Bernanke’s Final FOMC Leaves Emerging Markets in a Bind

Equity markets closed out a challenging January with further losses. For the week, the S&P 500 Index was down 0.4% and the DJIA lost 1.1%. During the full month, the S&P was 3.6% lower and the DJIA is off by 5.3%.

Economic data spanned a wide range of news in the U.S., and it proved to be a largely mixed week. But, markets were focused on a mix of earnings reports and developments in emerging markets – both of which introduced volatility throughout the week.

Within the U.S., the key focal point was the latest Fed meeting, which saw a further $10 billion reduction in asset purchases. At the current rate, the Fed will continue purchasing $65 billion in assets per month. The Fed noted that economic activity “picked up in recent quarters,” and without a significant change in growth rate, every expectation is for the Fed to keep reducing asset purchases at a measured pace through the remainder of this year.

Source: Econoday

Somewhat confirming the Fed’s assessment was fourth quarter gross domestic product (GDP), which rose to 3.2% annualized. That is down slightly from the 4.1% growth rate in the fourth quarter, but the second half of the year proved to be one of the strongest periods of growth for the economy in recent years. Economists were split on the underlying health of the data, noting that consumption accelerated to 3.3%, but inventory accumulation added 0.4% to overall GDP. Inventory build will reverse in the quarters ahead and could act as a minor headwind to GDP.

On Friday, a more detailed review of personal consumption showed consumers funding spending through a drawdown in savings accounts. The personal savings rate fell below 4% and neared the lowest levels since 2008. Such low levels of savings are unsustainable and should temper consumption growth somewhat in 2014.

Source: Haver Analytics

There was litany of activity in emerging markets last week, as they struggled to contain budding imbalances and fears of slowing growth prospects. Pinpointing the exact pressure point in EM is difficult, but China deserves an outsized portion of the blame. Recent economic data showed a weaker manufacturing sector, and there are serious concerns about the health of the financial sector in China.

Despite those fears, many countries were forced to act in an out of character manner last week. The Reserve Bank of India unexpectedly raised rates by 0.25% to 8.0% to head off inflation concerns. The central bank in Turkey made the massive aggressive maneuver last week, moving short-term rates from 4.5% to 10%. Finally, countries such as South Africa, Argentina, Costa Rica, Russia, and Croatia intervened in currency markets, or made announcements that such options were readily available.

The final bit of news the market was trying to digest was corporate earnings. Through the first few weeks, 70% of companies are beating earnings forecast, albeit many of those forecasts were revised down leading into the earnings cycle. The news has not been uniformly positive however, with large names like Amazon and ExxonMobil missing forecasts, while Target and Walmart preannounced negative warnings. In aggregate, the current earnings growth rate is 7.9% for the fourth quarter, which would be the strongest rate since 2012. That is slightly distorted by financials, though, and excluding financials earnings, the growth rate slips to 4.9%.

Source: FactSet

Earnings reports will play another prominent role in markets this week. Another 93 companies in the S&P 500 Index are scheduled to report, including popular names such as General Motors, LinkedIn, Kellogg, Disney, Aflac, Merck, and Yum! Brands.

Investors Should Focus on Wages, Not Jobs

This Friday investors receive the first official labor market report of 2014. Following a highly disappointing jobs figure in December, many market participants hope to see a rebound – particularly one that will help justify the Fed’s decision last week to continue tapering its asset purchases.

However, investors may find it more appropriate at this time to shift their focus within labor market data to something that may ultimately prove more meaningful: wages. While the public at large hinges their economic opinion on the unemployment rate and nonfarm payroll reports, there are reasons to question the relevance of that data.

By now, most market participants are aware of the poor quality of the improvement in those respective reports. The unemployment rate has been distorted by a generational shift in labor force participation (whereby discouraged workers dropped out of the labor force, artificially lowering the headline measure). That may only get worse this year, following the elimination of extended unemployment benefits at year-end. According to Bloomberg Research, that could add as many as 1.3 million people to the 7 million that have already exited the work force.

Source: Bloomberg

Meanwhile gains in nonfarm payrolls have largely occurred in low wage industries like temporary help, restaurants, and clothing retailers. The establishment survey also does not distinguish between part-time and full-time workers, placing another blemish on an otherwise steady pace of job gains.

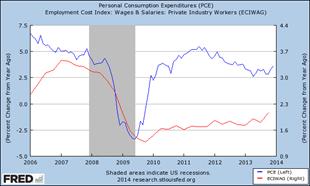

Wages, on the other hand, provide a clearer view of these shortcomings in the labor market. Wage growth has been stagnant since the financial crisis, as evidenced by measures such as the Employment Cost Index and Average Hourly Earnings produced by the Labor Department. Some observers may find this pattern more reflective of reality in recent years. And an uptick may better correlate to improvement in consumption habits, which is what ultimately drives GDP; recent strength in personal consumption expenditures coincided with the first meaningful move higher in wages in some time.

Source: St. Louis Fed

In some ways, the recent improvement in wage growth may actually be the best sign that labor markets are tracking towards normalcy. According to the Federal Reserve Bank of San Francisco, pent-up wage cuts during the recession caused by “downward nominal wage rigidity” (i.e. workers’ unwillingness to accept wage reductions) causes wage growth to slow even after the economy recovers and the unemployment rate reaches more normal levels. With the unemployment gap narrowing (now just over 1% as of year-end 2013), the Phillips curve suggests that we may be near an inflection point for wage growth.

Source: FRBSF

According to research firm Capital Economics, there are several other reasons to believe that wage growth could see a continued turnaround this year. The National Federation of Independent Businesses (NFIB), for example, notes that small businesses having difficulty finding qualified candidates for open jobs is at a five-year high. In the Labor Department’s Job Openings & Labor Turnover Survey (JOLTS) data, the number of job openings and voluntary separations are increasing, suggesting that overall labor market “churn” is picking up. Both of these developments should contribute to higher incomes for jobholders.

Source: NFIB

For investors, a pickup in wage growth carries with it a few very important implications, with the first being derivative inflationary pressures. Although inflation has been extraordinarily tame in recent years, the Fed would likely move quickly to quell any increase with a tighter policy prescription, particularly given the immense levels of liquidity in the financial system. Second, while corporate profits have enjoyed record margins amid cost control, wage improvement will certainly start to eat into those profits.

This could cause some near-term pressure on equity markets as both accommodative policy and strong earnings have been supportive factors of the post-GFC bull market. Ultimately, however, a healthier labor market with more consistent income growth should lead to a more sustainable and organically driven expansion for both the economy and financial markets.

The Week Ahead

Economic data is limited, but top heavy, this week, with the ISM manufacturing index and the jobs report due for release. ISM’s sister index, the non-manufacturing index, is also slated for publication.

Central bank activity picks up this week, with policy decisions looming from both the European Central Bank and Bank of England. Recent disinflation in Europe has many observers expecting that the ECB will cut their benchmark interest rate to 10 bps from 25 bps. Analysts do not anticipate policy changes from the BoE. Other rate decisions are due from Romania, Australia, Poland, the Philippines, and Czech Republic. Some of these meetings may garner greater attention given recent instability in emerging markets.

About Fortigent

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value

© Fortigent