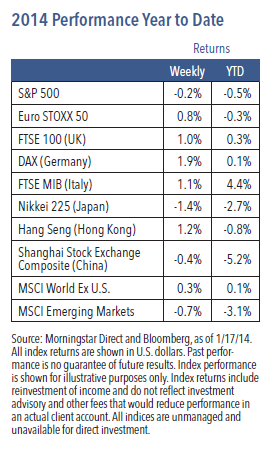

U.S. equity performance was mixed last week, as the S&P 500 recovered from Monday’s sell-off that was the largest one-day decline since early November.1 Economic data was mostly in line or slightly better than expected, following the disappointing December unemployment report. Corporate earnings drove much of the price action. Bank earnings were fairly well received but did not always translate to good performance since the stocks ran up earlier. Negative guidance trends remain an overhang, particularly for retail.

Less Fear and More Confidence Should Begin to Emerge

Last year’s rally in risk assets and losses in safe assets were driven by a process of fading fear. Market views on growth did not improve, but the downside fears that were present early in the year — European implosion, Chinese hard landing and U.S. fiscal crisis — did not materialize.

Entering 2014, investors do not seem as concerned about downside risks, but they have started worrying about the upside on growth. This absence of confidence leads into our theme of less fear and more confidence. Many investors believe the market is overheated as estimates move downward. We perceive it is only a matter of time before earnings growth accelerates and other coincident and lagging indicators show improvement. We are not bothered by the end of Federal Reserve (Fed) bond purchases, potentially weaker fourth quarter 2013 earnings or the possibility of rising U.S. Treasury bond yields. Rising interest rates are normal during economic expansion, and while there is a good chance rates will move higher in 2014, we do not anticipate a hurdle for equity valuations. We believe stock prices can move higher, but only in the context of improved earnings growth. Recent equity market volatility is stemming from the Fed’s intention to eliminate bond purchases by the end of the year, and investors are in search of a new guidepost. As a result, investors may be overreacting to new economic or fundamental data. Our constructive stance remains anchored by accelerating earnings per share growth, positive relative value for equities versus bonds and also the potential for an upside economic surprise.

Weekly Top Themes

1. Retail sales in December increased 4.1% versus December 2012.2 Total sales

for the 12 months of 2013 rose 4.2% over 2012. These figures indicate the holiday season was relatively healthy.

2. Core consumer prices continued to rise at a subdued rate in December.3 Also, initial jobless claims were roughly in line with expectations, but continuing jobless claims unexpectedly turned up.4

3. There is a lack of hard evidence of a pickup in bank lending growth. The macro hopes of a sustained acceleration in the U.S. rests in part on an increase in capex as well as hourly earnings growth.

4. Lawmakers passed a bill to fund the government for the rest of the fiscal year, and the Senate rejected a plan to extend unemployment benefits for three months. The only budget issue that could be a challenge is the debt ceiling, however, we think the odds are low that it would disrupt the economy or markets.

5. U.S. inflation is likely to remain low, which provides important support for growth. Restraints on inflation include moderate economic growth, the rising dollar, high unemployment, low unit labor cost gains and increased use of low cost natural gas.

The Big Picture

Global markets continue to struggle with mixed economic growth data and concerns over the path and impact of global long interest rates. S&P 500 earnings releases over the coming weeks will give a better view of how companies performed at the end of 2013 and help handicap the 2014 outlook. We continue to expect U.S. and global GDP growth to improve this year and global markets to end higher. Our target for the S&P 500 is 1950, and we expect U.S. leadership for at least the first half of the year. There are probably investors that want to own more equities and therefore market corrections have been reasonably short-lived. We do not expect potential for a huge correction or bear market, despite the re-rating that has occurred largely because policymakers are still trying to stimulate growth. In our view, the forward path of U.S. equities will depend mostly on the trajectory of profits rather than further expansion in valuation.

1 Source: Morningstar Direct, as of 1/17/14. 2 Source: U.S. Census Bureau, U.S. Department of Commerce, “Advance Monthly Sales for Retail and Food Services December 2013,” January 14, 2014, http://www.census.gov/retail/. 3 Source: Bureau of Labor Statistics, “Consumer Price Index Summary – December 2013,” January 16, 2014, http://www.bls.gov/news.release/cpi.nr0.htm. 4 Source:

U.S. Department of Commerce, “Unemployment Insurance Weekly Claims Report,” January 16, 2014, http://www.dol.gov/opa/media/press/eta/ui/current.htm.

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. Euro STOXX 50 Index is Europe’s leading Blue-chip index for the Eurozone and covers 50 stocks from 12 Eurozone countries. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock

Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. FTSE MIB Index is an index of the 40 most liquid and capitalized stocks listed on the Borsa Italiana. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Non- investment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

GPE-BDCOMM2-0114P

© Nuveen Asset Management