MANUFACTURING REPORT OVERSHADOWS IMPROVING CONSUMER DATA

Stocks were modestly positive last week following three straight weeks of negative performance. Markets crawled back following an ugly Monday in which the S&P 500 suffered its worst loss in more than seven months. For the week, the S&P rose 0.9% while the Dow Jones Industrial Average added 0.7%.

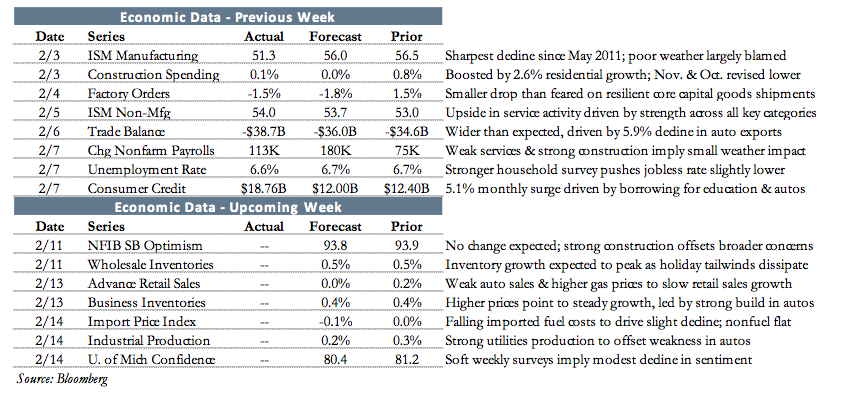

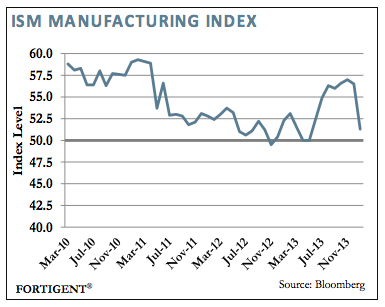

Economic data was mixed last week, with the Institute for Supply Management’s (ISM) Manufacturing Index capturing most of the negative attention. The report’s surprising decline on Monday was the catalyst for market losses.

The ISM Manufacturing Index slipped more than five points to 51.3, just over the expansion/contraction demarcation line. Economists were expecting a far more robust 56.0 figure. Weakness was broad based, as eight of the 10 component measures weakened in January. In what is always the most closely watched part of the PMI, new orders were shockingly bad. That measure plummeted 13.2 points to 51.2.

If there is any solace to be had from this report, ISM noted that a number of survey respondents cited poor weather as an inhibiting factor during the month. A normalization of business activity in the manufacturing sector could lead to a rebound in next month’s reading.

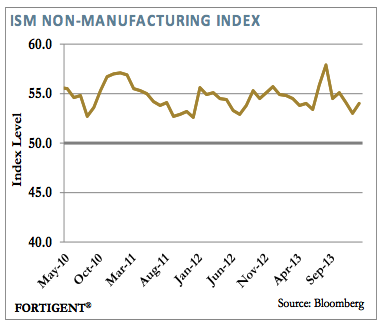

ISM’s sister report on the service sector was more encouraging, as the Non-Manufacturing Index moved slightly higher to 54.0. Unlike the manufacturing report, eight of the 10 components were positive, led by a two-point gain in business activity. New orders improved marginally, but are currently teetering on the edge of contraction at just 50.9. The latter measure has been in expansionary territory for 54 straight months.

The ISM reports paint a picture largely consistent with what most market participants have gotten used to: a fair, but not spectacular state of the US economy. Despite the manufacturing index’s lunge, it remains above the 50 line and indicates that the sector is growing.

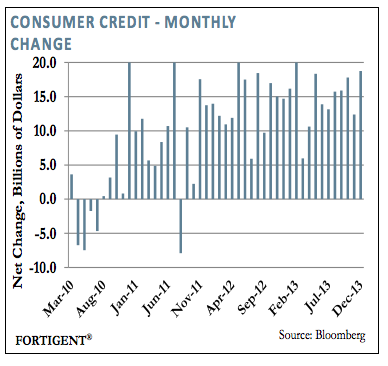

Somewhat buried under the headlines Friday was a sharp increase in consumer credit to .8 billion. This was far in excess of the expected .0 billion figure, but more encouraging still was a .0 billion increase in revolving credit (i.e. credit cards). According to research firm Econoday, that is the third largest increase of the economic recovery.

Previous consumer data, now combined with December’s credit picture, suggests a somewhat healthier consumer than the image portrayed during the holiday retail season. Some have postulated holiday sales were inhibited by cold weather and a shorter-than-typical holiday season, which may account for some of the discrepancy. Whatever the case, improvement in this portion of the economy will be key for GDP expansion in the quarters ahead as fiscal consolidation is likely to be a continued drag on growth.

WAS THE LABOR REPORT POSITIVE, OR NEGATIVE, ANYONE?

For the second time in as many months, the nonfarm payroll report led to a disappointing headline result. Regardless, equity markets found reason to be happy and raced to a greater than 1% gain. By some accounts, the labor report was a slight dud, but there was some manner of positive news in the underlying data.

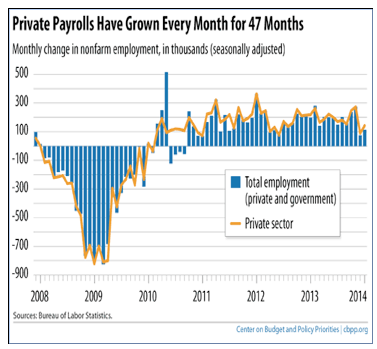

According the Bureau of Labor Statistics (BLS), the economy added 113,000 jobs in January, following an upwardly revised 75,000 jobs in December. The unemployment rate moved incrementally lower, reaching 6.6% in January.

Source: Center on Budget and Policy Priorities

A number of “unusual” occurrences from the past month led to complications in the January jobs report. Some economists blamed the weather, others cited the recent expiration of federal unemployment benefits, and yet other economists said the Affordable Care Act is rearing its head.

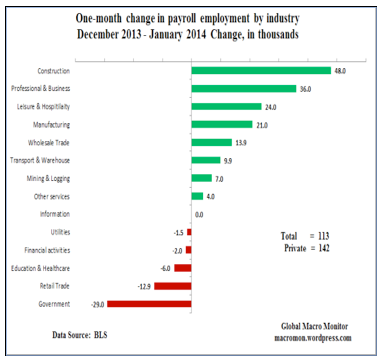

Interestingly, the notion that weather played a role in January hiring may be misguided. The sector experiencing the highest job growth last month was construction, adding 48,000 jobs. Construction is notoriously fickle around periods of unpredictable weather, suggesting that cold weather was not to blame last month. This may be recognition that December was impacted by weather conditions, though, as construction workers were hired in greater numbers during January.

Source: Global Macro Monitor

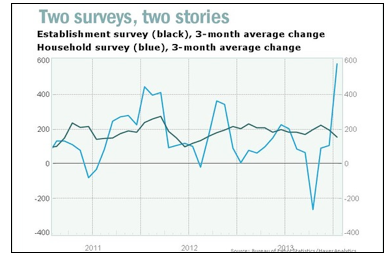

Inside the employment report, the two underlying surveys provided starkly different viewpoints on the health of labor markets. The establishment survey, which is based on sampling payroll reports from a wide number of businesses, provided the disappointing 113,000-job growth figure. On the other hand, the household survey, which surveys a random sampling of individuals 16 years and older, suggested that employment grew by more than 600,000 in January. The large dispersion between these two reports is common over shorter periods, and suggests a growth rate that is somewhere in the middle of these two reports.

Source: Marketwatch

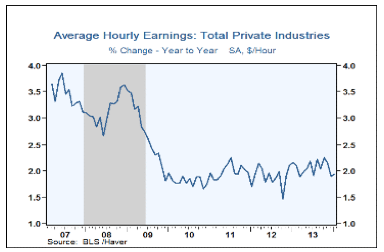

The other slightly positive news came in the form of the unemployment rate and wages. In January, the unemployment rate dipped to 6.6%, while average hourly earnings ticked up 0.2%. For the past year, earnings are up 1.9%, and the growth rate is ever so slightly moving in a higher direction.

Source: Haver Analytics

January’s labor report suggests it was the best of times, and the worst of times last month. Headline job growth was disappointing, but the household survey painted a more optimistic picture. As unemployment dips lower, and wages gain speed, the benefits to the economy will be obvious.

THE WEEK AHEAD

Economic data is limited this week in terms of volume, but includes notable reports such as retail sales on Thursday and industrial production on Friday. Important data is due outside of the US, however, including measures of Q4 GDP for the European Union and Japan.

On the central bank front, Janet Yellen gives her first Monetary Policy Report to Congress as Federal Reserve Chair on Thursday. No unexpected commentary is likely to emerge from that hearing. Global central banks meeting during the week include Indonesia, South Korea, Sweden, Serbia, Peru, and Russia.

ABOUT FORTIGENT

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

For more information, please visit our website at http://www.Fortigent.com.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value