Does the title sound familiar? Think feral instead of frugal, and William Blake’s “Tyger, Tyger, burning bright” may start to flicker between the synapses of memory and an English lit class you once soldiered through. But even if you haven’t read “The Tyger”, its theme is aptly captured in the opening line and its image of a big flaming kitty cat. Essentially, Blake saw reality in duality: To appreciate the ferocious feline in all its glory is to come face to face with the same force that created “The Lamb”, another entry in the poet’s Songs of Innocence and of Experience. Strip out the weighty meaning-of-life implications and you’re left with an all-encompassing philosophy that truth lies in contraries. And that’s a useful concept to consider in this age of thrift we find ourselves in at the start of 2014, six years removed from the excesses of yesteryear.

In economic terms, excess spending must equal excess saving; ergo, the debt-fueled over-consumption in the U.S., Europe and Japan leading up to 2008 could not have existed without the contrary force of savings-based under-consumption and excess production somewhere else in the world (in this case, China). Back in 2005, Ben Bernanke — then a Fed governor — dubbed the consequence of this duality a “global savings glut”, as the emerging world pulled in the deluge of developed world excesses and spit them back in the form of excess savings invested in safe havens like U.S. Treasuries and German Bunds. The savings glut continued to expand and, in fact, intensified after 2008, as U.S. and developed market over-consumers shed their excesses through deleveraging and increased savings, governments implemented painful austerity measures and the corporate sector hoarded cash.

The global impulse to save has kept interest rates low, fixed income assets in limited supply and inflationary pressures subdued. Meanwhile, central banks — through quantitative easing and other engineered phenomena designed to keep interest rates low — have worked overtime to equilibrate the imbalance by redirecting excess savings into consumption and investment in the hopes of sparking real economic growth and avoiding the dreaded “D” word (deflation). Even now, with private sector deleveraging well underway, growth expectations in the developed world showing signs of sustainable life as the era of austerity comes to a close, and central banks like the Fed beginning to close the liquidity spigot, the propensity to save continues to burn brighter than the propensity to consume.

As Blake suggested, strength cannot exist without the contrary force of weakness; as such, the preponderance of thrift will continue to be reflected in the tenor of our macroeconomic views: subdued U.S. and global growth, muted inflationary pressures, gradually rising interest rates and the continued retrenchment of emerging markets.

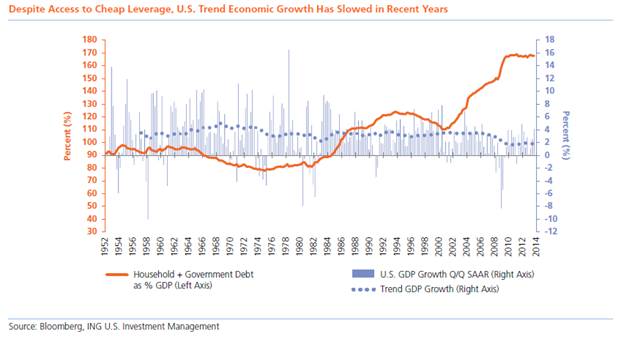

U.S.: Near-Term Growth to Exceed Slower Trend Pace

The upward trend in leading economic indicators — such as strong PMI data and a shrinking trade deficit — suggests positive U.S. growth momentum will continue in 2014. The virtuous and self-sustaining U.S. residential and commercial real estate recoveries will drive stronger construction activity and household wealth. With a bipartisan budget agreement in place and the Washington brinksmanship fad apparently now passé, fiscal drag is on track to decline by approximately 1% in 2014 relative to 2013.

These and other cyclical tailwinds are likely to propel U.S. economic growth beyond its long-term trend during 2014; however, we believe the trend growth hurdle is lower than widely perceived. While the unemployment rate continues to move lower, it is largely a consequence of a structural decline in labor force participation; since 2001, the labor force participation rate has declined by more than 4% as an aging population sends workers into retirement or disability at ever-higher rates. Coupled with the deleveraging of U.S. households, the desire and need to save is bolstered, thus lowering the speed limit on U.S. economic growth in the coming years.

Global: A Less-Austere Europe to Contribute to Global Growth

Europe, like the U.S., will benefit from highly accommodative monetary policy through an increasingly dovish European Central Bank, as reinforced by the ECB’s latest rate cut and gestures toward the possibility of Fed-style bond buying should deflationary risks intensify. December’s 0.8% euro zone inflation print gives the ECB no reason to change course. Positive fiscal impulse (i.e., decreasing drag) in Europe is on track to deliver similar benefits as in the U.S. European PMIs have continued to improve, which has had a lagged but positive effect on Europe’s trading partners, including emerging market economies in Asia and EMEA.

While Europe has thus far faced the most painful adjustment to the post-crisis unwind of global imbalances, success stories of improved competitiveness and fiscal adjustment are becoming more plentiful, making the euro zone a less-unhealthy contributor to the global economy. Structurally, however, Europe faces a more advanced demographic trend toward retirement and declining productivity than does the U.S. So while we expect Europe to contribute positively to global growth, like the U.S., its contribution will likely be subdued.

U.S.: Fed Will Stay Committed to Forward Guidance, ZIRP

As mentioned, despite our expectation of positive cyclical growth for the U.S. and Europe, highly accommodative monetary policy in the U.S. under Ben Bernanke’s successor Janet Yellen is likely to continue, as longer-term structural concerns like trend growth and the natural rate of unemployment should afford the Fed plenty of latitude in setting policy. Therefore, the path to higher interest rates as engineered by the Fed should be gradual. Moreover, Yellen’s commitment to forward guidance on interest rates will keep policy dovish despite reduced asset purchases. While tapering has pulled forward the market’s expectation of when the Fed will begin to raise the target federal funds rate, the central tendency of interest rates still confirms lower for longer. Therefore, price swings and market gyrations that result from Fed tapering and the market’s tendency to over-interpret Fed messaging will distort valuations and create investment opportunities along the way.

U.S.: Inflationary Pressures Will Remain Subdued

That said, the era of zero interest rates in the U.S. does have an expiration date, even if its timing is still unknown. The longer the Fed elects to keep short-term rates at zero, the sharper the eventual correction could be, particularly if the market’s faith in the Fed’s ability to manage the transition turns out unfounded and the cyclical tailwinds pushing growth beyond its now-reduced speed limit prove stronger than expected. But while an unexpected emergence of inflationary pressures could challenge the foundational assumptions of both current Fed policy and market consensus, we expect inflationary pressures will remain subdued given declining labor force participation. It is difficult to achieve above-target inflation without wage inflation, and both limited wage growth and contained CPI indicate that inflation is under control. Increases in hourly earnings remain very modest, and employee expectations of raises are low. Food and energy commodities have cheapened, reducing inflation in necessity items. Longer-term inflation expectations also remain well-contained.

U.S.: Economic Divergence Is Peaking

Much of the explanation for limited wage growth can be attributed to the economic divergence caused by the Fed’s attempt to spur economic growth and demand. Easy monetary policy has engendered corporate margin expansion and a wealth effect of appreciating real and financial assets, which has driven most of the growth in consumption — but only for those who own such assets. It’s tough for the shrinking middle class to justify buying an iPad when the primary concern is putting food on the table and maybe saving for the future by funding the 529 and 401k plans.

This growing income divide has propelled government approval ratings into the doldrums, and while the late-2013 budget agreement suggests that political uncertainty and periodic episodes of acute brinksmanship are in decline, this economic divergence — if uncorrected — may add to the political strain around entitlement questions. Consumer and business skepticism about the government’s effectiveness in these areas could further impede economic growth and is a key political risk to monitor. Of course, if the Fed’s commitment to dovish policy proves to be a mistake and cyclical tailwinds push economic growth well beyond its trend pace, investors who closely high-frequency inflation signals closely could be richly rewarded.

Global: EM Still Has a Long Way to Go

Emerging markets — which once benefitted from excess consumption in developed economies — will continue to feel the effects of a reduced propensity to consume and structural declines in their developed market counterparts, resulting in further retrenchment. Chinese growth and the positive uptrend for the U.S. and Europe is supportive of emerging markets, but fundamental vulnerabilities and the reduction in Fed asset purchases will undermine returns, particularly in local-currency investments. Outflows from both hard and local currency emerging market funds have been considerable, and idiosyncratic political situations (for example, Ukraine, Venezuela, Thailand) have generated further volatility.

Countries bedeviled by weak current accounts and troubled fiscal situations have suffered disproportionately during the latest retrenchment. Emerging market countries must undergo significant structural reform and consolidation in order to evolve from a mercantilist, export-based culture of net savers with an overabundance of labor and a fixed exchange-rate policy — such as China — into a fully industrialized consumer-based nation. This process does not happen overnight.

Outlook: Appetite for Risk Assets Should Remain in Favor

In the meantime, as investors ponder burning issues like the slaughter of their fixed income portfolios by rising interest rates, we offer the following advice: Easy, Tyger. While we must appreciate the possibility that the impetus for higher rates is stronger than central banks are forecasting, we cannot underappreciate the realities of thrift caused by the excesses of yesteryear. The global savings glut created by those excesses burns brighter today than it did prior to 2008, as deleveraging and unfavorable demographic trends in the developed world have perpetuated the bias toward under-consumption. To counteract these forces, central banks globally will continue to implement extraordinary measures even as the U.S. tapers its asset purchases, which should keep disinflationary pressures at bay. The extremes engineered by central banks have contributed to financial repression by depressing the real yields of sovereign bonds, moving many valuations of income-generating assets from cheap to fair. While the experience of 2008 tells us that these richer valuations can’t last forever as the dueling forces that created the global savings glut slowly begin to reverse — particularly as emerging markets continue to develop — we expect valuations to become significantly richer in 2014 and for the foreseeable future.

In this prolonged environment of global thrift, we continue to favor the brightest economic recovery story since 2008 in the U.S. While expansion will likely be lower than widely assumed, the world’s largest economy is poised to generate 2014 growth in excess of the long-term trend. Combined with improvements in Europe and China, this should help sustain a healthy appetite for risky assets. While QE gyrations may result in volatility, the distinction between tapering and rate hikes will keep higher-yielding “carry” assets well-supported. Our bias is for domestic credit instruments such as high yield bonds and floating-rate bank loans as well as sectors tied to the real estate recovery such as commercial mortgage-backed securities.

This commentary has been prepared by ING Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults (5) changes in laws and regulations and (6) changes in the policies of governments and/or regulatory authorities.

The opinions, views and information expressed in this commentary regarding holdings are subject to change without notice. The information provided regarding holdings is not a recommendation to buy or sell any security. Fund holdings are fluid and are subject to daily change based on market conditions and other factors. Past performance is no guarantee of future results.

© 2014 ING Investments Distributor, LLC • 230 Park Avenue, New York, NY 10169

CID 8416