Executive Summary

-

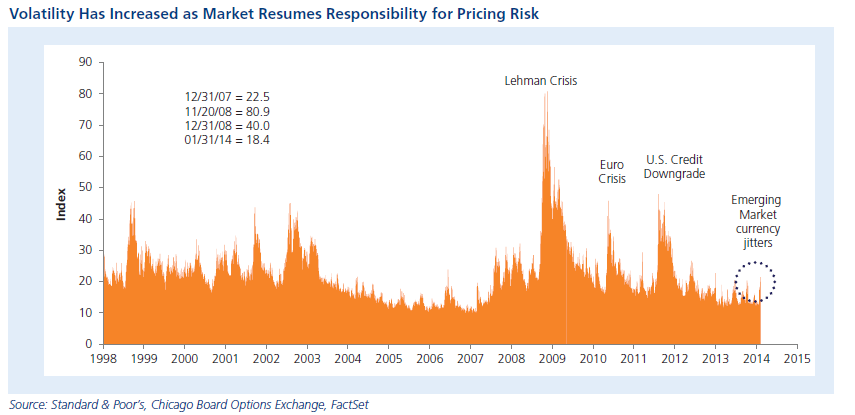

By slowly normalizing policy, the Fed is passing the responsibility of pricing risk back to the markets, resulting in higher volatility.

-

The health of the emerging markets is vital to global growth, as developing countries have doubled their contribution to global GDP over the past decade to nearly 40%.

-

S&P 500 corporations derive half their revenue from overseas; support from global consumerism and manufacturing is on track to continue.

-

Broad global diversification across equity and fixed income markets is the best way to protect against volatility.

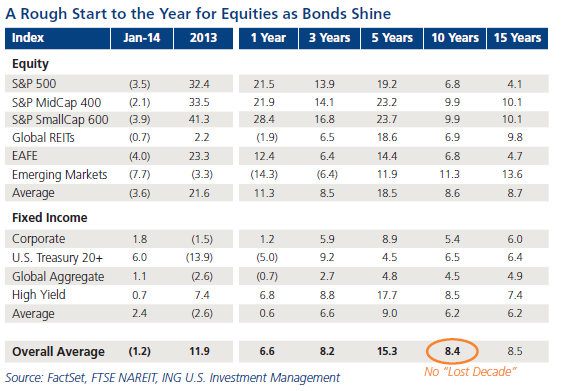

Just as a polar vortex held the nation in its miserably cold grasp for much of January, a combination of emerging market troubles and soft data here at home sent a chill through formerly red-hot equity markets.

Though developed markets at first seemed to shrug off the Federal Reserve’s mid-December announcement that it would begin to curtail its monthly asset purchases, emerging markets — especially those with ballooning current account deficits like Turkey, Argentina and South Africa — soon found themselves under attack. Their fairly illiquid currency, stock and debt markets plummeted in concert, triggering margin calls and sell instructions for a variety of liquid risk instruments, including U.S. equities, throughout January.

February hasn’t been much better thus far. The month led off with a variety of frosty economic data reports for January — including softening ISM Manufacturing data, the first fall in auto sales since September, a drop in pending home sales and a quarterly decline in construction spending — to extend the selloff. The icy statistics apparently were due to, no surprise, cold weather. Though the explanation was clear as ice, investor expectations were high after the strong fourth quarter GDP report; when the data disappointed, investors fled first and asked questions later.

Policy makers may have been late coming around to the idea that it is better to initiate reforms when times are good as opposed to when markets are volatile, but we say better late than never. Turkey, to its credit, implemented a shock-and-awe response to stem the outward flow of its currency, pushing its overnight rate to 12.0% from 7.75%. Now that the curtain of Fed stimulus — both the ongoing liquidity injections of asset purchases along with artificially low rates — is being rolled back, economies worldwide will need to institute pro-growth economic policies such as corporate income tax cuts, deregulation, free trade and others to promote innovation and faster, sustainable growth.

Emerging Markets, Emerging Threats

Here’s a brief summary of how we got to today’s burgeoning currency crisis.

-

In 2009, advanced economies’ GDP fell 3.4% while emerging market economies actually grew 3.1%.

-

From 2010 through 2012 the Fed launched several iterations of quantitative easing to increase liquidity and lower interest rates in the U.S., culminating in a trillion bond-buying binge.

-

These artificially low rates drove investors to hunt for yield in more exotic assets classes, with a good share going into emerging market debt. Concurrently, emerging economies exploded with .46 trillion in foreign direct investment.

-

May 2013 was the first signal of a possible inflection point, as then-Chairman Ben Bernanke announced that the Fed could begin tapering its QE program at any time. The currencies of Russia, Mexico, South Africa, Turkey, Brazil, India and Indonesia fell 3–15% against the U.S. dollar. When the Fed unexpectedly announced in mid- September that it was not yet prepared to taper, the aforementioned currencies rebounded but only slightly.

-

After introducing a billion per month reduction of its quantitative easing program following its December meeting, the Fed lopped another billion from its monthly buying commitment in January, sharpening focus on those emerging markets with high current account deficits. In essence, the Fed is returning the responsibility for pricing assets and efficiently allocating capital back to the markets, where it belongs. Of course, the supply and demand driven market pricing mechanism is not as smoothly effective as Fed proclamations; as such, it’s not surprising that volatility has spiked from a 12 handle to 18 and beyond.

Why is Fed activity having such a profound impact on the emerging markets? Currency movements tend to be poorly understood by the investing public, but a knowledge of this dynamic is integral to an appreciation of the current market malaise.

Basically, as a country’s currency drops (that is, devalues), it raises both the cost of imports and the cost of debt denominated in another currency (emerging markets typically issue a greater amount of debt in such “hard currencies” as the dollar and euro as opposed to their domestic currencies). Countries with large current account deficits (that is, those that import more than they export) are particularly susceptible to currency devaluations, as it forces them to finance their large deficits with a currency that is increasingly worth less. Further, a falling currency conspires to spike inflation throughout an economy and adversely impacts growth. Though central banks often raise interest rates in order to attract capital and thus prop up the local currency, it’s very difficult to counter the forces of a currency crisis once it gains steam.

The Asian currency crisis in 1997 took about a year to hit the developed markets; with emerging markets now a far bigger contributor to global growth, however, the impact of their struggles were felt only a few weeks after concerns first surfaced. Here are the countries most impacted on a year-to-date basis:

-

Argentina. In the most dramatic depreciation since the country’s 2002 financial crisis, the Argentine peso fell 23%. With inflation estimated to be running at 28%, Argentina’s central bank sold peso-denominated notes due in 98 days at an astounding 25.9% to defend its currency.

-

Turkey. After falling 6% in January, the Turkish lira rebounded slightly after the central bank raised interest rates a whopping 425 basis points to 12%.

-

South Africa. South Africa’s rand has fallen to its weakest level since 2008 after declining 7.5% despite the central bank’s 50 bp rate hike to 5.5%.

-

Russia. Despite the ruble falling 7% to a five-year low, Russia’s central bank has declined to intervene.

-

India. The Indian central bank surprised markets by raising rates 25 bps to 8% to fight inflation pressures.

-

Brazil. Despite floundering economic growth, the Brazilian central bank chose to focus on inflation and aggressively raised rates by 50 bps to 10.5%.

Market Fundamentals Remain Intact

While interest rate hikes bolster currencies, they also weigh on economic growth. It is notable that despite the hike in interest rates by many emerging market countries, a number of these currencies remain under pressure, suggesting investors are not convinced enough action has been taken. Even so, market fundamentals continue to march forward.

Earnings are the fundamental driver of equity markets; as such, while the emerging markets are garnering headlines across the globe, it is essential for investors to keep their eyes on the ball. With 55% of the S&P 500 having reported fourth quarter results, year-over-year earnings growth is tracking at 10%, the fastest pace we have seen in almost two years, though this earnings growth has been accompanied by comparatively weaker sales growth of 2.3%. Robust earnings can be found across sectors except energy, which has posted negative growth this far. Should the rest of earnings season hold close to expectations, the S&P 500 will achieve record earnings of 0 per share.

These corporate profits are supported by global consumerism and global manufacturing. Indeed, it is the drive of the global consumer and manufacturing sector that has propelled total global economic output to nearly double over the past decade, from trillion to trillion projected for year-end 2013.

Global Consumer. Despite the harsh weather, U.S. retail sales ticked up 0.2% in December thanks to heavy discounts and abundant promotions; the latest January reading showed aggregate retail sales once again reaching all-time highs. Online sales continue to grab market share and spurred a 2.7% increase in holiday-season sales nationwide and more than compensated for a total retail store traffic decline of 14.6%. Overall 2013 retail sales were up 4.3% over 2012, as the consumer continues to drive the U.S. economy. Meanwhile, China retail sales were up more than 13% for the year, and China has overtaken Japan to become the second largest consumer economy, with .3 trillion in private consumption.

Consumers outside of the largest economies are expected to contribute as well. Russia, still an emerging market, is opening the most expensive Winter Olympics ever in Sochi. Brazil will host the soccer World Cup in 2014 and the 2016 Summer Olympics. Though still categorized as emerging markets, countries like these are packing a bigger punch than their sizes might suggest.

Global Manufacturing. The latest poor PMI numbers from the U.S. spooked markets, coming as they did directly on the heels of somewhat softer China manufacturing data. However, both of these metrics remain in expansion mode, and there have been many bright spots in global manufacturing. The U.K., for example, has continually posted manufacturing numbers suggestive of robust growth, and euro zone data indicate renewed economic expansion.

Here in the U.S., the bitter cold sent natural gas prices spiking over .00/btu for the first time since 2010, but manufacturing continues to gain footing given the relative natural gas price advantage the U.S. enjoys over other manufacturing countries. Since 2010, the U.S. has regained a net 568,000 factory jobs, and they are primarily more skilled and higher paying positions. North Dakota is a good example of the U.S. manufacturing renaissance; in the last six years, the state’s per capita income has jumped to sixth in the nation from 38th, with the gains centered on its natural gas extraction industry. The manufacturing rebirth is also evident in trade data, with the most recent report showing the trade deficit falling to its lowest level since 2009.

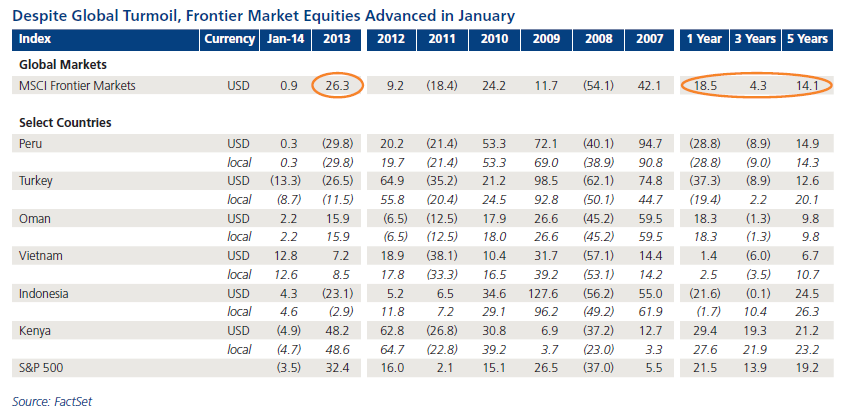

Frontier Markets Offer Growth, Attractive Diversification

While it’s easy to paint all of the emerging markets with a broad brush, investors would be wise to bifurcate them into emerging and frontier markets. Of the two, we prefer the frontier markets; not only are they one of our “tectonic shifts” and catalysts for growth in the broadening global expansion, they have largely avoided the adverse impacts of the carry-trade currently bedeviling much of the emerging world.

After a 2.3% decline in 2013, emerging market equities have been punished even more soundly in 2014, down 6.5% in January. Frontier markets, however, are a completely different story; the MSCI Frontier Market Index returned 26.3% for 2013 and was up 0.9% in January amid all of the equity market turmoil. These thinly traded markets are useful diversifiers, as many have managed to stay above the fray and avoid currency pressures. The frontier markets will continue to offer high growth potential and will also fuel global growth as they continue to evolve and mature.

Take Vietnam, which along with Peru, Indonesia, Oman, Turkey and sub-Saharan Africa comprises our PIVOTS frontier markets story. The country has a current account surplus, expected GDP growth of 5.8% for 2014, forecast industrial production growth increase to 5.9% and an inflation target below 7%. And Vietnam equities were up more than 12% in January.

Conclusion

If the reaction of global equities to recent emerging market currency issues is any indication — the Dow Jones Industrial Average dropped more than 5% in January, for example, while Japan’s Nikkei 225 shed nearly 7% in yen terms — the so-called developing countries are no longer marginal players on the world stage. Economic output data also back this up, as emerging and frontier markets now contribute nearly 40% to global GDP, double the share from a decade ago. Meanwhile, January’s market underscored the “folly of gaming diversification”. Investors that sold bonds in fear of rising rates missed the point of fixed income exposure (namely, portfolio downside protection), as bonds significantly outperformed equities when stock markets caught a chill during the month.

This commentary has been prepared by ING U.S. Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults (5) changes in laws and regulations and (6) changes in the policies of governments and/or regulatory authorities.

The opinions, views and information expressed in this commentary regarding holdings are subject to change without notice. The information provided regarding holdings is not a recommendation to buy or sell any security. Fund holdings are fluid and are subject to daily change based on market conditions and other factors.

Past performance is no guarantee of future results.

© 2014 ING Investments Distributor, LLC • 230 Park Avenue, New York, NY 10169

CID 8537