Macro Factors and Their Impact on Monetary Policy,

The Economy and Financial Markets

How to Boost the U.S. Economy

In the 17 quarters since the current recovery began in June 2009, gross domestic product (GDP) has grown just 10.3%, after adjusting for inflation. In the other 10 recessions since World War II, GDP on average grew 18.5% after 17 quarters of recovery, according to Bureau of Economic Analysis data. Average annual GDP growth since June 2009 has been 2.2% versus the average of 4.1% in the 10 prior recoveries, which is more than 40% slower. The contrast in growth is even more striking when considering the amount of fiscal and monetary accommodation that supplemented the current recovery. The Federal Reserve has kept the federal funds rate near 0% for more than five years but the demand for loans remains weak. The Fed has expanded its balance sheet from $900 billion in 2007 to more than $4 trillion in 2013, but excess bank reserves exceed $2.56 trillion. Most of the money the Fed has created through the expansion of its balance sheet is sitting dormant while banks collect $6.25 billion on the 0.25% the Fed pays for excess reserves. During the course of the current recovery, the number of Americans receiving food stamps has grown almost 50% and now includes 47 million Americans who receive an average of $133 per month in food stamps. The Agriculture Department says the food stamp program cost $79.8 billion last year. Since 2008, federal unemployment benefits have been extended 12 times to a maximum of 99 weeks. The total cost of these federal extensions has been $210 billion, according to the Labor Department. The extended unemployment benefits and food stamp program, along with dozens of other assistance programs, were intended to support those who needed help as well as sustain aggregate demand and the overall economy. Between 2009 and 2012, the federal government ran annual deficits that totaled more than $5 trillion to offset the loss of demand from consumers and businesses. The recession would have been deeper, more protracted, and the recovery even weaker without the government deficit spending.

In the 17 quarters since the current recovery began in June 2009, gross domestic product (GDP) has grown just 10.3%, after adjusting for inflation. In the other 10 recessions since World War II, GDP on average grew 18.5% after 17 quarters of recovery, according to Bureau of Economic Analysis data. Average annual GDP growth since June 2009 has been 2.2% versus the average of 4.1% in the 10 prior recoveries, which is more than 40% slower. The contrast in growth is even more striking when considering the amount of fiscal and monetary accommodation that supplemented the current recovery. The Federal Reserve has kept the federal funds rate near 0% for more than five years but the demand for loans remains weak. The Fed has expanded its balance sheet from $900 billion in 2007 to more than $4 trillion in 2013, but excess bank reserves exceed $2.56 trillion. Most of the money the Fed has created through the expansion of its balance sheet is sitting dormant while banks collect $6.25 billion on the 0.25% the Fed pays for excess reserves. During the course of the current recovery, the number of Americans receiving food stamps has grown almost 50% and now includes 47 million Americans who receive an average of $133 per month in food stamps. The Agriculture Department says the food stamp program cost $79.8 billion last year. Since 2008, federal unemployment benefits have been extended 12 times to a maximum of 99 weeks. The total cost of these federal extensions has been $210 billion, according to the Labor Department. The extended unemployment benefits and food stamp program, along with dozens of other assistance programs, were intended to support those who needed help as well as sustain aggregate demand and the overall economy. Between 2009 and 2012, the federal government ran annual deficits that totaled more than $5 trillion to offset the loss of demand from consumers and businesses. The recession would have been deeper, more protracted, and the recovery even weaker without the government deficit spending.

There are many factors contributing to the lethargic growth experienced during the current recovery, but the common denominator curbing GDP growth is lack of demand. The question on our minds is what can be done to jump start GDP growth so it accelerates from the 2% range of the past three years and achieves a pace of self-sustaining growth? The challenge is to increase demand within the current monetary and fiscal restraints. The Federal Reserve’s traditional monetary policy  tools have been exhausted. Short-term real interest rates have been negative for years and quantitative easing (QE) has already run its course. In our opinion, the Fed’s reliance on forward guidance is basically jawboning to the extreme, and it is unlikely to do much in spurring an increase in demand. At best, the Fed’s forward guidance will limit how fast and how much longer-term interest rates increase. Fiscal policy has been a net drag on growth as federal spending contracted from $3,603 trillion in 2011 to $3,454 trillion in 2013. The Federal budget has contracted from a $1.3 trillion deficit to a $680 billion deficit in 2013 due to economic growth, tax increases, sequestration spending cuts and one-time contributions from Fannie Mae, Freddie Mac and the Federal Reserve. In the current political environment, spending increases or tax cuts are “dead on arrival,” so fiscal policy can’t be used to boost demand.

tools have been exhausted. Short-term real interest rates have been negative for years and quantitative easing (QE) has already run its course. In our opinion, the Fed’s reliance on forward guidance is basically jawboning to the extreme, and it is unlikely to do much in spurring an increase in demand. At best, the Fed’s forward guidance will limit how fast and how much longer-term interest rates increase. Fiscal policy has been a net drag on growth as federal spending contracted from $3,603 trillion in 2011 to $3,454 trillion in 2013. The Federal budget has contracted from a $1.3 trillion deficit to a $680 billion deficit in 2013 due to economic growth, tax increases, sequestration spending cuts and one-time contributions from Fannie Mae, Freddie Mac and the Federal Reserve. In the current political environment, spending increases or tax cuts are “dead on arrival,” so fiscal policy can’t be used to boost demand.

One of our favorite themes is the unintended consequences of policies that are well intended, but often have negative unintended consequences. For instance, the Federal Reserve slashed interest rates from 5.25% in 2007 to 0.25% in 2008 to stabilize the financial system and prevent a complete financial collapse. The Fed’s actions were necessary, and although criticized by some, proved successful. Unfortunately, the unintended consequence of the Fed’s 0% rate policy has been to severely hurt a generation of hardworking Americans, who played by the rules, saved for their retirement and lived modestly so they could enjoy their golden years. Virtually overnight the income generated from their nest eggs invested in certificates of deposit or money market funds was slashed by 80%. One could say that this situation isn’t fair and be correct. It was done for the greater good of bailing out banks that were mismanaged but too big to fail. The Federal Reserve’s forward guidance announced after the December 18 Federal Open Market Committee (FOMC) meeting, effectively sentences these Americans to at least another two years of what feels like saver’s hell. Despite our deeply held trepidation of the unintended consequences of policy initiatives, we are going to make a suggestion that we are confident of in one respect. It is certain to ruffle a few feathers.

One of our favorite themes is the unintended consequences of policies that are well intended, but often have negative unintended consequences. For instance, the Federal Reserve slashed interest rates from 5.25% in 2007 to 0.25% in 2008 to stabilize the financial system and prevent a complete financial collapse. The Fed’s actions were necessary, and although criticized by some, proved successful. Unfortunately, the unintended consequence of the Fed’s 0% rate policy has been to severely hurt a generation of hardworking Americans, who played by the rules, saved for their retirement and lived modestly so they could enjoy their golden years. Virtually overnight the income generated from their nest eggs invested in certificates of deposit or money market funds was slashed by 80%. One could say that this situation isn’t fair and be correct. It was done for the greater good of bailing out banks that were mismanaged but too big to fail. The Federal Reserve’s forward guidance announced after the December 18 Federal Open Market Committee (FOMC) meeting, effectively sentences these Americans to at least another two years of what feels like saver’s hell. Despite our deeply held trepidation of the unintended consequences of policy initiatives, we are going to make a suggestion that we are confident of in one respect. It is certain to ruffle a few feathers.

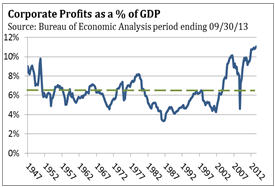

In 1950, 14.0 million workers produced $315 billion of manufactured goods and the average annual salary was $29,500. Both figures are adjusted for inflation in 2009 dollars by the Bureau of Labor Statistics (BLS). In 2007, 14.2 million workers produced $1.9 trillion in manufactured goods, and earned an average wage (in 2009 dollars) of $51,500. No doubt technology has played a huge role in productivity gains since 1950. However, these figures also underscore how income and productivity have not grown commensurately, since incomes rose 75% between 1950 and 2007 while productivity soared 600%. This disparity has continued since the recovery began in 2009. Median income adjusted for inflation has fallen 4.3% since June 2009, according to U.S. Census Bureau data, while productivity has increased by 6.6%, according to the Bureau of Labor Statistics. As we’ve noted in prior commentaries, corporations have kept costs under control primarily by not adding workers to their payrolls and keeping wage increases small. The net result is that corporate profits as a percent of GDP were a record 11.1% as of September 30, 2013, according to the Commerce Department. To put this into a broader perspective, profit margins are more than 80% above their long-term average of 6.1%, dating back to 1925.

In 2013 public corporations will buy back $482 billion of their stock, and they are on pace to distribute a record $310 billion in dividends, according to Standard and Poor’s. Some of the funding for buybacks and dividends is generated by bond sales at low interest rates (compliments of quantitative easing by the Federal Reserve). It appears that shareholders are being treated more equitably than the productive workers who are responsible for the record profits.

Being aware of the unintended consequences of policy initiatives, we make the following recommendation with a degree of trepidation. One way to increase demand would be to give a 5% pay raise to every employee whose income is between $30,000 and $104,000. The top 20% of wage earners would not be eligible for the raise, nor would the bottom 20%. The 5% pay raise would specifically target the middle class—workers earning just above and below the median income level of $50,000. Since taxes would be deducted, the 5% increase would erase most of the 4.3% decline in median income that has occurred since June 2009. According to the Bureau of Economic Analysis, employee wages and salaries as of September 30, 2013, totaled $7.164 trillion. A 5% increase would put an additional $358 billion in workers’ pockets, equivalent to 2.2% of GDP. Although this income increase would be received over a period of 12 months, it would boost consumer confidence, lift consumer spending and stimulate GDP growth. Since the pay raise would continue in the coming years, it would likely be more effective in lifting growth than a one-time tax cut. Who knows, corporations might increase business spending and make real investments in their future rather than spending almost $500 billion in stock buybacks.

Labor costs comprise about 65% of the cost of goods. To offset higher labor costs, companies would need to increase prices, which would push inflation higher. The Federal Reserve has expressed concern about the risk from low inflation and would prefer inflation to rise toward its 2% target. Paying hardworking employees more would boost inflation and help the Fed achieve one of its goals. Quantitative easing added 0.13% to GDP, according to research by the Federal Reserve Bank of San Francisco. We suspect the 5% increase in income would provide the economy more of a boost than quantitative easing has done so far. A stronger economy would increase tax receipts and raise income taxes, which would narrow the federal budget and strengthen state budgets.

One way to offset higher labor costs is to build on the energy revolution that has occurred in the United States over the past five years. U.S. imports of natural gas and crude oil have fallen 32% and 15%, respectively, according to the U.S. Energy Information Administration. In July, the U.S. produced the equivalent of about 22 million barrels of oil, natural gas and related fuels. An analysis of global data by the Wall Street Journal suggests the U.S. is likely to overtake Russia as the world’s largest producer of oil and gas in 2013. As domestic production rises, lower energy costs make U.S. companies more competitive in a global economy. Over time cheaper energy will translate to more jobs being retained in the U.S. and attract jobs from overseas. BASF is a 150-year-old German company and the world’s largest chemical maker. BASF is shifting more of its production and research investment to the United States to take advantage of America’s cheaper energy and biotechnology research. BASF has estimated that it could save $688 million a year in energy costs if its German plants were located in the U.S. For example, German industry pays more than $12.00 per million British thermal units (BTUs), versus a cost of $4.40 for the same amount in the U.S. Since 2010, BASF has doubled its investment in its U.S. plants to $1 billion per year and plans to maintain that annual investment through 2017. Although the $1 billion investment by BASF is a drop in the bucket of our $16 trillion economy, we believe the symbolism of this investment should be heralded. Germany is one of the most productive nations in the world, and the most productive in the European Union. A decade ago China capitalized on its cheap labor to rapidly grow its economy and boost the standard of living for hundreds of millions of its citizens. We think the U.S. should continue to capitalize on its energy technology and natural resources to improve living standards and stimulate job creation.

We are optimistic in the United States’ capacity in coming decades to craft environmental guidelines that will allow the U.S. to safely utilize its natural resources and move toward greater use of renewable energy sources. Our optimism is not based on wishful thinking. According to Environmental Protection Agency data, carbon monoxide emissions declined by 72% between 1980 and 2012, lead emissions fell by 99% and sulfur dioxide dropped by 79%. These results are all the more remarkable since the number of vehicle miles driven between 1980 and 2012 rose 92%, increasing from 1.54 trillion miles to 2.96 trillion miles. The environmental achievements over the past three decades too often go unrecognized by those who were most responsible for them–environmentalists.

U.S. Economy

At the conclusion of the FOMC meeting on December 18, the Fed published its 2014 projections for GDP growth, unemployment and inflation. These projections are derived from estimates made by the members of the FOMC and the presidents of the 12 Federal Reserve districts. To arrive at what the Fed refers to as the “central tendency,” the three highest and lowest estimates are excluded. The central tendency for GDP growth in 2014 is 2.8-3.2%, which is slightly different than the 2.9-3.1% central tendency projection made in September. Of course, the Fed could simply say it expects 2014 GDP growth to be around 3%, but that doesn’t sound as nearly as authoritative as a central tendency reading. While using the phrase central tendency may sound impressive, it hasn’t helped the Fed’s forecasting accuracy in recent years, since they have consistently overestimated the economy’s rate of growth. We think the Fed’s GDP projection is likely to prove too optimistic in 2014 as well.

The Commerce Department’s first estimate for third quarter GDP was 2.0%, which was revised up to 3.6% in early December. Although this revision sounded good, the increase from 2.0% to 3.6% was due entirely to a 1.6% jump in the value of accumulated inventories. On December 20, the Commerce Department reported its final revision (until it’s revised sometime in the future) and now estimates GDP expanded by 4.1%. The rise from 3.6% to 4.1% was fueled by consumer spending, as consumers purchased more cars and other durable goods than expected. In the third quarter, sales of durable goods jumped 7.9% and sales of nondurable goods rose 2.8% while services increased just 0.7%. Final sales rose 2.5% in the third quarter, up from 2.1% in the second quarter. The increase in final sales from 2.1% to 2.5% is a more accurate assessment of the economy’s strength than the 4.1% GDP figure, since the 1.7% increase in inventories during the third quarter will not be repeated in coming quarters.

The Commerce Department’s first estimate for third quarter GDP was 2.0%, which was revised up to 3.6% in early December. Although this revision sounded good, the increase from 2.0% to 3.6% was due entirely to a 1.6% jump in the value of accumulated inventories. On December 20, the Commerce Department reported its final revision (until it’s revised sometime in the future) and now estimates GDP expanded by 4.1%. The rise from 3.6% to 4.1% was fueled by consumer spending, as consumers purchased more cars and other durable goods than expected. In the third quarter, sales of durable goods jumped 7.9% and sales of nondurable goods rose 2.8% while services increased just 0.7%. Final sales rose 2.5% in the third quarter, up from 2.1% in the second quarter. The increase in final sales from 2.1% to 2.5% is a more accurate assessment of the economy’s strength than the 4.1% GDP figure, since the 1.7% increase in inventories during the third quarter will not be repeated in coming quarters.

The solid-looking GDP report has raised expectations for growth in 2014, which also increases the potential of disappointment should growth falter. We think there are a number of reasons why growth is likely to slow at some point during 2014. Even if the slowing is merely a pause, investors are likely to become concerned about the Fed’s decision to reduce its QE3 purchases in light of slower growth, and wonder whether the Fed might even reverse its decision.

The lack of healthy income growth is the primary reason we think final sales will not grow faster than 2.5% in 2014. Despite a modest improvement in job growth, annual income growth is still rising just 2.0-2.2%. Unless income growth improves significantly, most consumers simply don’t have the disposable income to spend without increasing their credit card usage or reducing the amount they save. As we forecast in our July commentary, the rate of improvement in the housing market has slowed, with existing and new home sales below their summer peaks. The Fed’s additional QE3 purchases and its forward guidance will likely succeed in keeping the 10-year Treasury yield below 3.25%, which should keep mortgages steady for a few months. The risk, however, is that yields rise and mortgage rates climb above 5%, which would negatively impact the housing market.

The lack of healthy income growth is the primary reason we think final sales will not grow faster than 2.5% in 2014. Despite a modest improvement in job growth, annual income growth is still rising just 2.0-2.2%. Unless income growth improves significantly, most consumers simply don’t have the disposable income to spend without increasing their credit card usage or reducing the amount they save. As we forecast in our July commentary, the rate of improvement in the housing market has slowed, with existing and new home sales below their summer peaks. The Fed’s additional QE3 purchases and its forward guidance will likely succeed in keeping the 10-year Treasury yield below 3.25%, which should keep mortgages steady for a few months. The risk, however, is that yields rise and mortgage rates climb above 5%, which would negatively impact the housing market.

At the end of 2013, 1.3 million people lost their extended unemployment benefits, with another 850,000 likely to lose their benefits by the end of the first quarter of 2014. According to the White House, a total of 4.8 million people could be without unemployment benefits by the end of 2014. The Congressional Budget Office estimates the lost unemployment benefits will total $25 billion and shave 0.10-0.15% off 2014 GDP. At the risk of sounding cynical, we suspect job growth could rise in coming months as some of those who lost their benefits are more motivated to find a job. If so, some of the lost GDP could be recovered by higher job growth.

At the end of 2013, 1.3 million people lost their extended unemployment benefits, with another 850,000 likely to lose their benefits by the end of the first quarter of 2014. According to the White House, a total of 4.8 million people could be without unemployment benefits by the end of 2014. The Congressional Budget Office estimates the lost unemployment benefits will total $25 billion and shave 0.10-0.15% off 2014 GDP. At the risk of sounding cynical, we suspect job growth could rise in coming months as some of those who lost their benefits are more motivated to find a job. If so, some of the lost GDP could be recovered by higher job growth.

November U.S. auto sales were the highest since February 2007, running at an annual pace of 16.4 million vehicles, according to industry researcher Autodata Corporation. Sales are being boosted by a number of factors. According to the car shopping website TrueCar.com, the average price for a new vehicle was $200 less than in November 2012, which suggests dealers are discounting more aggressively. Prior to the 2008 recession, leasing accounted for 16% - 20% of sales. According to online automotive resource Edmunds.com, leasing has accounted for 26% of new vehicle purchases in 2013. Credit standards for new car purchases are almost as loose as they were in 2007. Experian Automotive determined that the average credit score for new car loans was 753 at the end of September, down 22 points over the past four years and just 4 points above the low of 749 in 2007. Nonprime, subprime and deep subprime auto loans made up 26% of all new vehicle financing in the third quarter, up from 24.8% in 2012. Nonprime, subprime and deep subprime loans for used cars and trucks rose to 55% in the third quarter, up from 54.5% a year ago. Deep subprime loans include borrowers with credit scores below 550. Fueled by low interest rates and easy credit, the total amount of outstanding auto loans hit a record high of $845 billion at the end of September, according to the Federal Reserve Bank of New York. The average amount financed for a new car increased to $26,719, according to Experian Automotive. Credit information provider TransUnion expects the average auto loan for both new and used cars to reach a record $16,942 in the fourth quarter.

With sales up, many car manufacturers are pushing dealers to accept more inventory, since Chrysler, Ford and General Motors record sales when vehicles are shipped to dealers. Normally, inventories are maintained between 60 and 80 days. Currently, dealers are carrying a 90-day inventory, which means they are 30% above normal. The higher-than-normal vehicle inventories suggest that carmakers have been running production at a fast clip in recent months. In November, the ISM Manufacturing Index rose for a sixth consecutive month to 57.3, the highest level since spring 2011. Inventories will grow even larger relative to sales if sales activity slows from its recent six-year high. Even if sales hold up, automakers will likely lower production in coming quarters to bring inventories back to normal levels. As this develops, the ISM Manufacturing Index is likely to fall. Auto sales and production rates are not likely to increase in 2014 from the levels experienced in the second half of 2013.

With sales up, many car manufacturers are pushing dealers to accept more inventory, since Chrysler, Ford and General Motors record sales when vehicles are shipped to dealers. Normally, inventories are maintained between 60 and 80 days. Currently, dealers are carrying a 90-day inventory, which means they are 30% above normal. The higher-than-normal vehicle inventories suggest that carmakers have been running production at a fast clip in recent months. In November, the ISM Manufacturing Index rose for a sixth consecutive month to 57.3, the highest level since spring 2011. Inventories will grow even larger relative to sales if sales activity slows from its recent six-year high. Even if sales hold up, automakers will likely lower production in coming quarters to bring inventories back to normal levels. As this develops, the ISM Manufacturing Index is likely to fall. Auto sales and production rates are not likely to increase in 2014 from the levels experienced in the second half of 2013.

Finally, there is a risk that the Affordable Care Act (ACA) will prove to be more disruptive and costly than expected. Healthcare represents 18% of GDP, so almost any change, no matter how flawlessly executed, would be modestly disruptive, since most people find change to be stressful. So far we have not heard anyone describe the rollout of the Affordable Care Act as flawless. The success of the ACA is largely dependent on 40% of people between 18 and 34 enrolling in the new healthcare exchanges. Younger people tend to have lower medical costs and their premiums are needed to help pay for older enrollees who incur more medical costs. It’s far too soon to make any conclusions, but so far most state exchanges are running well short of the 40% target. Some enrollees are finding they will be able to lower their monthly premium costs, but will do so at the expense of higher deductibles. In the short run they may come out ahead, but could face much higher deductible costs if they don’t stay healthy for the entire year. There is the risk that healthcare costs could weigh on consumer spending later in 2014 as more consumers dig into their pocketbooks to pay for higher deductibles.

U.S Stocks

We believe that most headlines in the coming months will focus on how well the stock market performed in 2013 and overlook how low volatility remained throughout the year. The S&P 500 Index’s largest correction was a mere -5.75% between May 21 and June 24, after Federal Reserve Chairman Ben Bernanke broached the subject of reducing QE3 on May 22. As the nearby table illustrates, the other corrections in 2013 were extremely shallow. In addition to the Fed maintaining QE3, there were a number of other contributing factors that kept volatility low. Although the economy didn’t accelerate in the course of 2013, it did grow fast enough for S&P 500 earnings to grow about 6%, but not so fast  for the Federal Reserve to curtail QE3. Corporations continued to aggressively buy back their stocks, with $128 billion in purchases in the third quarter, according to S&P Dow Jones Indices. The gain in the stock market also boosted investor psychology with inflows into equity mutual funds and exchange-traded funds rising smartly. Other than a brief bout of selling pressure in late May and June, the overall lack of selling pressure provided the stock market a significant boost. It doesn’t take much buying to lift the stock market if selling pressure is low.

for the Federal Reserve to curtail QE3. Corporations continued to aggressively buy back their stocks, with $128 billion in purchases in the third quarter, according to S&P Dow Jones Indices. The gain in the stock market also boosted investor psychology with inflows into equity mutual funds and exchange-traded funds rising smartly. Other than a brief bout of selling pressure in late May and June, the overall lack of selling pressure provided the stock market a significant boost. It doesn’t take much buying to lift the stock market if selling pressure is low.

With the rising tide lifting almost all stocks, those short sellers attempting to profit from a market decline have had a tough year and many have given up. Investors who sell a stock short don’t own it so they have to borrow the amount of shares they want to short from a firm or investor who does own the shares. If the short seller can buy below the price the shares were sold short, they profit from the difference. For example, a short seller sells XYZ stock at $100 and six months later buys it for $80, making $20 in the process. The profit is no different than an investor who buys XYZ at $80 and later sells it for $100. However, if XYZ rallies to $120 after being sold short at $100, the short seller would lose $20 if the shares were bought at $120 to close their short trade. Markit Equity Research monitors the number of shares that have been borrowed by institutional investors around the world. In June 2012, 2.9% of all the company shares in the S&P 500 were on loan, indicating they had been sold short. As of November 20, 2013, the percent of S&P 500 shares sold short had declined to 2.2%, a 24% drop and a record low. Buying by short sellers has been another source of demand for stocks. Through November 20, 2013, the 50 S&P 500 stocks with the highest short ratio were up 50% more than the S&P 500 itself (40% vs. 26%).

Although the S&P 500’s price-earnings (P/E) ratio is reasonable at 15 times 2013 earnings, James Tobin’s Q ratio, Robert Shiller’s cyclically adjusted price-earnings (CAPE) ratio and the stock market’s capitalization as a percentage of U.S. GDP, all suggest the stock market is not as fairly valued as the P/E ratio implies. With so much going right, bullish sentiment regarding the U.S. stock market has reached a multidecade high. According to the weekly measure of investor sentiment by Investors Intelligence, the ratio of bulls to bears is at its highest in 26 years. As we’ve noted in prior commentaries, the stock market doesn’t decline because valuations are excessive or because investors have become overly bullish. Most institutional money managers and mutual fund managers are optimistic, so they will only sell if they are confronted with economic data that contradicts their positive outlook.

The high level of bullish sentiment and valuation suggests the market could be approaching a more significant top should economic growth disappoint in coming months. The current bull market will be five years old on March 6, 2014, which has been a noteworthy “age” in the past. The great secular bull market of the 1980s began after the S&P 500 bottomed on August 9 at 102.20. By August 25, 1987, and after a gain of 229%, the S&P 500 reached an intraday high of 336.77. After bottoming on October 10, 2002, the S&P 500 didn’t peak until it reached 1576.09 on October 11, 2007. The amount of time for each of these bull markets is nearly identical. Five years and 16 days between August 9, 1982, and August 25, 1987, versus five years and one day for the rally off the October 10, 2002, low. We would be inclined to dismiss this as just a coincidence more worthy of cocktail party chatter than the distinguished “Macro Strategy Review.” However, the August 14, 1987, Investors Intelligence weekly sentiment survey recorded 3.50 times as many bulls as bears, and in the week of October 19, 2007, there were 3.21 as many bulls for each bear. Starting with the week of November 6, 2013, there have been nine consecutive weeks with bulls outnumbering bears by more than 3 to 1, with a reading of 4.2 to 1 during the week of December 27. Sentiment and valuation are currently more excessive than in 1987 or 2007. The only thing missing is a reason to sell.

Based on statistical probability, not economic fundamentals or a crystal ball, the market is likely to experience a decline of at least 10% in the first half of 2014. Since 1980, the average intrayear decline has been -14.7%, according to J.P. Morgan Asset Management. In 2012, the largest decline was -9.93% between April 2 and June 1. As noted earlier, the biggest decline in 2013 was -5.75%. According to financial information provider S&P Capital IQ, the average duration between 10% corrections since 1945 has been 18 months. The last 10% correction ended in October 2011, so it has been 26 months. History suggests the market is overdue for a 10% correction.

Technically, the market is still in good shape. Our proprietary Major Trend Indicator suggests any correction is likely to be in the 4-7% range in coming weeks. Although the number of stocks making new 52-week highs has contracted since May, the ratio of new highs to new lows is still OK. As we have noted for months, the S&P 500 continues to make higher highs and higher lows, which is the technical definition of an uptrend. As long as the S&P 500 holds above 1,765, the trend is up.

Bonds

Bonds

Based on the pattern since the 10-year Treasury yield bottomed in July 2012 at 1.39%, the short-term interest rate target is 3.15-3.20%. Our guess is that yields will come down after reaching the short-term target, possibly to 2.5-2.7%. The longer-term target is 3.50-3.75%, which was the February 2011 yield high.

Jim Welsh, David Martin, Jim O’Donnell

Macro Strategy Team

Definition of Terms

10-Year Treasury is a debt obligation issued by the U.S. Treasury that has a term of more than one year, but not more than 10 years.

Cyclically adjusted price-earnings (CAPE) ratio is the ratio of stock prices to the moving average of the previous 10 years’ earnings, deflated by the Consumer Price Index.

Federal funds rate is the interest rate at which a depository institution lends immediately available funds to another depository institution overnight.

Federal Open Market Committee (FOMC) is the branch of the Federal Reserve Board that determines the direction of monetary policy.

Gross domestic product (GDP) is the total market value of all final goods and services produced in a country in a given year.

Institute of Supply Management (ISM) Manufacturing Index is a monthly index that tracks the amount of manufacturing activity that occurred in the previous month.

Price-earnings (P/E) ratio is a valuation ratio of a company's current share price compared to its per-share earnings.

Q ratio is a ratio devised by Nobel Laureate James Tobin that suggests that the combined market value of all the companies in the stock market should be about equal to their replacement costs.

Quantitative easing (QE) refers to a form of monetary policy used to stimulate an economy where interest rates are either at, or close to, zero.

S&P 500 Index is an unmanaged index of 500 common stocks chosen to reflect the industries in the U.S. economy.

Valuation is the process of determining the value of an asset or company based on earnings and the market value of assets.

One cannot invest directly in an index.

RISKS

Investing involves risk, including possible loss of principal. The value of any financial instruments or markets mentioned herein can fall as well as rise. Past performance does not guarantee future results.

This material is distributed for informational purposes only and should not be considered as investment advice, a recommendation of any particular security, strategy or investment product, or as an offer or solicitation with respect to the purchase or sale of any investment. Statistics, prices, estimates, forward-looking statements, and other information contained herein have been obtained from sources believed to be reliable, but no guarantee is given as to their accuracy or completeness. All expressions of opinion are subject to change without notice.

Jim Welsh is a registered representative of ALPS Distributors, Inc.

Forward Funds are distributed by Forward Securities, LLC.

© 2014 Forward Management, LLC. All rights reserved.

: FSD000430 013015