There’s no ignoring broad market trends when investing in equities, even for bottom-up stock investors like us. Among the factors we consider when researching a stock is whether there’s a supportive macroeconomic backdrop. For 2014, one of the positive longer-term trends we see is a strong environment for consumers.

Many Factors are Encouraging

There is no single data point giving us confidence in the power of the consumer, but a number of factors combined suggest that conditions are supportive of greater discretionary spending. The first is modest, but generally steady, improvement in employment data. Payrolls are up, new unemployment claims are down, and—perhaps most notably—the ranks of the long-term unemployed appear to be thinning.

U.S. Unemployment Rate—Unemployed for 27 Weeks or Longer

Source: ISI Group, 1/1972 to 11/2013

Are things perfect? No—after a punishing recession it’s not entirely surprising that employers are being deliberate in repopulating their ranks. But the bottom line is, more people are working now than were a few years ago, pumping income into the economy.

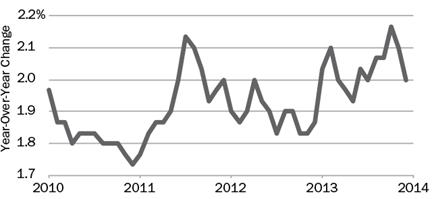

Those workers are making more money, too. While nominal wage gains haven’t been prodigious, in conjunction with low—and decelerating—inflation they have been sufficient to produce a meaningful increase in real terms.

U.S. Real Average Hourly Earnings (3 Month Average)

Source: Cornerstone Macro, LP and Bureau of Labor Statistics 11/1/2009 to 12/31/2013

In the current environment, even small incremental gains can make a noticeable difference.

Higher Net Worth Fuels Spending

At the same time that employment and real wages have been staging a moderate comeback, the housing market has continued to hold firm, and equity markets have posted outstanding returns. The result? Record-high levels of personal net worth. This helps make people more comfortable taking their discretionary income and spending some of it instead of parking it all in the bank.

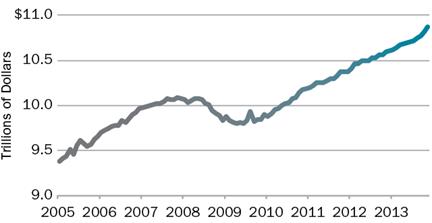

Personal consumption expenditures have been on a solid upward path since the Great Recession of 2008-2009. The pace has shown signs of accelerating more recently, suggesting that the trend could persist.

U.S. Real Personal Consumption Expenditures

Source: ISI Group, 1/2005 to 11/2013

There’s more than one way consumers help boost stocks. The first is fairly obvious: higher spending can drive corporate sales and earnings. When earnings rise, a company’s share price can appreciate without its price/earnings ratio (P/E) going up at all. Stocks can thus remain at relatively moderate valuations even as shareholders in consumer-driven areas like retailers, clothing manufacturers, and restaurants experience healthy total returns.

The impact of consumers resonates far beyond the mall, however. Automakers are moving more cars off the lot as drivers have become more comfortable taking on new car payments. Financials stocks benefit not only from those loans, but also from credit-card spending and other lending activity. Information Technology companies are set to sell more of the chips, processors, and software that play an ever-larger role in virtually every product people buy, from cars to phones to televisions.

Equities Appeal to Confident Consumers

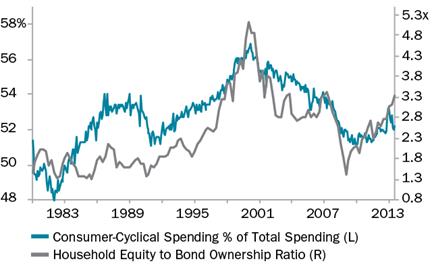

There’s another way that stocks can benefit. The same positive sentiment that drives consumer spending also gives them a greater appetite for equity investing. When households begin to run a surplus, it’s generally easier for them to accept stocks’ greater level of volatility in pursuit of higher gains.

Stock Ownership Increases When Consumer Cyclical Spending Increases

Source: Cornerstone Macro, LP, Bureau of Economic Analysis, and Board of Governors of the Federal Reserve System; Household equity to bond Ownership, quarterly 1/1/1980 to 7/1/2013; Consumer cyclical spending, monthly 1/31/1980 to 7/31/2013

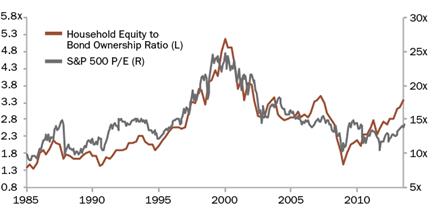

It may be common to think that only institutional investors, who often shift assets in large blocks, drive the markets. But in reality individual investors’ ownership of equities is also an important force behind the market’s P/E.

Households’ Ownership of Equity is a Key Determinant of the Market’s P/E

Source: Cornerstone Macro, LP, Board of Governors of the Federal Reserve System, and Thompson Financial’s I/B/E/S; Household equity to bond ownership, quarterly 1/1/1985 to 7/1/2013; S&P 500 P/E, monthly 1/31/1985 to 7/31/2013.

S&P 500 P/E ratio represents the next 12 months forward.

Past performance does not guarantee future results.

Household appetite for equities provides another avenue for price appreciation, this time in the form of multiple expansion. Strong demand for stocks makes investors willing to pay more for each dollar of earnings they produce, helping to make higher price multiples sustainable.

Looking Ahead in a Changing Market

As equity investors, we have no aversion to a rising market. With our contrarian, value approach, however, it’s in our DNA to become cautious when we see valuations expanding. Something that gave us concern in 2013 was that many stocks produced excess returns, despite having little or no earnings and heavy levels of debt.

We think the market drivers going forward could be quite different from what we’ve seen recently. In our view, companies that are able to demonstrate real financial strength and produce robust earnings—supported by healthy levels of consumer spending—are likely to be more in favor with the market, while highly leveraged companies that cannot generate a profit may lag behind.

We don’t try to call the market’s direction. But decades of experience applying our fundamental, bottom-up investment process have taught us to separate the companies that are experiencing justifiable appreciation because of their business success, from those that are becoming overvalued in the wake of short-term market trends. In the process, investors have the opportunity not only to participate in the market’s upside, but also to mitigate downside risk when the market tides shift.

Past performance does not guarantee future results.

Economic predictions are based on estimates and are subject to change.

Ted Baszler, CFA, CPA, is Vice President and Portfolio Manager for the Select Value Fund. He is also Portfolio Manager for three separately managed account strategies: Opportunistic Value Equity, Mid Cap Value, and Core Plus. He has 22 years of industry experience, 19 at Heartland.

The statements and opinions expressed in this article are those of the author. Any discussion of investments and investment strategies represents the portfolio manager’s views when presented, and are subject to change without notice. There is no guarantee that any particular investment strategy will be successful.

Heartland Advisors considers large-cap companies to be larger than $10 billion in market cap, mid-cap companies to be between $2 billion and $10 billion, small-cap companies to be between $300 million and $2 billion, and micro-cap companies to be less than $300 million. The above breakdown does not include short-term investments.

Cyclical Spending is composed of U.S. Total Consumption Excluding Food, Energy, Housing, Medical. Cyclical Stocks cover Basic Materials, Capital Goods, Communications, Consumer Cyclical, Energy, Financial, Health Care, Technology, and Transportation which tend to react to a variety of market conditions that can send them up or down and often relate to business cycles. Household Equity to Bond Ownership Ratio is represented by data series published by the Board of Governors of the Federal Reserve System and is calculated as the sum of Corporate Equities held by Households, Personal Trusts, and Nonprofit Organizations and Mutual Fund Shares held by Households, Personal Trusts, and Nonprofit Organizations divided by Credit Market Instruments held by Households, Personal Trusts, and Nonprofit Organizations. Price/Earnings Ratio (P/E) of a stock is calculated by dividing the current price of the stock by its trailing or its forward 12 months’ earnings per share. S&P 500 Index is an index of 500 U.S. stocks chosen for market size, liquidity and industry group representation and is a widely used U.S. equity benchmark. All indices are unmanaged. It is not possible to invest directly in an index.

Separately managed accounts and related investment advisory services are provided by Heartland Advisors, Inc., a federally registered investment advisor. ALPS Distributors, Inc. is not affiliated with Heartland Advisors. The Heartland Funds are distributed by ALPS Distributors, Inc. Ted Baszler is a registered representative of ALPS, Distributors, Inc.

CFA is a trademark owned by the CFA Institute.

2014054

© Heartland Advisors