U.S. equities closed with modest gains last week, as the S&P 500 overcame Monday’s decline, the largest one-day percentage loss since June 2013.(1) The weaker-than-expected ISM manufacturing and vehicle sales data drove the sell-off on Monday, exacerbating the focus on slowing momentum for the U.S. recovery. The impact of adverse weather complicates the picture. Also, although January non-farm payroll missed expectations, there were more upbeat indications from the household survey.

Anticipate Fluctuations but Stay Focused on Fundamentals

Bear market supporters have been talking about the scenarios of a combination of emerging market weakness and the removal of QE stimulus, and investors seem concerned. As discussed in our 2014 outlook, we expect this to be a volatile year as the environment transitions from one dominated by macro forces to more micro influences. We believe the recent weakness is a normal part of a healthy bull market. Although stocks have rebounded slightly over the last few days, we do not discount the possibility for further softness.

We think this is a correction rather than a more significant symptom for several reasons: U.S. earnings on average are coming in better than expected, U.S. fiscal drag is abating, Europe appears to be strengthening, global monetary policy is still broadly accommodative, inflation and bond yields are relatively low and short-term equity fundamentals are fairly strong and improving.

Weekly Top Themes

1. The January ISM Manufacturing survey declined from 56.5 to 51.3. (2) This is only the fourth time in the past 20 years that there has been a decrease of more than 5 points.

2. Payroll employment rose by a disappointing 113,000 in January, after weatherrelated weakness in December. (3) However, more encouraging elements surfaced this month as manufacturing job growth reaccelerated, business services recovered to near the recent trend and earnings and hours were both stronger. Also, the unemployment rate fell to 6.6%, the lowest level since October 2008.

3. Although it may be early to suggest an inflection point in sales and earnings growth, the trend may have improved over the second half of 2013. (4) 4Q13 earnings growth is on track to be the best quarter in two years as margins remain solid.

4. With the S&P 500 decline of roughly 6% since mid-January, about 50% of the companies experienced a decline of more than 10%. (5) We expect a choppy, bottoming process for equity markets.

5. In every mid-term election year since 1962, the S&P 500 has experienced an intra-year average decline of 18%. (6) From that intra-year low, the S&P 500 has increased every time in the following 12 months, with an average gain of 32%.

The Big Picture

Our economic view remains that we are mid-cycle — a transition from easy to less easy monetary policy — with fears receding and confidence increasing. In our opinion, equities remain the asset class to hold. Stocks were overbought at the start of the year and thus were ripe for a pullback after disappointing news. However, the global economy is slowly getting healthier and risk assets should generally grind their way higher over the next 12 months. Many emerging market economies will continue to face a period of adjustment, but underlying economic fundamentals are reasonably solid overall. Therefore, we do not see a threat to the U.S.-led economic recovery in the developed world. We are constructive on the outlook and maintain an overweight stance in equities. Since top and bottom-line performance continues to improve, returns should be solid following the recent pullback. However, equity trends are likely to be choppy, given growth and policy uncertainty. Equities are no longer cheap, but they are also not expensive, and valuation risk is not elevated if the U.S. and global economic recovery stays on track. The United States is in the unique position of having abundant and low cost energy, as well as an underutilized workforce. In the long-run, the improving health of our federal budget, banking system, credit markets and economy should drive stocks higher.

1 Source: Morningstar Direct, as of 2/7/14. 2 Source: January 2014 Manufacturing ISM Report On Business,® February 3, 2014, http://www.ism.ws/ismreport/mfgrob.cfm. 3 Source: Bureau of Labor Statistics, “The Employment Situation – January 2014,” February 7, 2014, http://www.bls.gov/news.release/empsit.nr0.htm. 4 Source: FactSet, “Earnings Insight,” February 7, 2014. 5 Source: MorningstarDirect; Strategas Research Partners, as of 2/7/14. 6 Source: Barrons, “The Stock Market Rises: Trust the Bounce?,” February 4, 2014, http://blogs.barrons.com/stockstowatchtoday/2014/02/04/ the-stock-market-rebound-trust-the-bounce/

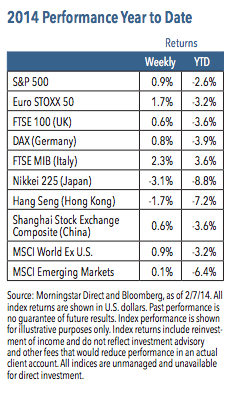

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. Euro STOXX 50 Index is Europe’s leading Blue-chip index for the Eurozone and covers 50 stocks from 12 Eurozone countries. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. FTSE MIB Index is an index of the 40 most liquid and capitalized stocks listed on the Borsa Italiana. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Noninvestment-grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of Nuveen Investments, Inc.

© Nuveen Asset Management