Global Growth Expectations Push Stocks Forward Despite Weather

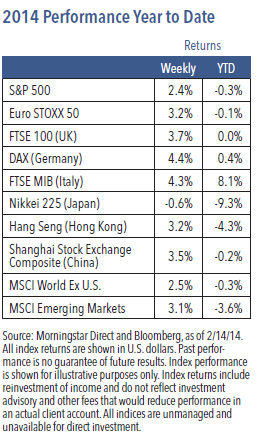

U.S. equities finished sharply higher last week with the S&P 500 increasing 2.3% and all major U.S. averages up more than 2%.1 The rapid market recovery from the January pullback is a bigger surprise than the pullback that preceded it.

Tailwinds Propel Equities Past Near-Term Weakness

Another batch of weaker-than-expected U.S. economic data did not accelerate concerns

about a slowdown in U.S. recovery momentum that had been hanging over the market since 2014 began. The weather impact, which is not only difficult to quantify but also expected to remain a near-term drag, was considered to be the main source of the soft data. New Federal Reserve Chair Janet Yellen’s emphasis on continuity of monetary policy was widely expected, yet particularly well-received. In addition, the House and Senate both passed a clean debt ceiling bill this week. A pickup in sentiment surrounding China was one of the higher profile tailwinds for global markets last week, and the ongoing recovery in Europe was also cited as supportive.

Weekly Top Themes

1.Retail sales missed expectations in January, falling 0.4%.2 We believe unusual weather patterns are probably suppressing the data. On the other hand, leading indicators such as the Fed’s senior loan survey and various indexes of financial and monetary conditions have shown no notable deterioration early in 2014. When weather returns to normal, energy prices should decline and boost the spring retail selling season.

2. Janet Yellen’s first official testimony pleased the markets and was interpreted

as continuity. The more informative Fed speech may have come from Federal Reserve Bank Philadelphia President Charles Plosser. He called the weather in January “unusually disruptive,” suggesting that it may take several more months of data to get a clear read on the economy.

3. The fiscal deficit has been reduced to just over 3% of GDP from more than 10% four years ago.3 Reasons for the improvement include the steady economic recovery despite various headwinds, including the 2013 sequester, higher tax rates and the gridlock in Congress that has effectively frozen federal spending over the last four years.

The Big Picture

We believe the cyclical advance in risk asset prices, particularly equities, still has legs. The recent setback should be viewed as a technical correction after the sharp run-up of last year. Underlying fundamentals continue to appear supportive; policy settings are very accommodative and global growth is strengthening, with equity valuations close to historical averages. We anticipate February payrolls will be soft due to continued abnormally disruptive weather. Despite subsequent weak payroll and retail sales reports, hiring plans hit a new cyclical high in the small business sector. Weather-related hits to the economy don’t change the underlying trend, and we expect solid payroll gains on average this year.

There has been a rotation into stocks over the past year at the expense of government bonds. This process is far from being advanced. There were massive, multi-year cumulative inflows into fixed income funds, and the shift in the other direction has barely started.4 Increased investor anxiety associated with the recent setback (small by historical standards) highlights the proverbial wall of worry yet to be climbed. Investors should expect 2014 to be more volatile, although improving economic data should begin convincing an increasing number of investors that the global expansion can be sustained.

We think the important takeaway is that the bull market for risk assets is not over in the absence of major exogenous shocks such as those that could come from policy mistakes in China or Europe. We believe there is more momentum behind the economy and earnings than most acknowledge, and surprises will continue to be to the upside after the weather improves. As confidence builds and the search for growth becomes a more dominant theme, investors are likely to focus on stocks with the best earnings power in a sustained but moderate growth environment.

1 Source: Morningstar Direct, as of 2/14/14. 2 U.S. Census Bureau, U.S. Department of Commerce, “Advance Monthly Sales for Retail and Food Services January 2014,” February 13, 2014, http://www.census.gov/retail/. 3 Source: Barron’s, “The Hidden Good News on Jobs,” February 15, 2014, http://online.barrons.com/article/SB50001424053111903506304579375011776442236.html#.

4 Source: Investment Company Institute, “Estimated Long-Term Mutual Fund Flows,” February 12, 2014 http://www.ici.org/research/stats/flows.

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure the performance of the broad domestic economy. Euro STOXX 50 Index is Europe’s leading Blue-chip index for the Eurozone and covers 50 stocks from 12 Eurozone countries. FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange. Deutsche Borse AG German Stock Index (DAX Index) is a total return index of 30 selected German blue chip stocks traded on the Frankfurt Stock Exchange. FTSE MIB Index is an index of the 40 most liquid and capitalized stocks listed on the Borsa Italiana. Nikkei 225 Index is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. Hong Kong Hang Seng Index is a free-float capitalization-weighted index of selection of companies from the Stock Exchange of Hong Kong. Shanghai Stock Exchange Composite is a capitalization-weighted index that tracks the daily price performance of all A-shares and B-shares listed on the Shanghai Stock Exchange. The MSCI World Index ex-U.S. is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets minus the United States. The MSCI Emerging Markets Index is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets.

RISKS AND OTHER IMPORTANT CONSIDERATIONS

The views and opinions expressed are for informational and educational purposes only as of the date of writing and may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The information provided does not take into account the specific objectives, financial situation, or particular needs of any specific person. All investments carry a certain degree of risk and there is no assurance that an investment will provide positive performance over any period of time. Equity investments are subject to market risk or the risk that stocks will decline in response to such factors as adverse company news or industry developments or a general economic decline. Debt or fixed income securities are subject to market risk, credit risk, interest rate risk, call risk, tax risk, political and economic risk, and income risk. As interest rates rise, bond prices fall. Noninvestment- grade bonds involve heightened credit risk, liquidity risk, and potential for default. Foreign investing involves additional risks, including currency fluctuation, political and economic instability, lack of liquidity and differing legal and accounting standards. These risks are magnified in emerging markets. Past performance is no guarantee of future results.

Nuveen Asset Management, LLC is a registered investment adviser and an affiliate of

Nuveen Investments, Inc.

GPE-BDCOMM3-0214P

© Nuveen Investments