plotted inversely in Chart 3 so that its movements correspond with those of deflated equity prices.

The green shaded areas show when the oscillator is in a rising mode i.e. when secular commodity price momentum is declining. Most of the time, this kind of environment is bullish for the very long-term trend of equities. The 1929-32 deflationary pocket is an obvious exception that proves equities abhor unstable commodity prices in either direction. The solid arrows point up when this inversely plotted oscillator crosses below its MA and the dashed ones when it experiences a mid-course change of direction. Both events seem to trigger a poor environment for equities. Remember the relationship is not a precise timing device. However, since the oscillator has started to decline again this clearly elevates the risk of holding equities and the likelihood of a resumption of the secular bear.

© AdvisorShares